“Soon the price action – or at some point the price action takes over, and you want to buy three houses and five houses and you want to buy it with nothing down and you want to agree to payments that you can’t make and all of that sort of thing, because it doesn’t make any difference: It’s going to be worth more next year.”

- Warren Buffett

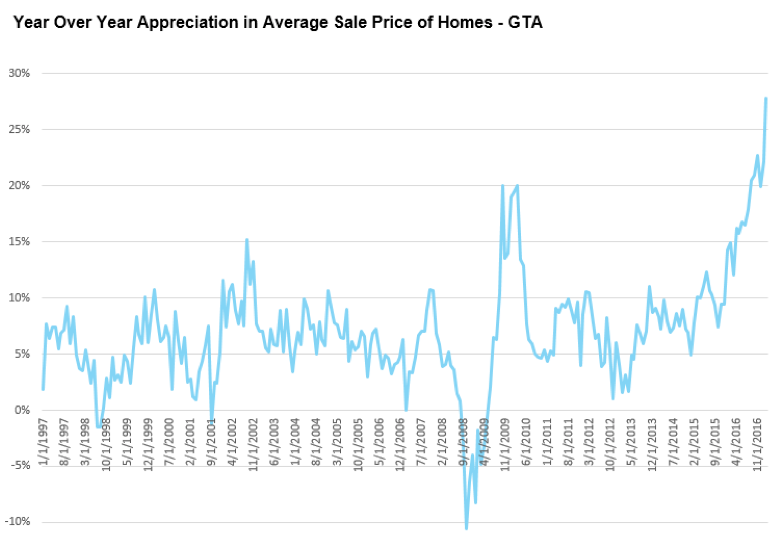

Toronto’s real estate market is already at a critical point. Detached house prices are appreciating at a rate of over 30% year over year and if public policy makers want to introduce policies that cool our housing market, they need to act now.

But first, they need to diagnose the problem correctly. Rising house prices are merely a symptom of underlying problems – they do not reveal the cause of it. Understanding the cause is critical if government is to introduce a policy that actually works to cool our market safely by targeting unhealthy behaviours instead of all behaviours (or the wrong behaviours altogether). Misunderstanding the cause could instead result in a prescription that exacerbates problems.

It does not help that our market is full of commentators who always argue that the Toronto real estate market is on the verge of collapse. As there are many factors that affect supply and demand in real estate, these commentators move from one suspect factor to another (e.g., price to income ratio, price to rent ratio, etc.). It is not that these factors are unimportant, but more precision is needed to determine what factor at a particular point in time is causing a particular problem.

Conversely many in the real estate industry see perennially healthy markets. One long standing view, held by the Ontario Real Estate Association (OREA) and the Toronto Real Estate Board (TREB), is that the problem with Toronto’s housing market has nothing to do with ‘improper’ demand – high demand for houses is understandable because Toronto is a world-class city that many people, both Canadian and foreign, want to live in. Rising immigration and migration to the GTA explains why demand and prices continue to rise. The real problem, this theory suggests, is that our municipal and provincial governments are preventing builders from building enough homes (a “supply” problem). The solution is to allow builders to get their projects approved more quickly so we could build ourselves out of this problem. This argument is not entirely without merit – governments do impact supply, for example, by introducing policies to prevent housing sprawl and promote higher density housing (condos) over lower density housing (detached houses).

But the numbers for this theory don't add up.

Toronto’s house price appreciation has seen an average growth rate of 7% annually over the last twenty years, with a rapid acceleration to the 20%-30% range last year. The only other time appreciation reached the 20% range in Toronto over the last 20 years was in late 2009, one year after the US crisis.

Part of Toronto’s 7% growth story is no doubt due to high demand from those looking to live in Toronto coupled with restricted housing supply. But if immigration is responsible for the 20-30% increase in house prices we are seeing, we would expect the data to show this but Statistics Canada Census data shows that Toronto’s population only grew by 6.2% during the 2016 Census, down from 9.2% in 2011 and the slowest population growth rate over the past 40 years.

Government policies restricting sprawl and promoting density (Ontario’s Places to Grow Act, was introduced in 2006, other initiatives date back further) have had some impact on house prices (such policies are intended to), but there have been no marked changes to those policies over the last few years which can explain skyrocketing appreciation rates from 2016 onwards.

The goal of this research was to see if there is any quantitative evidence that corroborates many of the observations we have made about the demand from these investors as well as their attitudes towards their investments.

Specifically, I wanted to answer two important questions:

1) Is the GTA seeing a rise in the number of people buying single family homes strictly to rent them out?

2) What percentage of those investors would be breaking even assuming they made a 35% down payment?

In many areas of real estate, the government and the real estate industry are surprisingly poor at gathering, tracking and sharing data, though they should presumably be enacting policies in response to such data. For example, the impact of government policies on house building is hard to measure because the supply, use and development of land (mostly in the hands of private companies) is not well tracked. The impact of foreign investors in Toronto has been hard to measure because of lack of data on the precise immigration status of individuals buying properties.

