It's always felt hard to be a renter in Toronto - but a dig into the numbers shows the problem has gotten much worse.

Anyone who has lived in Toronto for some time might conclude that the city has always had a rental crisis. Vacancy rates have been stubbornly low for decades, and I remember hearing about Toronto’s rental crisis when I was still a university student.

When things feel like a never-ending crisis, it’s hard to figure out if things have always been this bad or if there was a point in time when things got dramatically worse for renters. The only way to answer this question is to look at the data.

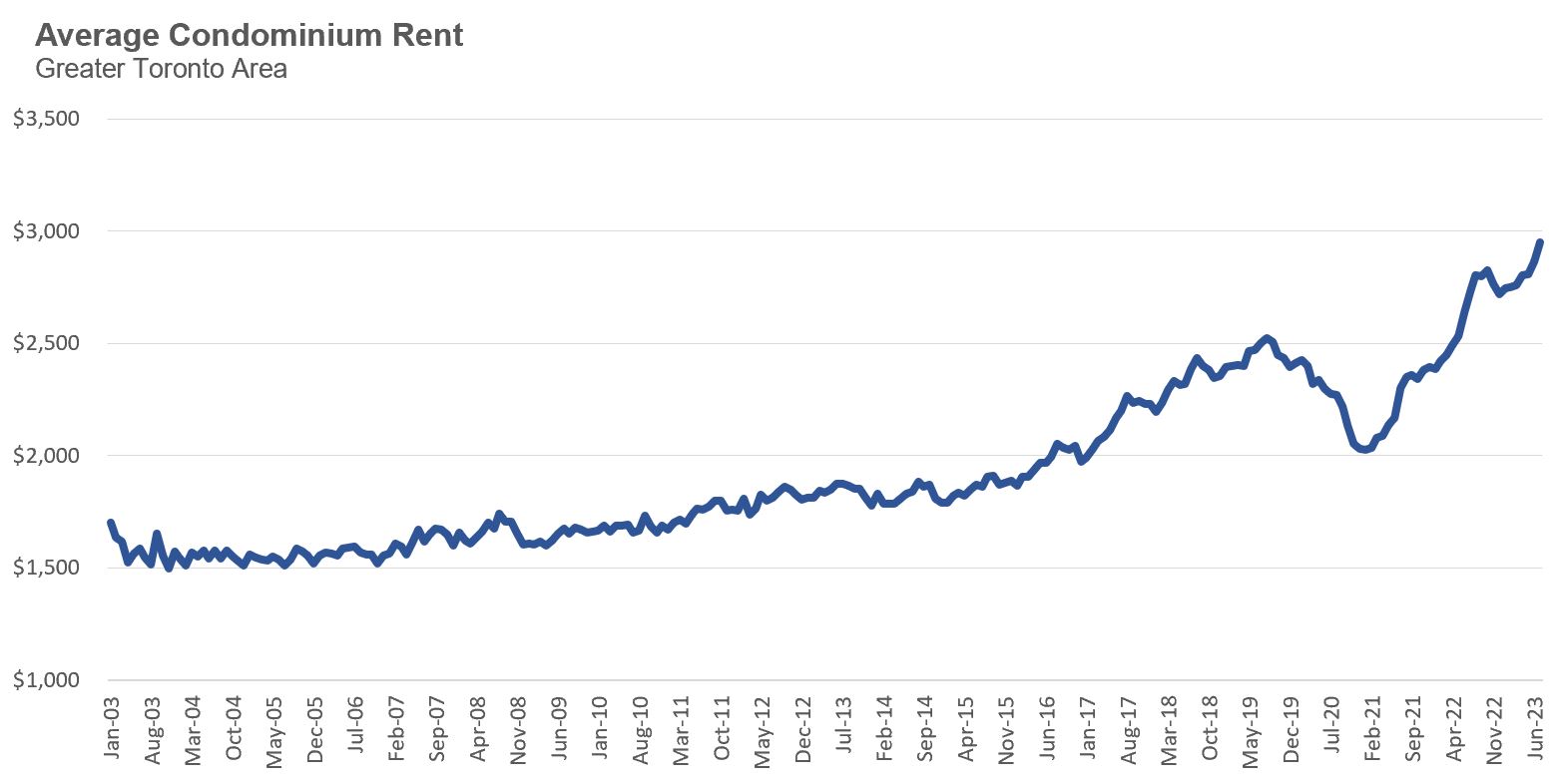

The rental data I will be using for this Data Dive is based on condominium apartment rental transactions from the Toronto Regional Real Estate Board’s MLS system. The chart below shows the average rental price for a condominium apartment from 2003 to July 2023.

