LIVE MARKET UPDATE: WATCH REPORT HIGHLIGHTS & Q/A - THURSDAY AUGUST 14th 12PM ET

Join John Pasalis, report author, market analyst and President of Realosophy Realty, in a free monthly webinar as he discusses key highlights from this report, with added timely observations about new emerging issues, and answers your questions. A must see for well-informed Toronto area real estate consumers.

WATCH THIS STORY NOW: Will Prices Fall and Other Key Questions About Toronto's Condo Market

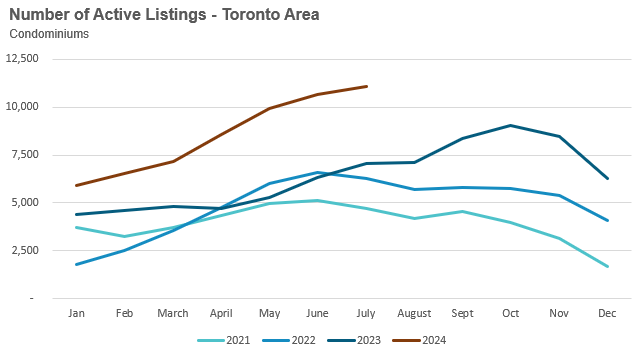

The Greater Toronto Area has a record 11,079 condominium units available for sale, the highest number of units for any month in any year.

With nearly six months of inventory, the condominium (condo) market is in buyer’s market territory, but prices remain relatively flat (average condo prices were down a modest 3% in July over last year).

One question I keep getting from readers is why Toronto condo prices haven’t seen a more dramatic decline and whether we should expect a bigger drop in the future.

While nobody has the answers to these questions, I’ll do my best to offer some factors that might explain the relative stability in condo prices and things we’ll want to keep an eye on in the months ahead.

The charts I’m going to present in this section consider the number of active condo listings, condo sales, and new listings in the Greater Toronto Area since 2013. To remove the high volatility caused by seasonal differences in sales and listing volumes, I will use a 12-month rolling average of the data which takes the average number of listings or sales over the previous 12 months.

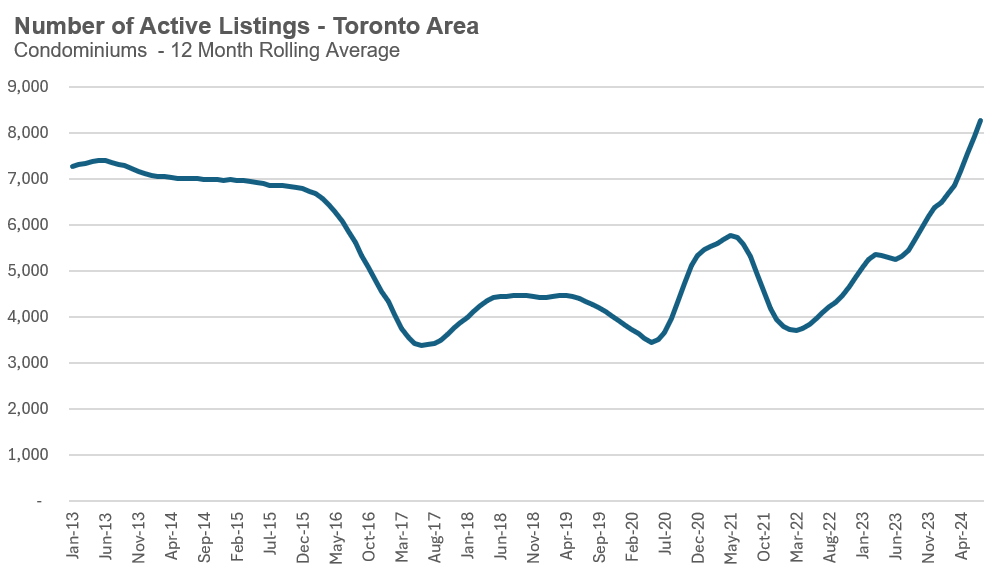

The chart below shows the 12-month average number of active condominium listings (inventory) in the Greater Toronto Area, which we can see continues to reach new record highs.

The number of active listings on the market is a function of the number of new listings coming on the market for sale and the number of sales in any given month. Even if new listing volumes are in line with historical trends, active listings can accelerate if the demand for condos (sales numbers) falls dramatically. If fewer people are buying condos, the inventory of condos for sale gradually increases.