However, real estate listing data which reflects the details of how properties are being bought and sold, such as the data contained in the Toronto Real Estate Board’s Multiple Listing Service (MLS) database, can tell us a lot about larger trends, if we look at it carefully.

For the purposes of my analysis, an investor is defined as someone who has bought a property that was listed on the MLS and subsequently listed it for lease on the MLS either in the same calendar year or in the first two months of the following calendar year.

To answer whether or not we are seeing an increase in the number of investors buying homes in the GTA, I first calculated how many freehold houses (detached, semi-detached and rowhouse) sold each year over the past 5 years through the MLS.

To calculate the number of homes purchased by investors each year, I checked all the homes that sold in a given year to see if the property that sold was also listed for rent (lease) on the MLS after the new owner took possession.

This is not to say that every single person renting their home after taking possession is an investor – I expect there to be a certain percentage of buyers each year who for various reasons cannot move into their home and have to rent it out. But I don’t expect the number of buyers who fit this description to fluctuate much from one year to the next.

One advantage to this methodology is that it provides quantitative evidence of homes that were purchased by investors strictly to be rented out. It also gives us some insight into the actual price investors are paying for their investments and how much they are actually earning in rent when they lease them.

The downside to this approach is that it understates the actual number of investors in the market because not all investors list their properties for rent on the MLS after they buy.

Specifically, there are four main types of investors that would not be captured in our analysis:

While this approach has its shortcomings by understating overall investor demand, it should offer some insight into investor behaviour.

In 2012, approximately 4% of all freehold houses that were sold on the MLS system were listed for lease shortly after the new owner took possession.

In 2016, four years later, that percentage more than doubled to 10% with investors buying 5,705 out of the 58,3330 freehold houses.

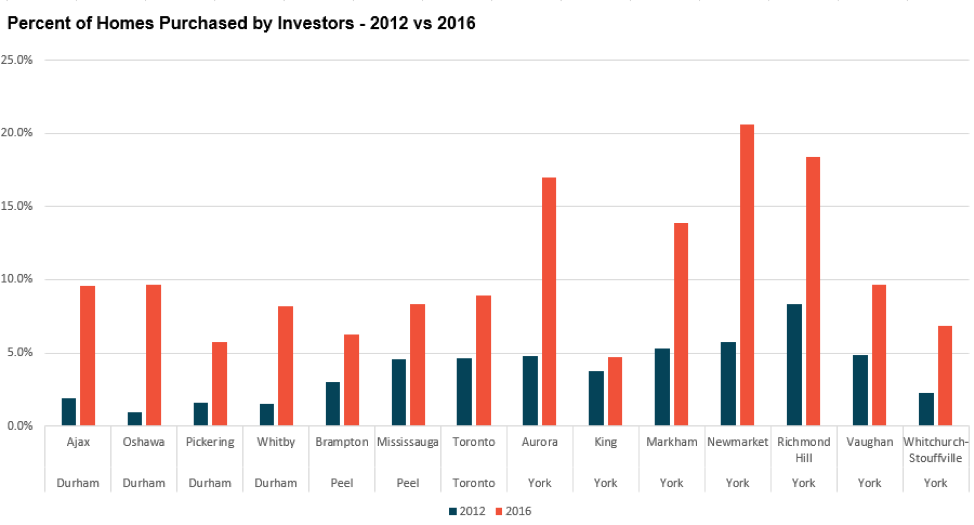

When we look at how demand from investors has changed across the GTA by municipality we see a number of interesting localized trends.

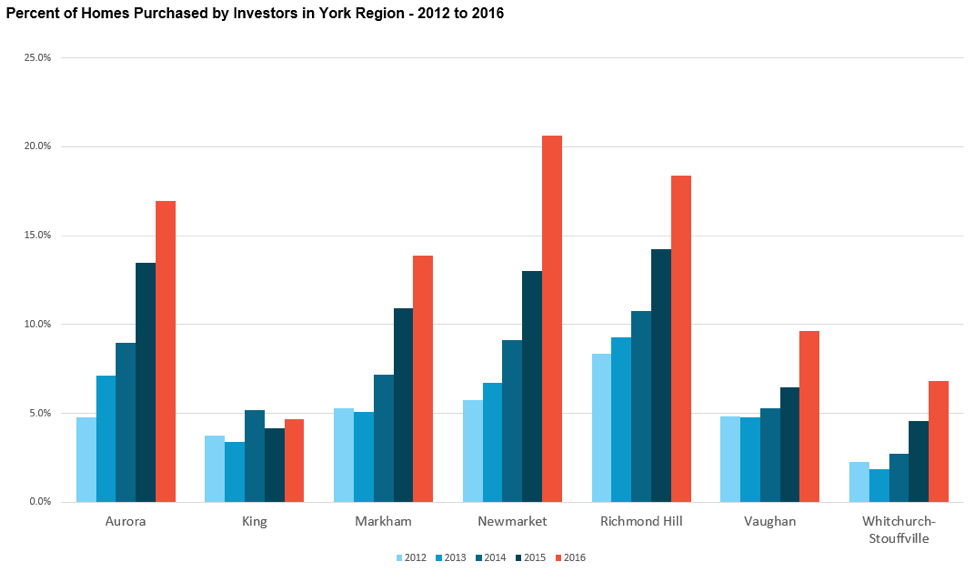

The top four in demand municipalities in the GTA were all in York Region. Newmarket topped the list where 20.6% of all homes sold were purchased by investors. Demand from investors increased by 260% from 2012 when investors made up 5.7% of all sales.

