LIVE MARKET UPDATE: WATCH REPORT HIGHLIGHTS & Q/A - THURSDAY APRIL 11th 12PM ET

Join John Pasalis, report author, market analyst and President of Realosophy Realty, in a free monthly webinar as he discusses key highlights from this report, with added timely observations about new emerging issues, and answers your questions. A must see for well-informed Toronto area real estate consumers.

WATCH NOW: John talks about the latest monthly numbers

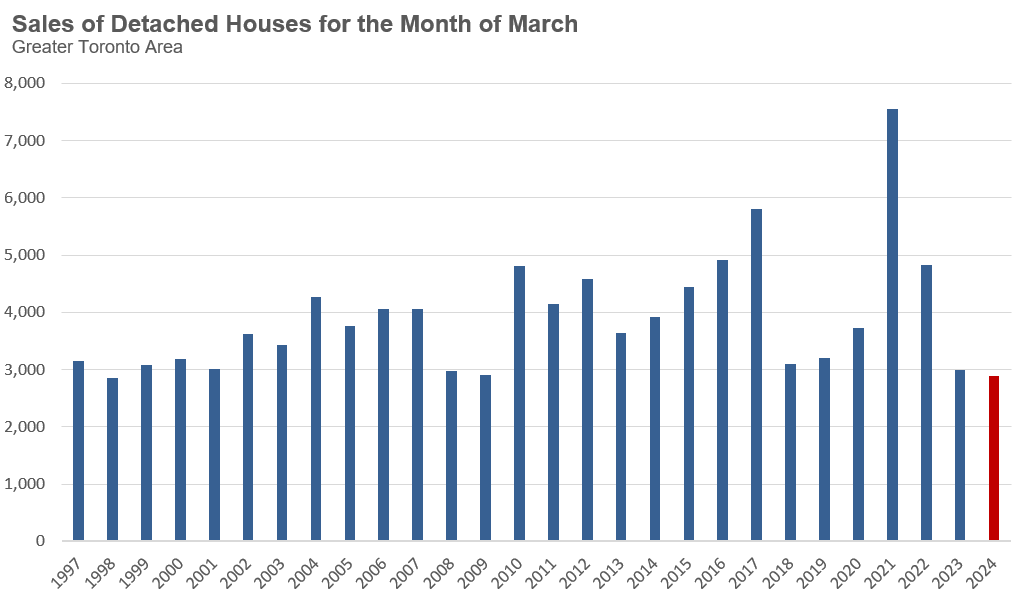

High home prices and high interest rates have kept many home buyers on the sidelines, resulting in a record low volume of sales for detached homes in the month of March.

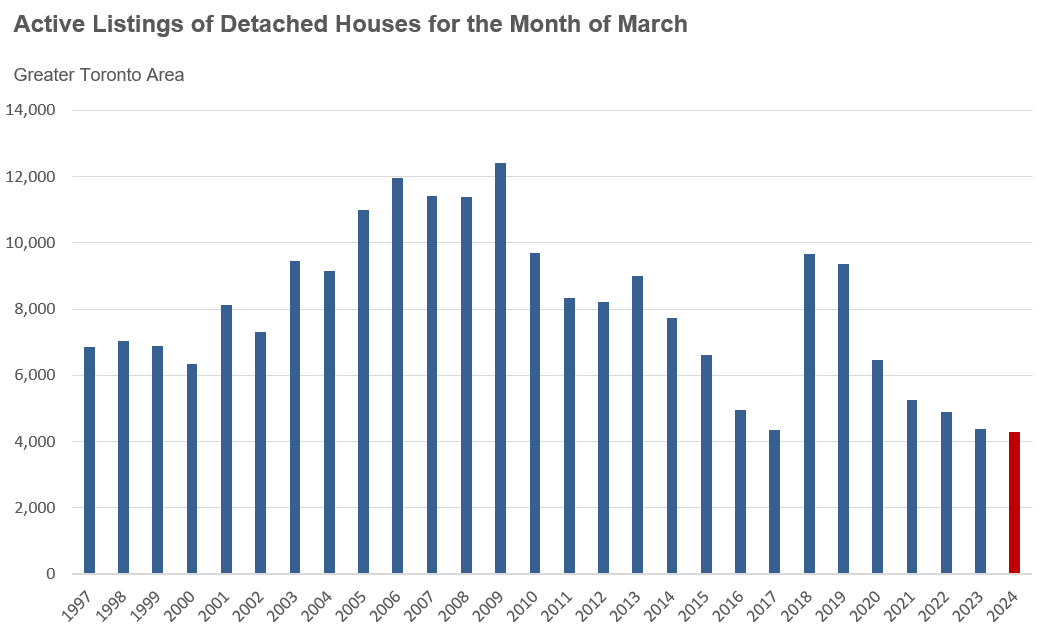

However, despite the low sales volume, the market for detached homes remained competitive because the number of detached homes available for sale also reached a record low in March.