When looking at a relatively long time series of rents, we are interested in understanding if rents have been rising at a similar rate over time or if there is a particular period where rents were rising much faster than other periods. In this chart, it’s quite clear that rent prices were rising gradually between 2003 and 2015 before rapidly accelerating in the following years.

Average rents declined in the second half of 2020 as part of the urban exodus due to COVID, but they quickly recovered and are currently well above pre-COVID levels.

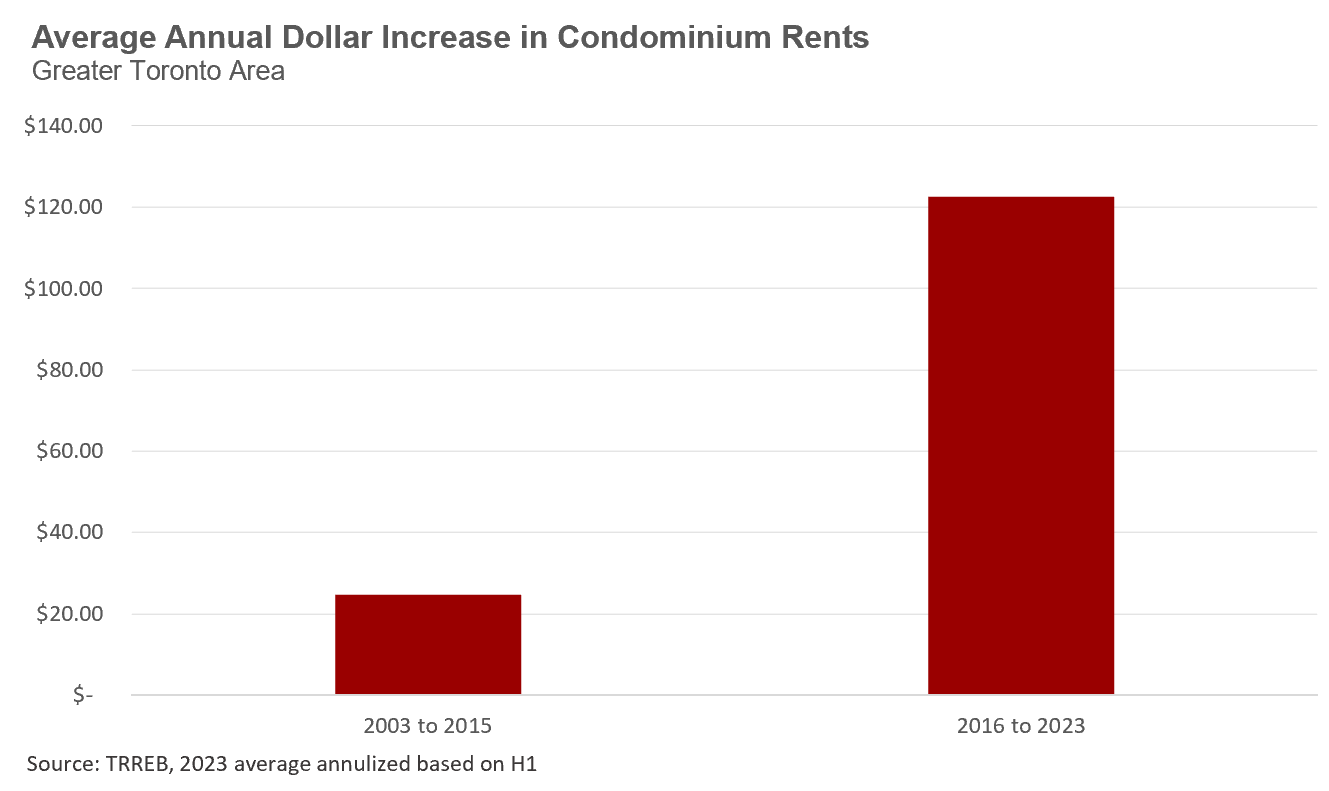

To get a better understanding of how average rents changed during the period of modest rent growth between 2003 and 2015 vs the following period, it’s helpful to convert the single-month average prices to a twelve-month average for each month, as this way, we are not putting too much emphasis on the fluctuations in a single month’s average price data. Going forward, any reference to average rent will refer to the previous twelve-month average.

In January 2004, the average condo rent was $1,564; by the end of 2015, the average rent had reached $1,862. That translates to a $298 increase in average rent over twelve years. If we break out this twelve-year increase into an average annual number, we find that the average condo rent increased each year by $25 per month.

In contrast, the average condo rent for January 2016 was $1,866, which climbed to $2,786 in June 2023. That translates to a $920 increase in the average rent over a seven-and-a-half-year period. If we break out this seven-and-a-half-year increase into an average annual number, we find that the average condominium rent increased each year by $123 per month.