In 2012, Richmond Hill was the most sought after municipality in the GTA for investors where they accounted for 8.3% of all sales. Since then investor demand has continued to grow and is responsible for 18.4% of all sales in Richmond Hill.

Aurora saw sales to investors climb 255% from 4.8% in 2012 to 17% in 2016 while Markham saw investor demand climb from 5.3% to 13.9% in the same period.

Investors made up 9.6% of all transactions in Vaughan in 2016, an increase from 4.8% in 2012. Whitchurch-Stouffville saw investors make up 6.8% of sales in 2016, an increase from 2.3% in 2012.

King saw the most modest demand from investors in 2016 where they made up just 4.7% of all sales, a 25% increase from 3.7% in 2012.

The table below shows the average sale price of homes that were purchased by investors in 2016, along with the average rent earned for those properties.

|

|

Average Price |

Average Rent |

|

Aurora |

$937,625 |

$2,201 |

|

King |

$1,186,909 |

$2,470 |

|

Markham |

$1,137,166 |

$2,241 |

|

Newmarket |

$784,268 |

$1,943 |

|

Richmond Hill |

$1,183,763 |

$2,277 |

|

Vaughan |

$1,001,616 |

$2,451 |

|

Whitchurch-Stouffville |

$787,135 |

$1,967 |

Looking at sales at the neighbourhood level, we found that the two most attractive neighbourhoods for investors in York Region were Markham’s Bullock (McCowan Road & Hwy 407) where investors accounted for 39% of all transactions and Richmond Hill’s Crosby (Yonge St & Major Mackenzie Dr E) where investors purchased 36% of all homes in 2016.

The average price of the homes purchased by investors in Bullock in 2016 was $1,160,229 while average rents were $1,870 per month.

The average price of the homes purchased by investors in Crosby in 2016 was $1,058,497 while average rents were $1,812 per month.

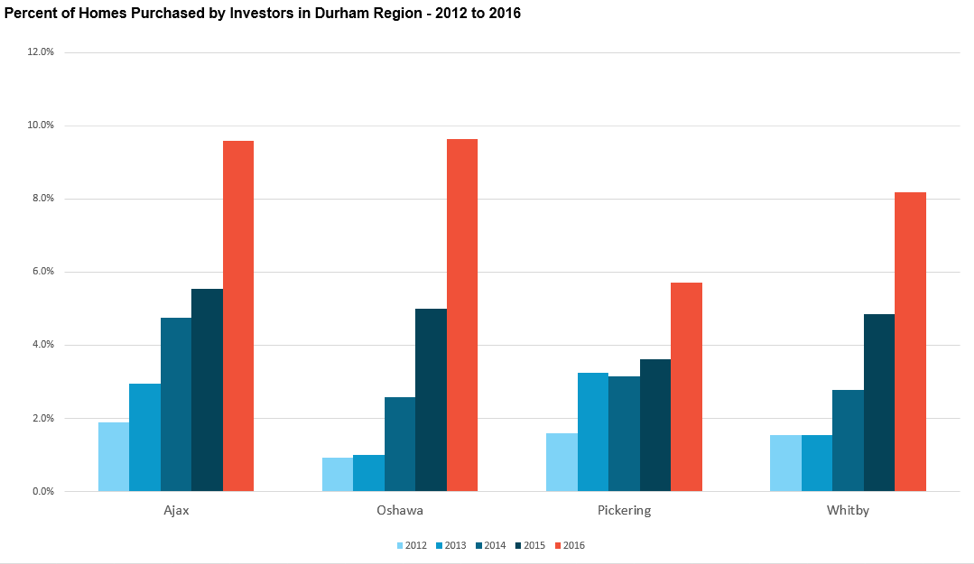

While the percentage of homes purchased by investors for the municipalities in Durham in 2016 was relatively average for the GTA, Durham is noteworthy because it has seen the most rapid increase in the demand from investors.

Oshawa in particular saw the biggest increase in demand from investors over the past four years. In 2012, less than 1% of properties were purchased by investors. By 2016, demand from investors increased by 944% with investors making up 9.6% of all purchases in 2016.

Investors made up fewer than 2% of transactions in Ajax and Whitby in 2012. Both municipalities saw demand increase by more than 400% as sales from investors made up 9.6% and 8.2% in Ajax and Whitby respectively in 2016.