The low inventory levels can, at least in part, be explained by the low sales volumes. Far fewer people are upsizing in today's higher interest rate environment, which means they are not buying a home and are not selling their existing home, leading to a decline in sales and active listings.

However, the other structural change we are seeing in the housing market is that more people are moving out of their existing homes, either due to upsizing or relocation, and not selling their existing homes. They are holding their existing homes as investment properties.

Over time, this has reduced the stock of homes that can be purchased by people who intend to use them as their principal residence. This means that the declining number of resale homes available for sale every year isn't a symptom of a lack of supply but the result of the increasing share of homes bought by investors who convert the homes to rental properties.

Politicians and housing experts often dismiss the role that real estate investors play in our housing market. In doing so, they ignore their impact on housing affordability in Canada and the significant change in the role that houses play in Canada's society and political economy.

Owning a home provided families with certainty and security in their housing needs and an investment that could help fund their future retirement. As Canada sees more homes bought by investors, a generation of Canadians is being shut out of owning a home, which means they are losing the housing security previous generations had and that long-term investment to help fund their retirement.

By the Numbers: March 2024

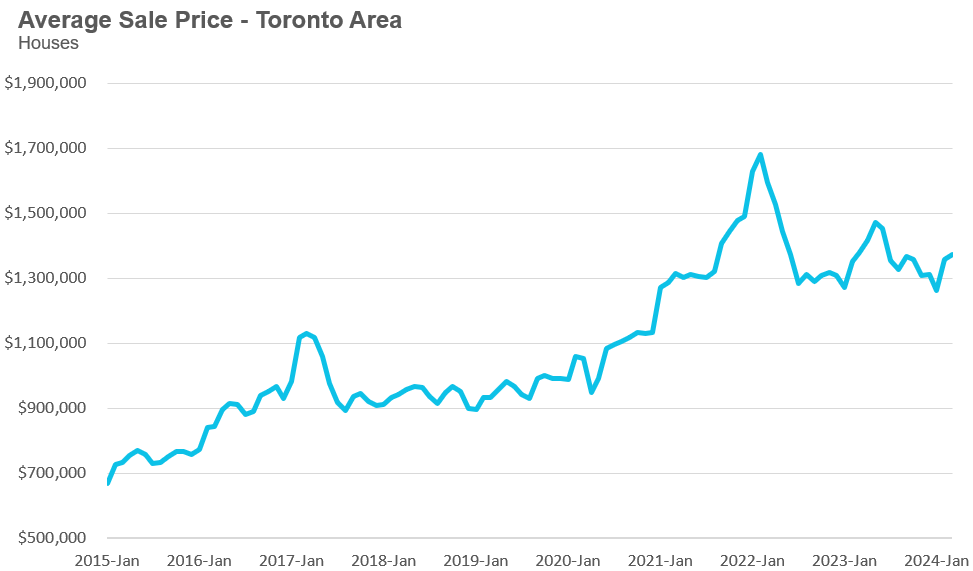

The average price for a house in the Toronto area was $1,373,316 in March, unchanged over the same month last year. Last month's median house price was $1,218,500, also unchanged over last year.