So if it feels like Toronto’s rental crisis keeps getting worse, that’s because it is getting worse.

Annual condominium rents in Toronto are increasing 5 times faster after 2016 than they were before 2016.

What might be driving this rapid increase in rent since 2016?

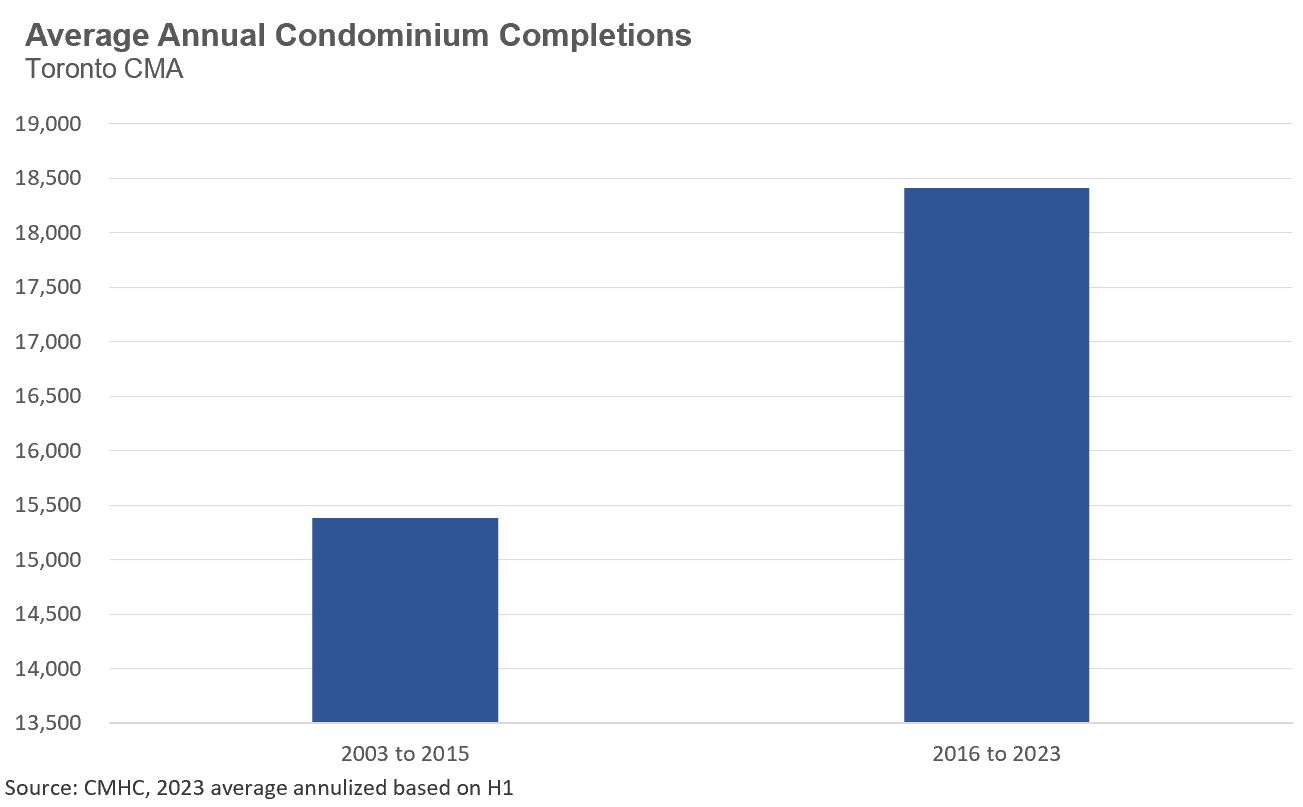

The common explanation we hear from politicians, some economists and housing advocates is that this rapid increase in rents is due to a lack of supply. Specifically, either the city or province (or both) are restricting the supply of new housing through red tape, restrictive zoning policies, or to satisfy the demands of NIMBYs, or Not-In-My-Backyard-Neighbours who protest any new housing development planning for their area.

But unfortunately, this narrative doesn’t really hold up very well in explaining why rents have so rapidly accelerated when one looks at the data. Average annual condo completions in the Toronto CMA were actually higher in the years after 2016 than before 2016.

This does not mean that provinces and municipalities don’t need to do more to encourage more housing, especially when we consider that this increase in condo completions after 2016 was also coupled with a decline in new low-rise completions.