Pickering saw the most gradual increase for the region, with sales to investors climbing from 1.6% in 2012 to 5.7% in 2016.

The table below shows the average sale price of the homes that were purchased by investors in 2016 along with the average rent earned for those properties.

|

|

Average Price |

Average Rent |

|

Ajax |

$612,304 |

$1,928 |

|

Oshawa |

$518,363 |

$1,797 |

|

Pickering |

$653,364 |

$1,898 |

|

Whitby |

$581,960 |

$1,892 |

Looking at demand from investors at the neighborhood level, we found the demand from investors strongest in Oshawa neighbourhoods Taunton (Wilson Rd N and Tauton Rd E) and Windfields (Simcoe St N and Conlin Rd) where investors drove 18% and 15% of sales respectively.

The average price for the homes purchased by investors in Taunton and Windfields were approximately $636,000 while average rents were approximately $2,000 per month.

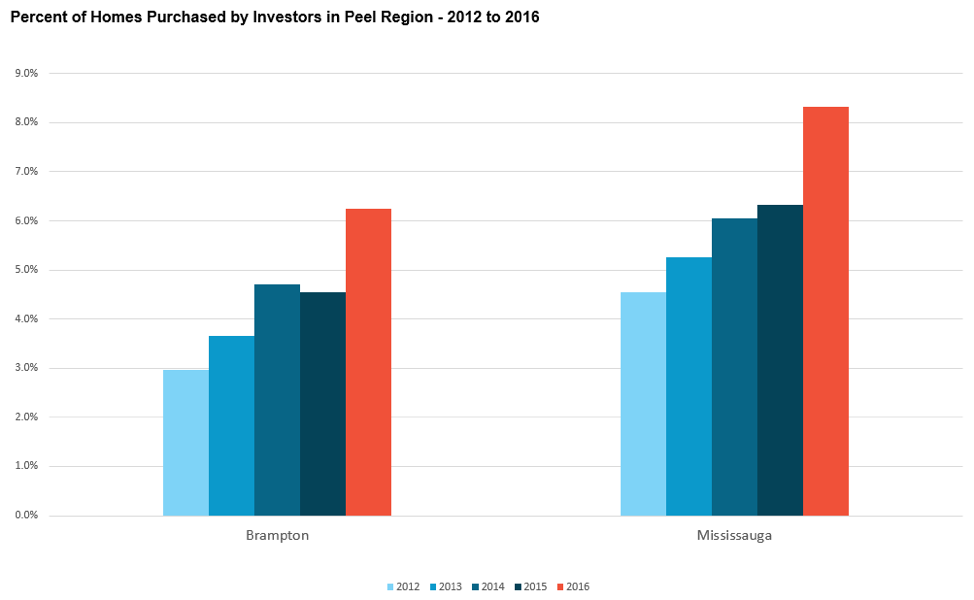

Brampton and Mississauga were among the municipalities with the slowest rate of growth in demand from investors.

In 2012, investors accounted for 3% of sales in Brampton and 4.5% of sales in Mississauga; in 2016, this increased to 6.3% and 8.3% for Brampton and Mississauga respectively.

The table below shows the average sale price of the homes that were purchased by investors in 2016 along with the average rent earned for those properties.

|

|

Average Price |

Average Rent |

|

Brampton |

$577,431 |

$1,820 |

|

Mississauga |

$814,776 |

$2,278 |

The most popular neighbourhoods for investors in Peel were the Mississauga neighbourhoods of Fairview (Mavis Rd & Burnhamthorpe Rd W) and Central Erin Mills (Britannia Rd & Winston Churchill Blvd) where investors accounted for 16% and 15% of sales respectively.

The average price of the homes purchased by investors in Fairview in 2016 was $745,000 while average rents were $2,230 per month.

The average price of the homes purchased by investors in Central Erin Mills in 2016 was $1,003,000 while average rents were $2,653 per month.