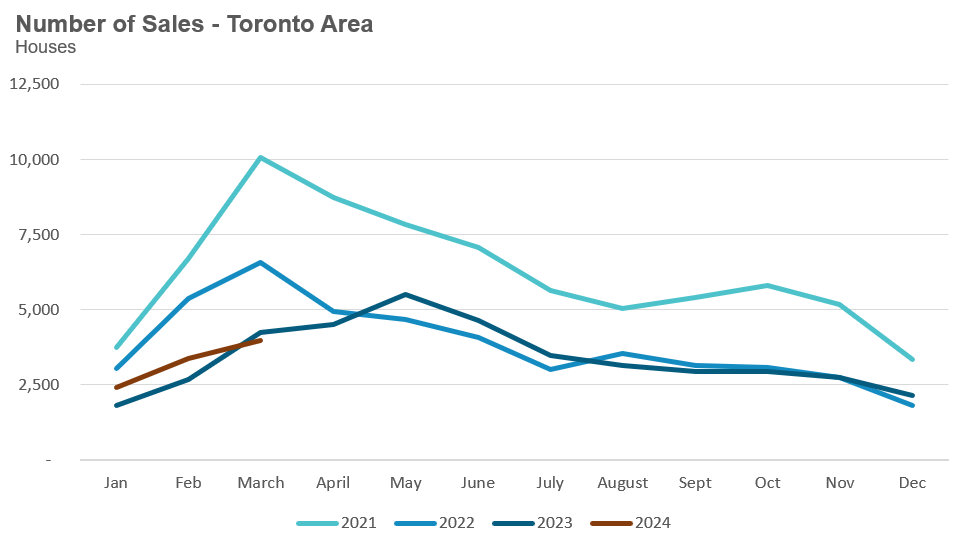

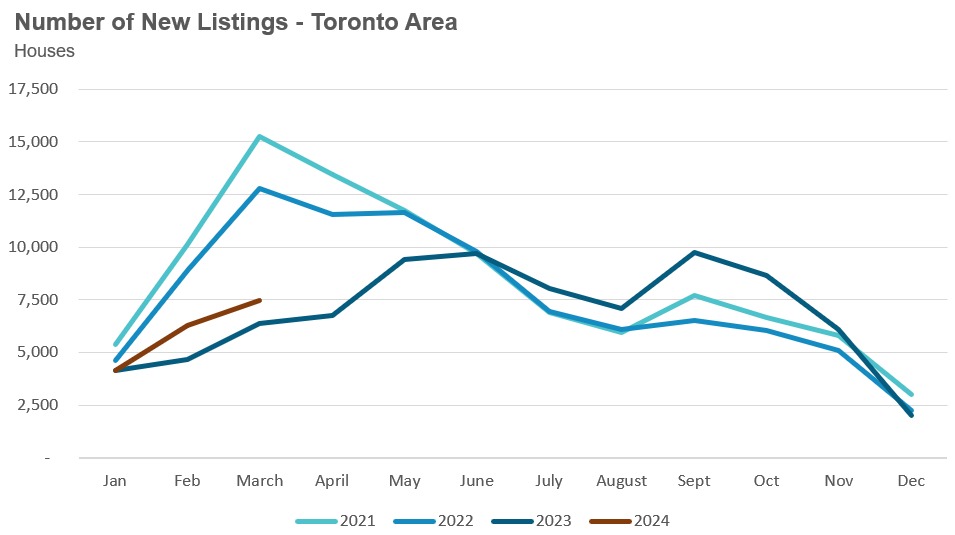

House sales in March were down 6% over last year, while new house listings were up 17%.

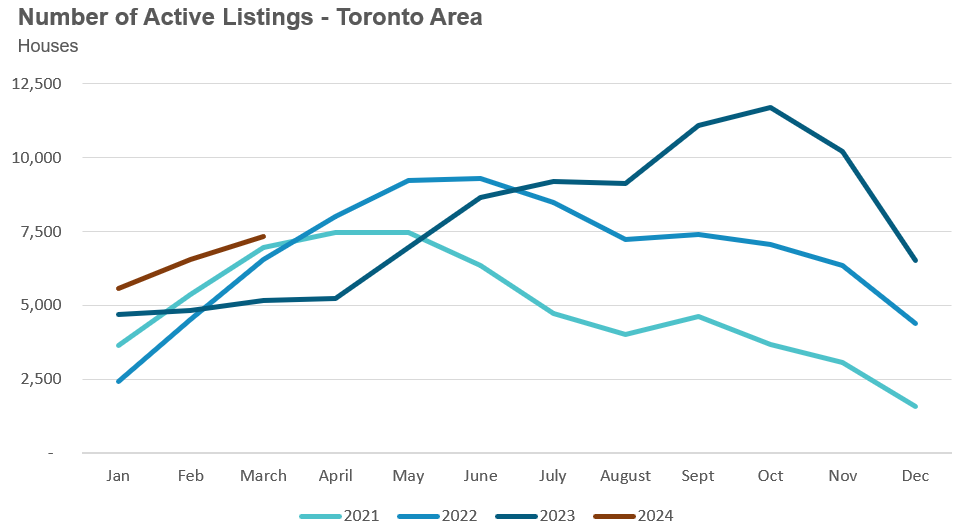

The number of houses available for sale at the end of the month, or active listings, was up 42% over last year.

