Our fallen productivity is a "national emergency."

Canada’s poor economic productivity has been in the headlines lately, with the Bank of Canada calling it a national emergency.

Today, I will discuss what economic productivity means and what role the housing market might play in Canada’s poor performance.

Statistics Canada defines productivity as “the efficiency with which an economy transforms inputs into outputs”.

The Bank of Canada highlighted three elements that contribute to strong productivity:

- Capital intensity—giving workers better physical tools like machinery, and using new technologies to improve efficiency and output

- Labour composition—improving workers’ skills and training

- Multifactor productivity—using capital and labour more efficiently

A recent report by Alberta Central chief economist Charles St-Arnaud noted that while Canada had the sixth-highest labour productivity out of 32 OECD countries in 1970, it ranks 22nd today.

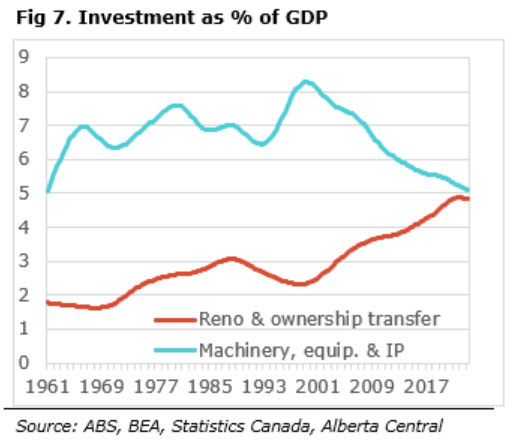

According to St-Arnoud, one of the big reasons why Canada’s labour productivity is falling is that Canadian businesses are investing far less in physical tools and technologies that would make their labour force more efficient. Since 2000, the share of Canada’s GDP spent on machinery, equipment, and IP has declined, while the share of residential investment in renovations and transfer costs has increased and is now nearly identical.

St-Arnoud argues that one of the significant drivers behind this change is the supply of credit from financial institutions. Lenders are willing to lend to borrowers who offer the greatest risk-adjusted return on their capital.

Over the past twenty years, residential mortgages have proven to be a relatively low-risk investment for banks compared to commercial debt, not only because mortgage default rates in Canada are extremely low but also because the collateral on mortgage debt (the value of each home) has appreciated over time. This, coupled with higher capital requirements for corporate lending, has made corporate debt considerably more expensive, contributing to the decline in corporate lending.

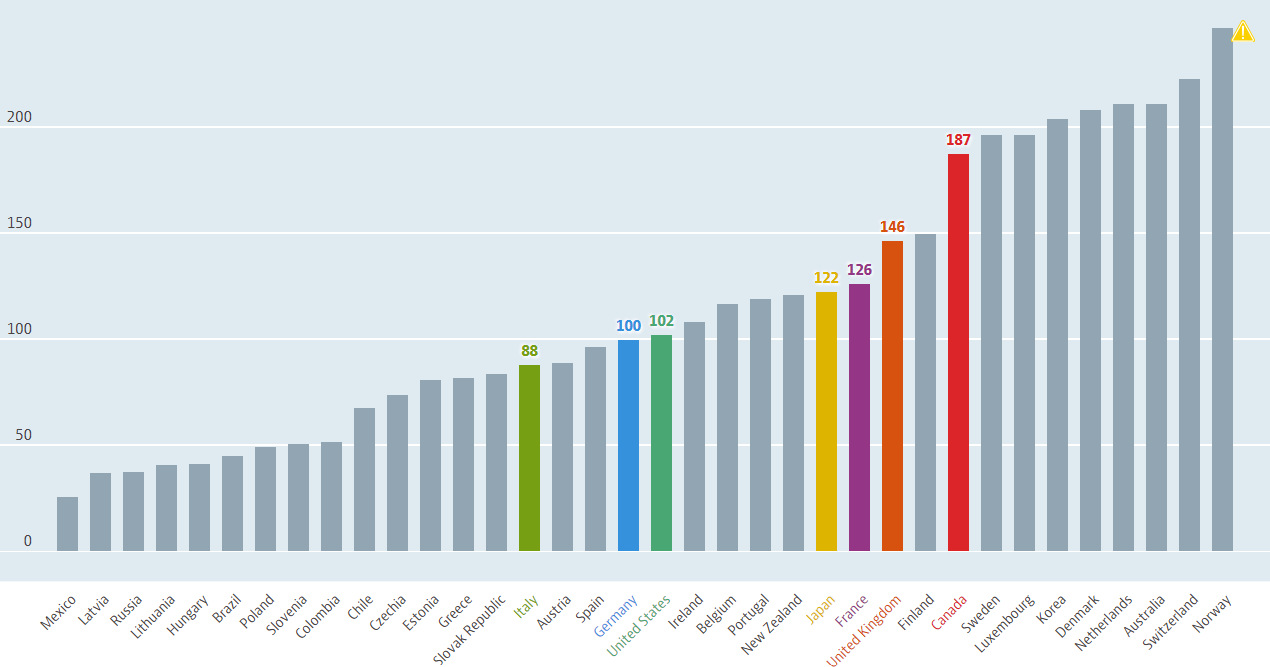

While households were net savers in Canada from the 1960s to 2000, they have since become net borrowers, contributing to Canada’s rapid increase in household debt relative to income and GDP.

Household Debt - Total, % of net disposable income, 2022 or latest available

Source: OECD

According to St. Arnoud, the solution to Canada’s productivity problems requires two important policy responses: incentives to increase lending to corporations and incentives to encourage households to save more and borrow less.

Unfortunately, converting a nation that has become addicted to using its home equity as an ATM to finance renovations, investments, and lifestyles is easier said than done. Converting households to net savers rather than borrowers can only be achieved by making it harder for homeowners to borrow against their home equity, which banks and policymakers are in no rush to do.

John Pasalis is President of Realosophy Realty. A specialist in real estate data analysis, John’s research focuses on unlocking micro trends in the Greater Toronto Area real estate market. His research has been utilized by the Bank of Canada, the Canadian Mortgage and Housing Corporation (CMHC) and the International Monetary Fund (IMF).

Have questions about your own moves in the Toronto area as a buyer, seller, investor or renter? Book a no-obligation consult with John and his team at a Realosophy here: https://www.movesmartly.com/meetjohn

Published: April 23, 2024