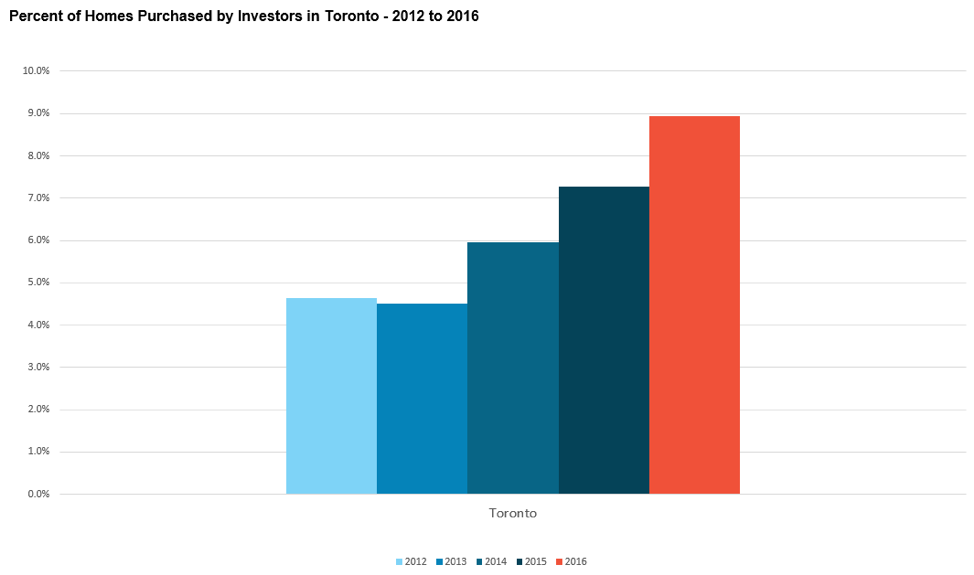

The City of Toronto saw demand from investors increase by 93% in the four years from 2012 to 2016. Investors accounted for 9% of all sales in Toronto in 2016.

The table below shows the average sale price of the homes that were purchased by investors in 2016 along with the average rent earned for those properties.

|

|

Average Price |

Average Rent |

|

Toronto |

$1,195,789 |

$2,777 |

The highest demand neighbourhoods from investors in Toronto were Henry Farm (Sheppard Ave E & Leslie St) and Lawrence Park North (Lawrence Ave E & Yonge St) where investors accounted for 22% and 20% of all sales respectively.

The average price of the homes purchased by investors in Henry Farm in 2016 was $1,505,500 while average rents were $3,015 per month.

The average price of the homes purchased by investors in Lawrence Park North in 2016 was $1,653,900 while average rents were $4,381 per month.

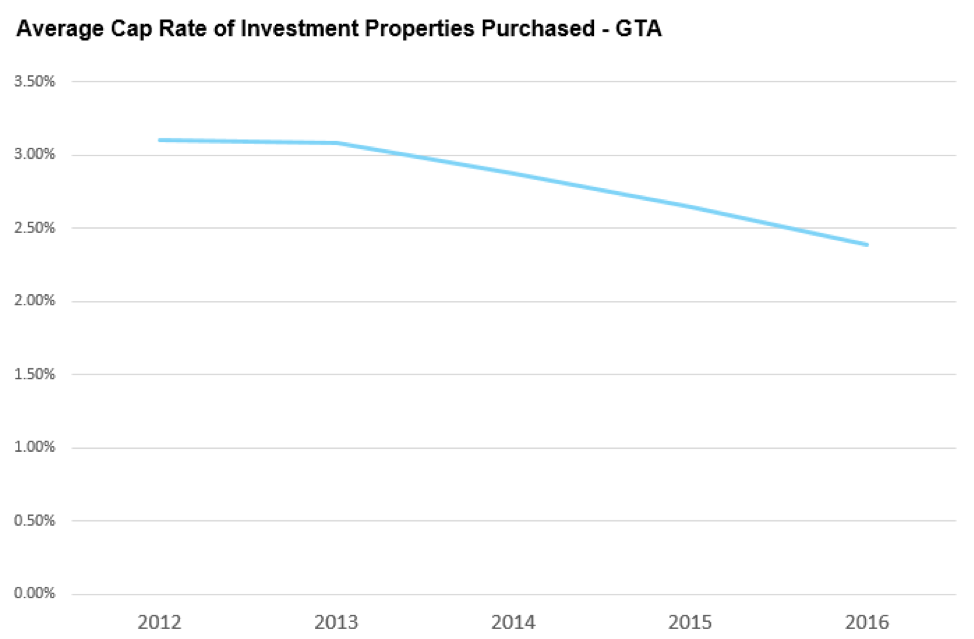

One of the main metrics investors use to measure the potential return on a real estate investment is something called the capitalization rate (cap rate for short). To calculate the cap rate, investors first estimate the net income of the rental property by adding up the estimated rents for the entire year then subtracting all expenses (excluding mortgage payments). Once they have the net income for the property, they divide it by the estimated purchase price to get the cap rate.

As an example, suppose I bought a $500,000 home as an investment and I estimate that I’ll be able to collect $2,000 in rent each month and the annual expenses for the home are approximately $4,000.

My net income for the home would be $20,000 ($24,000 in rent minus $4,000 in expenses).

This would leave me with a cap rate of 4% ($20,000 net income / $500,000 purchase price).

Real estate investors would generally be satisfied with a cap rate in the 4%-6% range for a residential property.

Below is a chart showing the average cap rate for all the properties purchased by investors between 2012 and 2016.