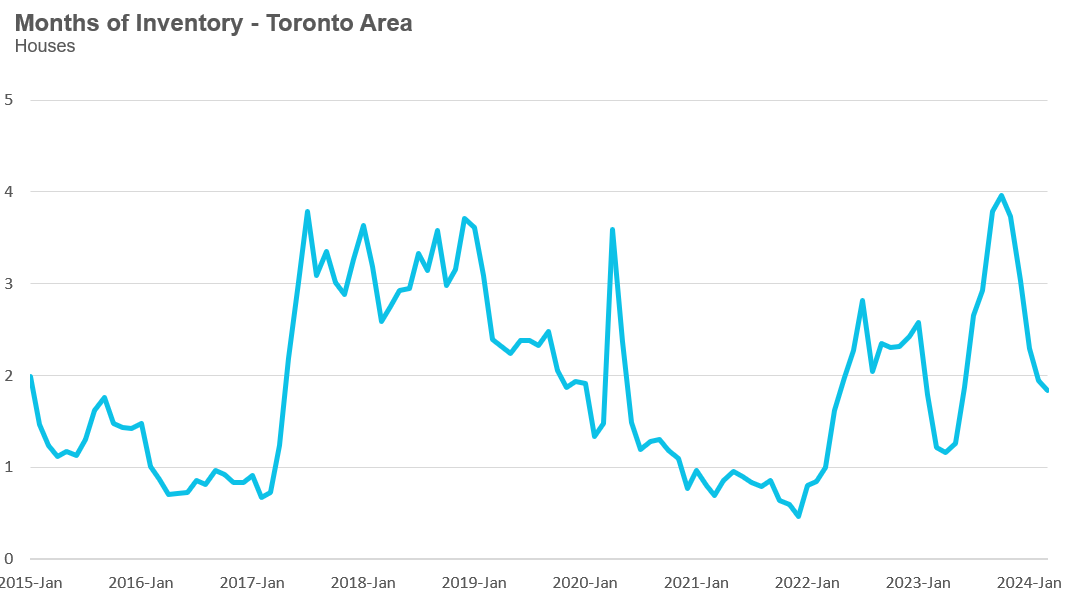

The current balance between supply and demand is reflected in the MOI, which is a measure of inventory relative to the number of sales each month.

In March, the MOI for houses fell slightly to 1.8.

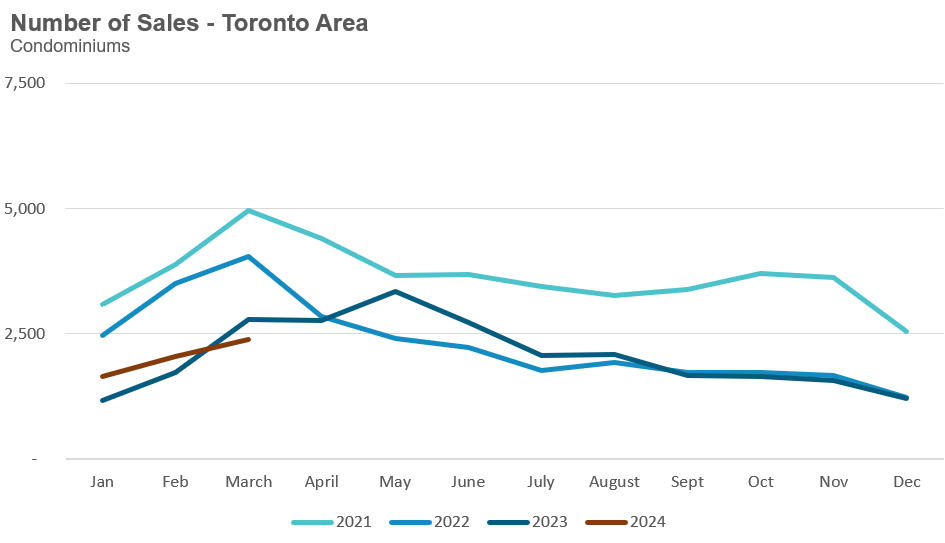

The average price for a condo in the Toronto Area was $728,585 in March, which is unchanged over last year. The median price for a condo in March was $670,000, up 1% over last year.