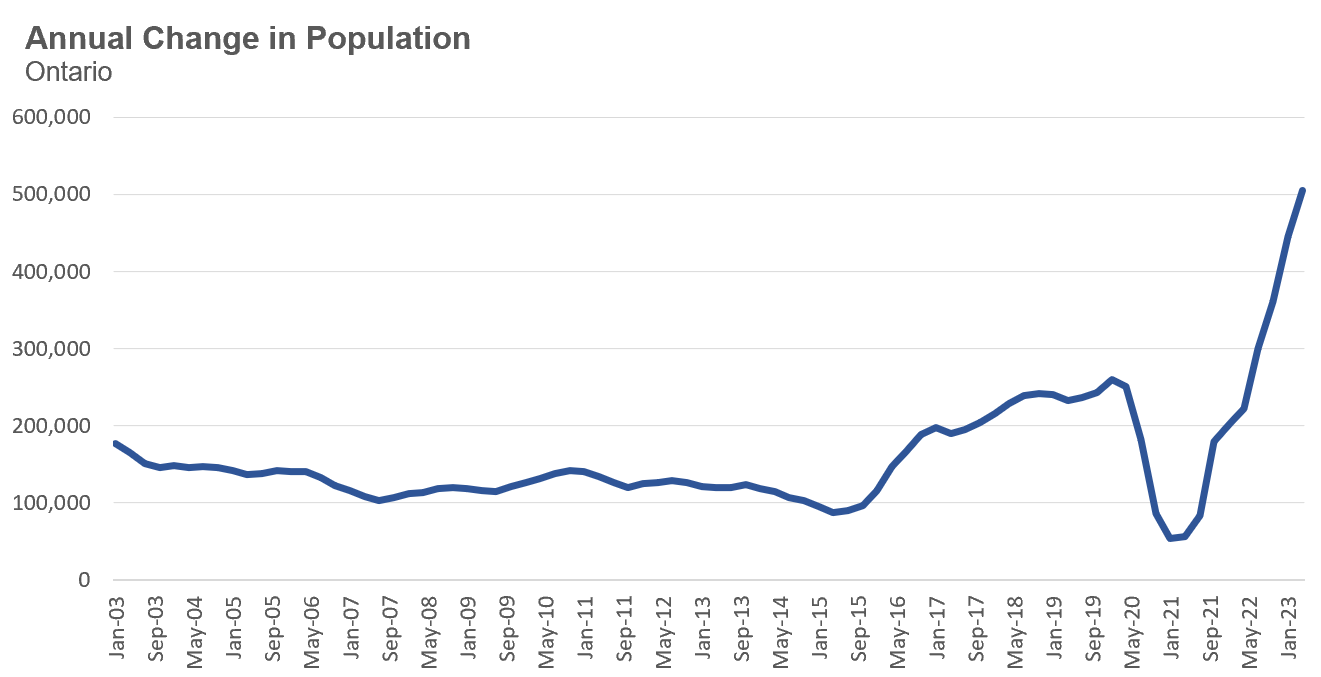

But ultimately, condo rents are a function of the demand for rentals and the supply of new completions each year. While the supply of new condo units increased, this growth did not help to cool rent prices because Ontario’s population growth, and by extension, the demand for rental housing, has grown far more rapidly over the same period.

Prior to 2016, Ontario’s population was growing by an average of 125,000 people per year. We saw that number increase to well over 200,000 between 2016 and 2020. After a short dip in 2020 due to COVID, Ontario’s population has grown by over 500,000 over the previous twelve months.

When a government rapidly increases the demand for housing without giving any thought to where people will live, the natural result is a market where average rents are increasing five times faster than historical trends.

When Canada’s new immigration minister Marc Miller announced that Ottawa might increase the rate at which our population is growing, this raised some questions from people concerned about Canada’s housing crisis.

University of Toronto economist Rob Gillezeau unpacked the federal government’s rationale and consequences of their immigration strategy on Twitter when he said (emphasis is mine):

“It's hard to fathom that government would knowingly choose to further exacerbate the housing crisis, but at least the federal government is being clear about its policy path. I do appreciate

Marc Miller's honesty on the rationale. Rather than engaging in other reforms to ensure long run fiscal sustainability, government is choosing a temporary worker + immigration to path to meeting that fiscal goal. That may be an economically viable path, but it comes with enormous costs with respect to the housing crisis & inequality that will disproportionately hurt newcomers, young people, renters, and working & middle class Canadians.”

In short, rather than engaging in other reforms to ensure Canada’s long-run fiscal sustainability, our federal government is using a shortcut solution, rapidly increasing Canada’s population growth, which they should know comes with enormous costs to the poorest households in Canada.

Sacrificing the poor for a shortcut to economic growth is not a promising vision for Canada.

John Pasalis is President of Realosophy Realty. A specialist in real estate data analysis, John’s research focuses on unlocking micro trends in the Greater Toronto Area real estate market. His research has been utilized by the Bank of Canada, the Canadian Mortgage and Housing Corporation (CMHC) and the International Monetary Fund (IMF).

Published: September 07, 2023