The cap rate for the

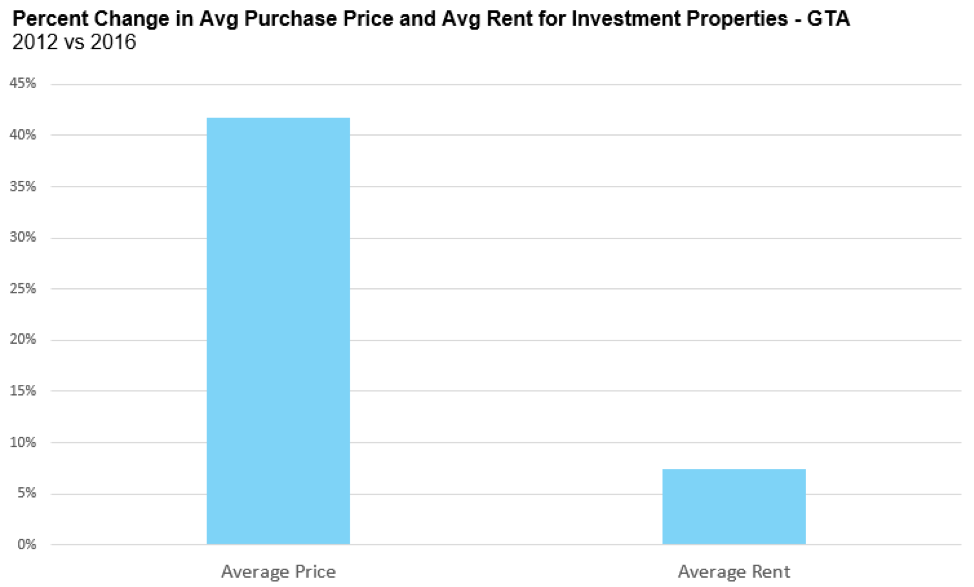

The chart below shows the percentage increase in the average price of the homes purchased by investors from 2012 to 2016 against the average price of the rent they generated during the same period.

The average price of the homes purchased by investors was $669,564 in 2012 and increased by 47% to $949,175 in 2016. The average rent generated on these homes was $2,124 in 2012 and climbed just 7% to $2,283 in 2016.

Another

To estimate the percentage of investment properties breaking even each month, I was able to rely on information in the MLS including the price the investor paid for their property, their annual property taxes and how much they leased the house for.

The table below highlights the source of the data for my income and expense calculations along with several assumptions.

|

Rent |

Actual rent for leased properties on the MLS |

|

Property Taxes |

Actual property tax amount advertised on the MLS when the investor bought the house |

|

Insurance and Maintenance |

Estimated at a fixed $160 per month |

|

Utilities |

No utility expenses were included for the landlord |

|

Vacancy |

Assumed the properties were fully rented 365 days out of the year |

The mortgage payment was calculated based on the actual sale price of each home and I assumed a 35% down payment and an interest rate of 2.8% and a

Using the methodology described above, I was able to estimate what percentage of properties were cash flow positive vs negative each month.

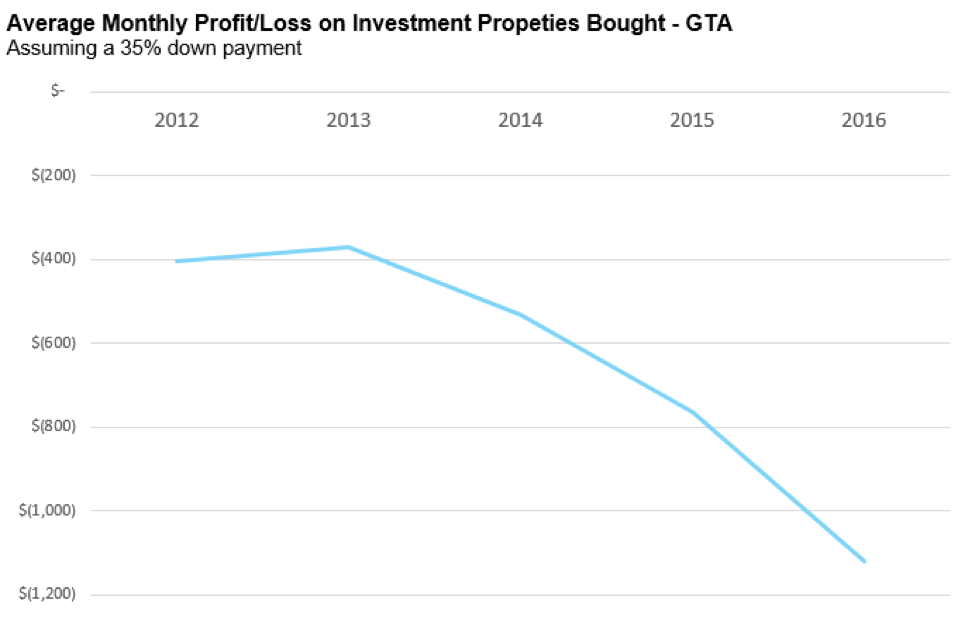

When taking into account the actual purchase price of each home, the amount it was leased for and the estimated expenses, 95% of the investment properties purchased in 2016 would be losing money every month. This means that 95% of the owners who bought investment properties would personally have to contribute to the carrying costs of the property because the rent alone is not sufficient to cover the expenses of the home. The average monthly loss per property in 2016 was $1,121.