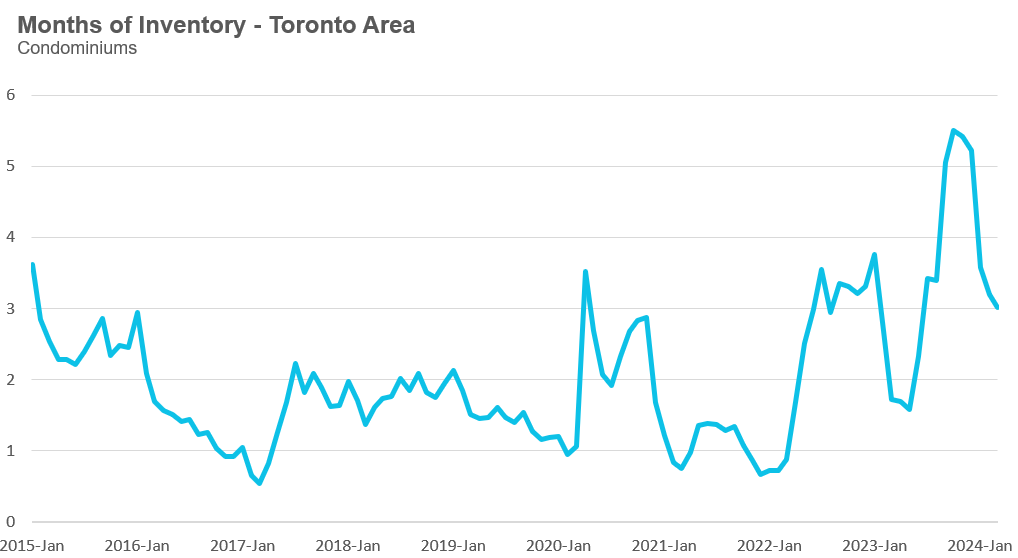

Condo sales in March were down 15% over last year, and new condo listings were up 19% over last year. The number of active condo listings was up 49% over last year. The MOI decreased slightly to 3.

Browse detailed monthly statistics for March 2024 for the entire Toronto area market, including house, condo and regional breakdowns at the .

WATCH NOW: John talks about Federal Government's change to immigration policy

Last week, Canada’s immigration minister, Marc Miller, announced that the Liberal federal government plans to reduce the number of non-permanent residents (NPR) in Canada from the current 6.2% share of total population to 5% over the next three years.

Ten years ago, NPRs made up roughly 2% of Canada’s population, and since then, the surge in NPRs has contributed to Canada’s rapid population growth.

On the surface, this reduction doesn’t sound like a noteworthy announcement that will have much of an impact, but a closer look at the data makes it clear that this is a significant shift in policy and one that will have wide-reaching effects, particularly on the housing market.

The number of NPRs in Canada in the fourth quarter of 2022 was roughly 1.7 million (M), which increased to just over 2.5M a year later, an 800,000 (800K) increase. For the federal government to reduce the portion of NPRs to 5% of the population, the number of NPRs in Canada would have to decline by around 450K people over the next three years.

While this change may not have a drastic effect on the number of NPRs in Canada immediately, it will have a significant effect on how quickly Canada’s population grows each year. Over the next three years, while roughly 450K people will arrive in Canada due to net immigration of permanent residents, a corresponding decline of roughly 150K non-permanent residents will result in Canada’s population growing by roughly 300K people each year. This means that Canada’s population, which grew by 1.2M in a single year last quarter, may grow by only 300K per year 12 months from now.

This graph outlines Canada’s population growth each year and the projected growth if the Liberals achieve their target.

This dramatic change in managing Canada’s population growth is a significant change in approach by Liberal federal government, one that is a game-changer for our housing affordability crisis.

For years, the Liberals have argued that Canada’s housing crisis is due to a lack of supply and that the only solution is to build more homes, the same argument many industry experts have been making for years. By insisting on supply-side only solutions, and ignoring any calls to better manage demand for housing (which includes increased demand from rapid population growth), the government and many experts have been suggesting that Canada could restore affordability by tripling the number homes built over the next ten years, a massive increase in supply from the current average of just over 200K homes built yearly since the 1990s.

Bank of Montreal economists Doug Porter and Robert Kavcic were among the few economists to disagree, rightly arguing that ramping up housing supply takes a very long time, due to need to increase available labour, amongst other challenges, and that to address housing affordability in the short term, policymakers need to look at better managing the demand for housing.

In a recent interview, Kavcic had this to say about the federal government’s change to NPR target numbers:

“This is attacking the demand curve now, which is a complete change in philosophy for policy makers, and one that we think is actually going to work.”

Kavcic is correct; assuming these targets are reached, this approach is actually going to work — but it’s important to note that this doesn’t mean that houses will suddenly be more affordable in the near-term.

By reducing Canada’s annual population growth rate, the federal government is achieving several important goals.

Canada’s previous approach to the housing crisis, which focused only on trying to increase supply while our population continued to grow far more rapidly ensured that our housing shortage and affordability crisis would only get worse each year.

Reducing Canada’s population growth to roughly 300K people per year will take some pressure off home price appreciation in the years to come. Canada will still have a housing shortage, but the shortage will not be getting worse each year, and, in fact, housing completions are likely to outpace population growth which means Canada will be gradually reducing its overall shortage.

This is not an immediate solution to our housing affordability crisis, but is a correct and necessary first step.

I also believe that this change in approach will resonate far more with all who are increasingly concerned about housing affordability, particularly as supply targets continued to be missed as our population reached a record high growth over the past few years.