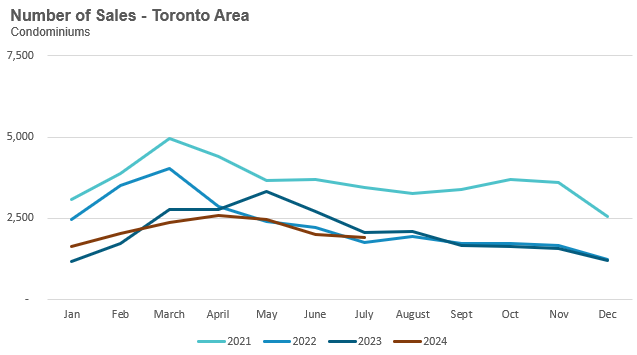

The chart below shows the 12-month average number of condominium sales in the Greater Toronto Area, which we can see is at the lowest level in over a decade.

A big factor behind the surge in active condo listings is that far fewer people are buying condos these days. Fewer end-users are looking to buy a condo at today’s prices and interest rates, and investors have largely stopped buying rental condos in today’s market. As sales fall, inventory gradually builds up.

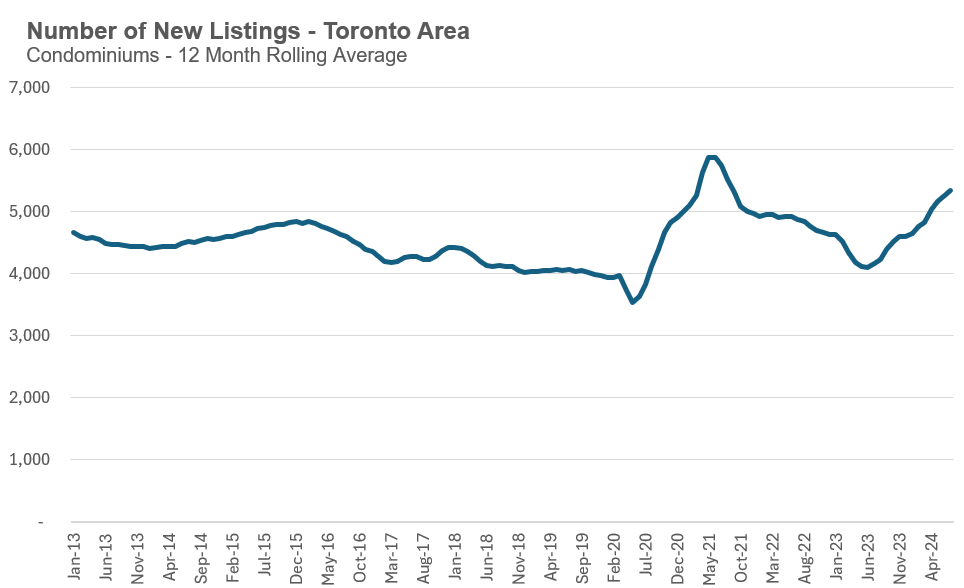

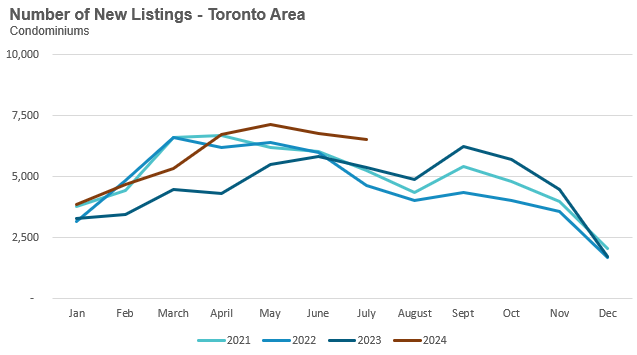

The chart below shows the 12-month average number of new condominium listings.

The average number of new listings over the previous 12 months is relatively high, but only modestly above the volumes in 2021 and early 2022.

This suggests that the sharp increase in active listings is driven by a sharp decline in buyer demand and an above-average increase in the number of listings coming on the market for sale.

Returning to our original question, given these conditions - why aren’t prices falling?

Firstly, it’s important to remember that home prices tend to be sticking on the way down. Sellers are typically slow at reducing their prices and are more inclined to just wait for the market to give them the price they want.

But I suspect that a big reason why investors in Toronto are slow to dramatically reduce their prices is that most are optimistic that the condo slowdown we are experiencing is a short-term trend that they need to wait out. Since most of the inventory buildup is due to very low sales volumes, many feel that upcoming rate cuts will move buyers and investors from the sidelines to buy a condo which should improve market conditions.

Of course, if the Bank of Canada cuts rates aggressively in the near term, it would be because Canada’s economy is worsening faster than expected, which may not result in the sudden surge in demand that many are hoping for. The eventual rebound in demand for Toronto condos is more likely to be gradual vs. sudden.