In 2012, 68% of all the investment properties were losing money each month with the average loss coming in at $406.28.

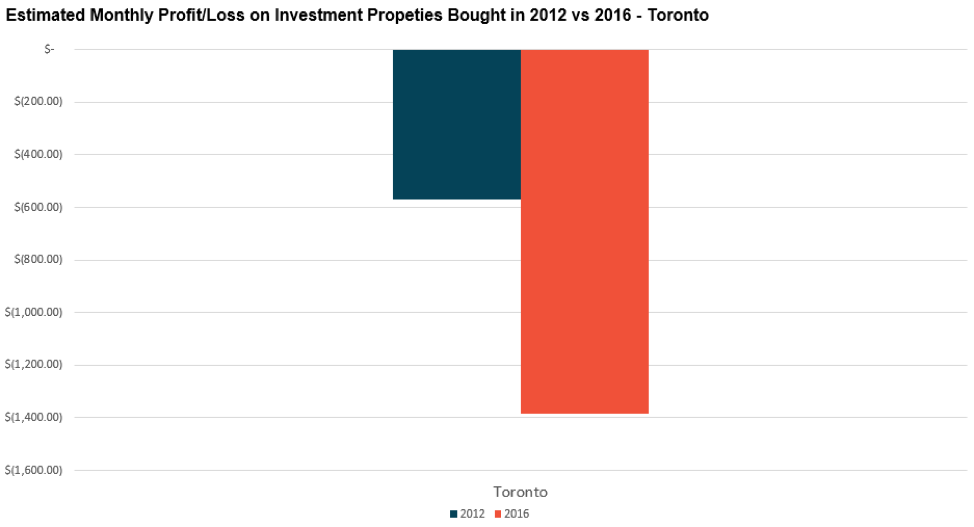

The chart below shows how the average monthly loss on the investment properties purchased has changed over the past five years.

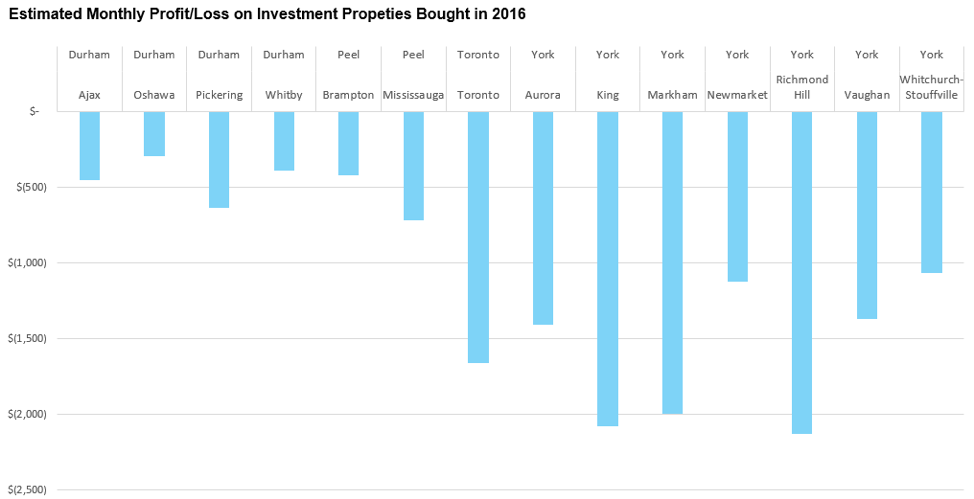

The chart below shows the average monthly loss for the investment properties purchased in 2016.

It is important to note that the estimated average monthly losses for these investments

Specifically, we have heard anecdotal accounts that many foreign investors are purchasing properties with more equity than I have assumed in our example. This means that the losses for these investors may not be as significant as described above.

On the other hand, domestic investors are likely purchasing investment properties with less equity that I have assumed. Anecdotal accounts suggest that most domestic investors are borrowing against the equity of their principal residence to come up with the down payment for their investment properties.

Even with the assumption that domestic investors are making a 35% down payment when buying an investment property – this means that in many cases their investment properties are effectively being financed entirely by debt – 65%