House sales (low-rise freehold detached, semi-detached, townhouse, etc.) in the Greater Toronto Area (GTA) in March 2023 were down 6% compared to the same month last year.

New house listings in March were 17% compared to last year.

The number of houses available for sale (“active listings”) was up 42% in March compared to the same month last year.

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number of homes sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell, given the current level of demand? The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

While the current level of MOI gives us clues into how competitive the market is on-the-ground today, the direction it is moving in also gives us some clues into where the market may be heading.

The MOI for houses dipped to 1.8 in March, down from 4 MOI in October.

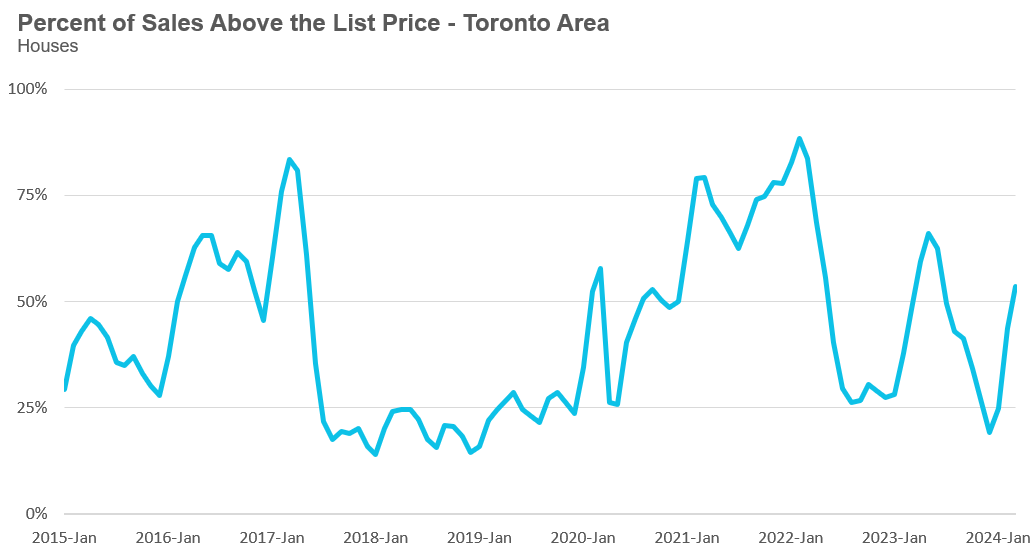

The share of houses selling for more than the owner’s list price increased to 54% in March.

The average price for a house in March was $1,373,316 in March 2024, unchanged compared to the same month last year.

The median house price in March was $1,218,500, unchanged over last year.

The median is calculated by ordering all the sale prices in a given month and then selecting the price at the midpoint of that list such that half of all home sales are above that price and half are below that price. Economists often prefer the median price over the average because it is less sensitive to big increases in the sale of high-end or low-end homes in a given month, which can skew the average price.

Condo (condominiums, including condo apartments, condo townhouses, etc.) sales in the Toronto area in March 2023 were down 15% over the same month last year.

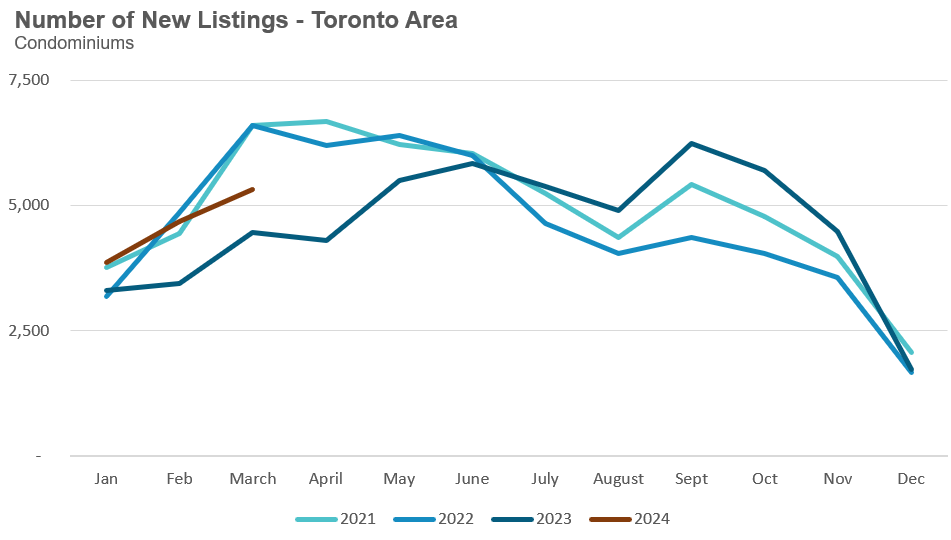

New condo listings were up 19% in March over last year.