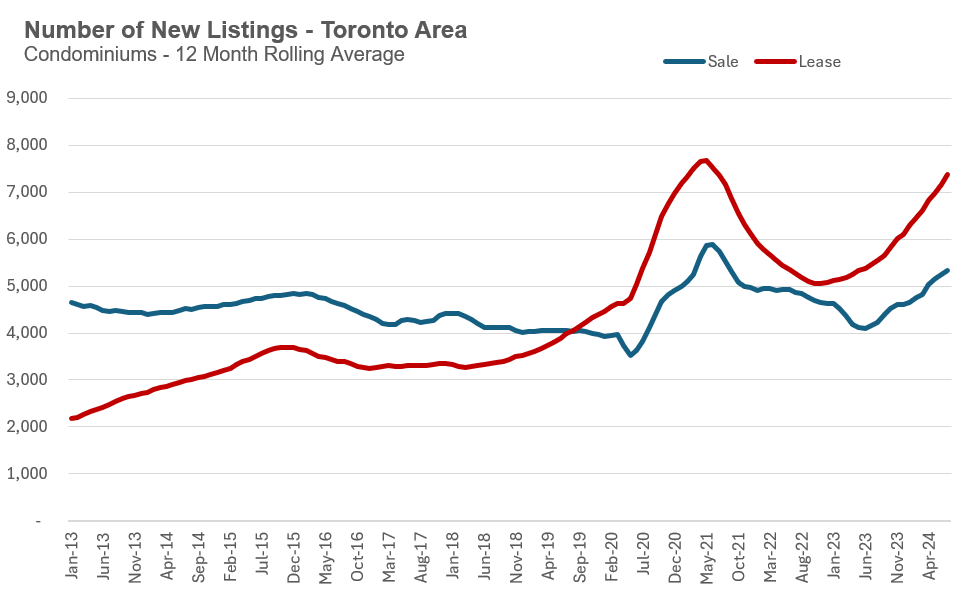

Finally, as some of our clients begin to consider taking their condos off the market for sale and opting to rent them out instead, I thought it would be interesting to compare the average number of new listings for condos for sale vs. condos for lease.

The surge in condo rental listings is even more dramatic than the spike in condominiums listed for sale. This trend matters because as long as investors are willing to wait out this slow market and, in some cases, opt to rent their units instead of selling them, we may not see as much downward pressure on condo prices as some buyers are hoping for.

On the other hand, if an increasing number of condo owners need to sell and can’t afford to keep their condos as rentals, we may see downward pressure on prices if condo inventory continues to increase in the months ahead.

By the Numbers: July 2024

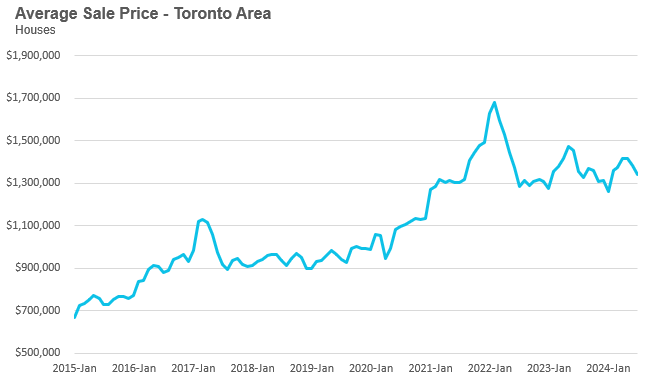

The average price for a house in the Toronto area was $1,338,418 in July, down 1% from the same month last year. Last month's median house price was $1,150,000, down 3% from the same month last year.

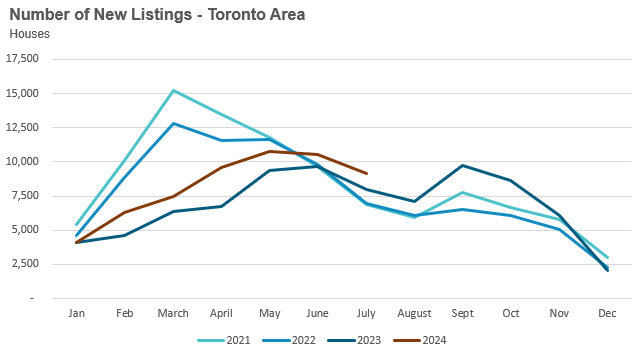

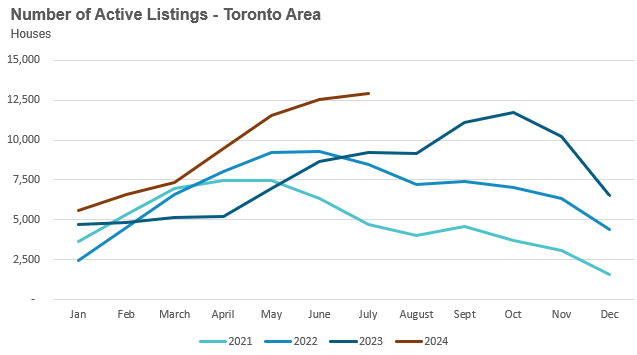

House sales in July were down 4% over last year, while new house listings were up 14%. The number of houses available for sale at the end of the month, or active listings, was up 41% over last year.