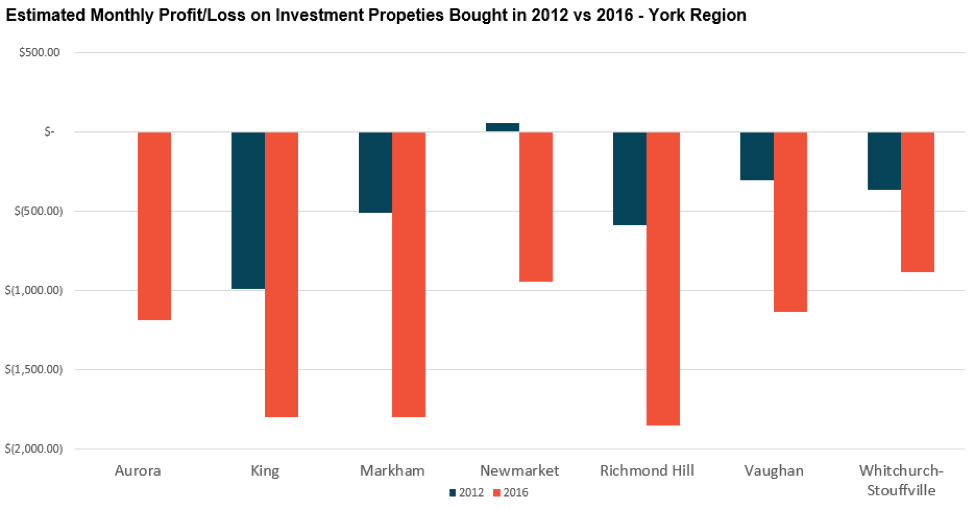

The chart below shows how the monthly profit and/or loss from these investment properties has changed over time in York Region.

In 2012, investments in Aurora were on average breaking even while investments in Newmarket were making a slight profit. Markham and Richmond Hill both saw monthly losses in the $500 per month range.

By 2016, all municipalities on average were running at a monthly loss on their investments with King, Markham

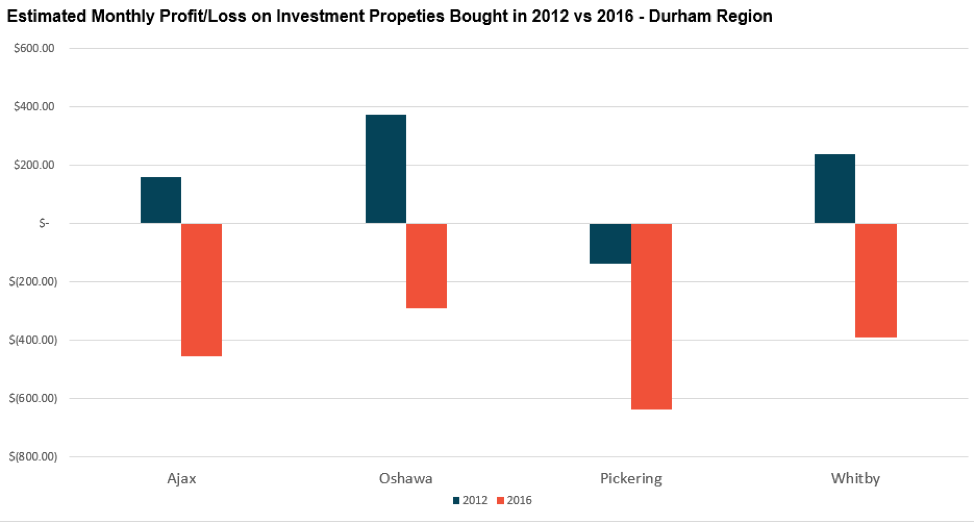

In 2012, three out of the four municipalities in Durham region had an average monthly profit on the real estate investments purchased that year.

Oshawa, Whitby

Rising house prices have wiped out all average profits for investment properties in 2016 for each of the municipalities.

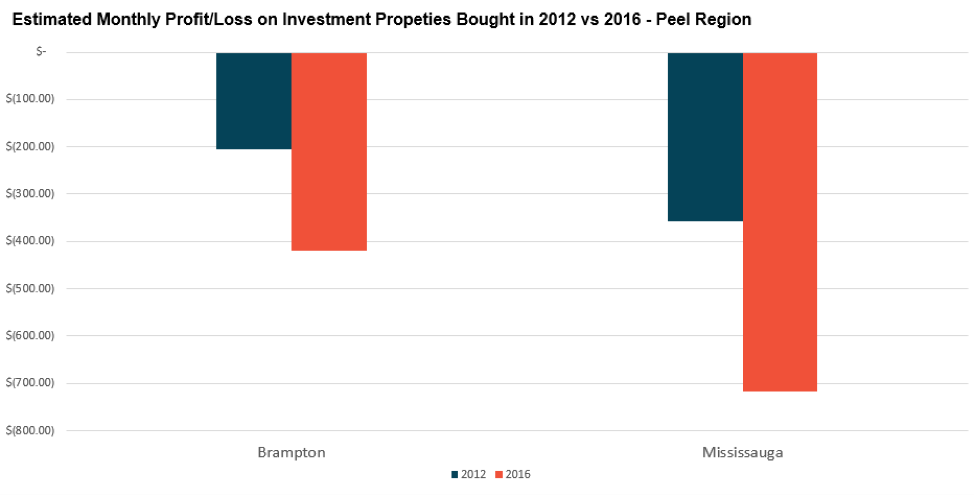

Brampton and Mississauga both saw their average monthly loss on investment properties double in the four years from 2012 to 2016.

The average monthly loss in Brampton increased from $205 in 2012 to $418 in 2016. The average monthly loss in Mississauga increased from $358 in 2012 to $718 in 2016.

Toronto saw the average monthly loss on investment properties increase from $571 per month in 2012 to $1,384 in 2016.