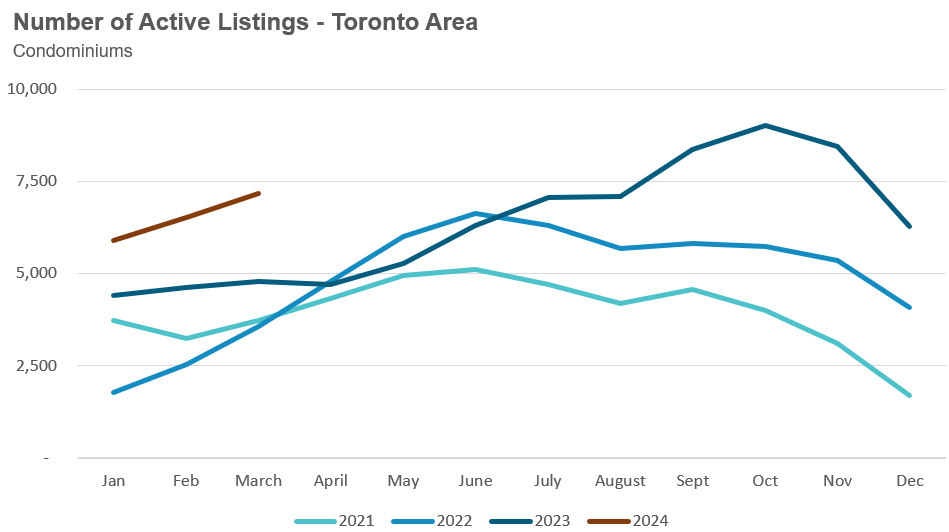

The number of condos available for sale at the end of the month, or active listings, was up 49% over last year.

Condo months of inventory decreased slightly to 3 MOI in March.

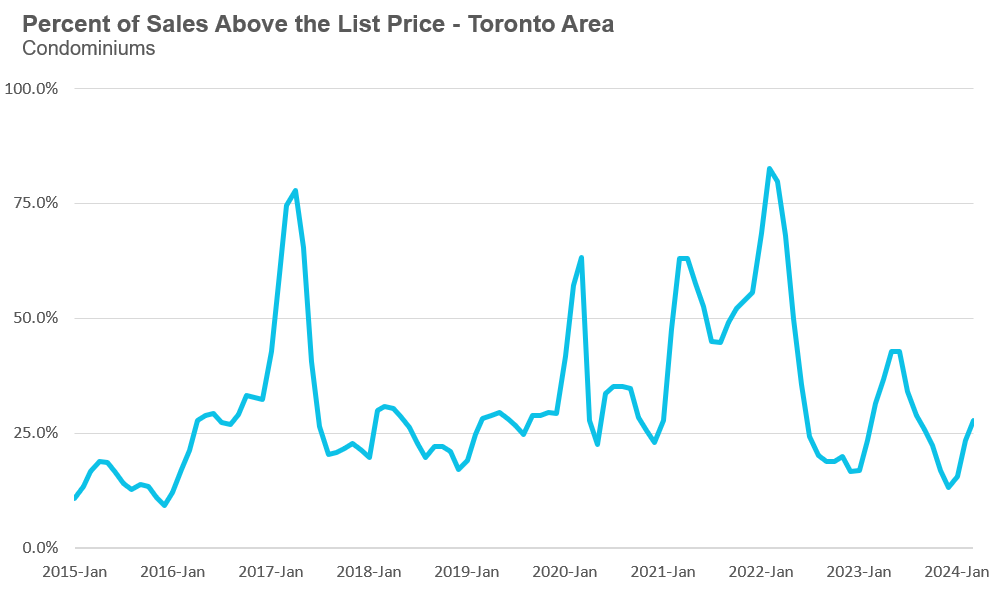

The share of condos selling for over the asking price increased to 27% in March.

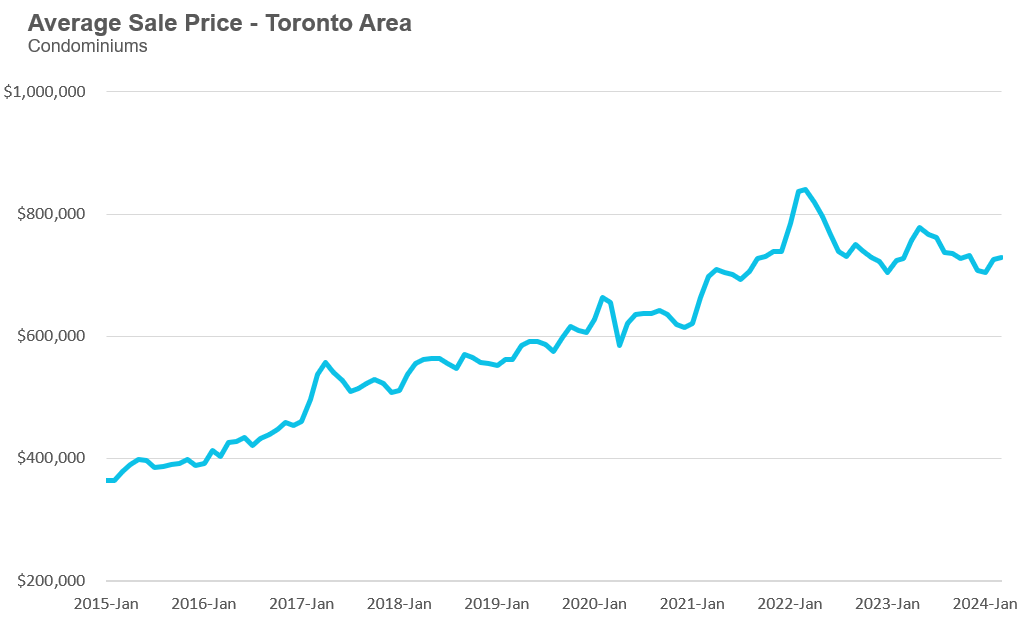

The average price for a condo in March was $728,585, unchanged over last year. The median price for a condo in March was $670,000, up 1% over last year.

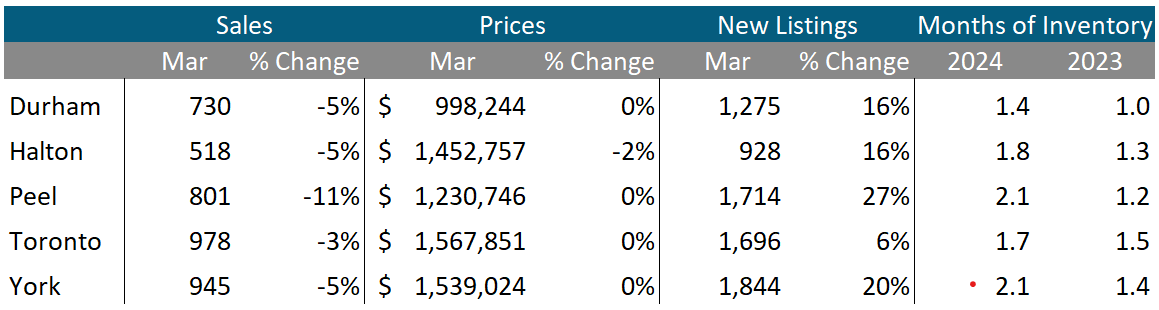

Houses

All five regions saw sales decline over last year. Halton saw average prices decrease by 2%, while all other regions saw no change in average prices. All five regions saw significant increases in new listings in March, while the MOI was above last year.

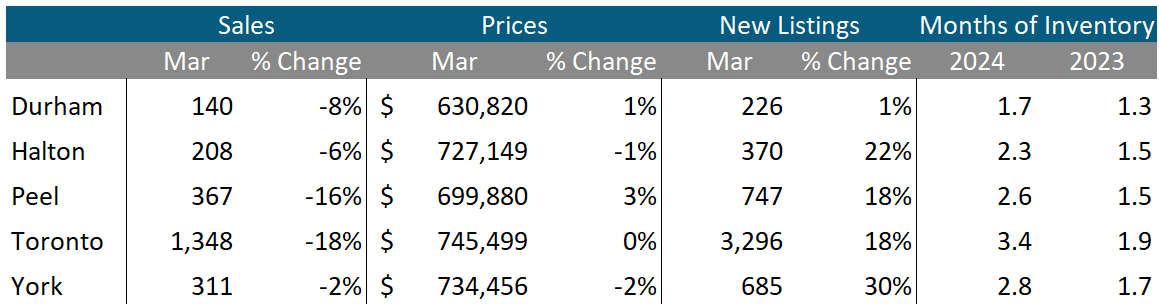

Condos

Condo sales were down in all five regions in March. Average prices were down in Halton and York, unchanged in Toronto and up slightly in Durham and Peel. The MOI is above last year’s level for all regions.

See Market Performance by Neighbourhood Map, All Toronto and the GTA

Greater Toronto Area Market Trends