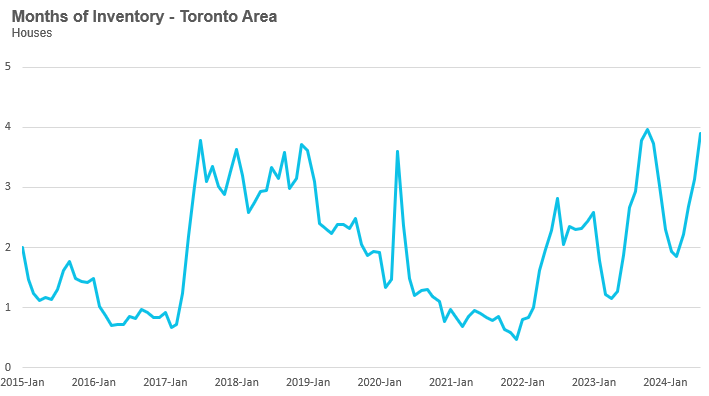

The current balance between supply and demand is reflected in the months-to-inventory ratio (MOI), which measures inventory relative to the number of sales each month. In July, the MOI for houses increased slightly to 3.9.

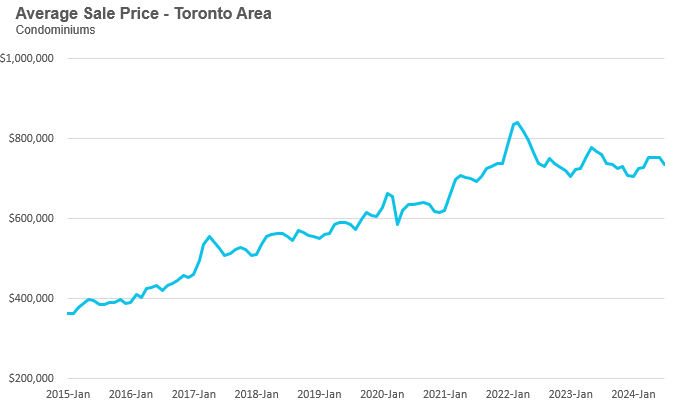

The average price for a condo in the Toronto Area was $736,850 in July, down 3% from the previous year. The median price for a condo in July was $665,000, down 4% from the previous year.

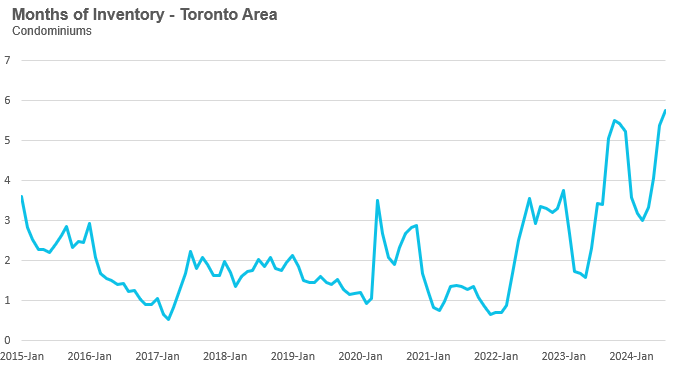

Condo sales in July were down 7% from last year, but new condo listings were up 21%. The number of active condo listings was up 57% from last year and reached a new record of 11,079 for any month. The MOI increased to 5.8.

Browse detailed monthly statistics for July 2024 for the entire Toronto area market, including house, condo and regional breakdowns below.

“Only government intervention could ensure that all Canadians, regardless of where they lived, had the same rights, privileges and living standards. And that’s what my corporation is all about today: pursuit of that public policy purpose.”

- George Anderson, CMHC

House sales (low-rise freehold detached, semi-detached, townhouse, etc.) in the Greater Toronto Area (GTA) in July 2024 were down 4% compared to the same month last year.

New house listings in July were up 14% compared to last year.

The number of houses available for sale (“active listings”) was up 41% in July compared to the same month last year.

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number of homes sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell, given the current level of demand? The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

While the current level of MOI gives us clues into how competitive the market is on-the-ground today, the direction it is moving in also gives us some clues into where the market July be heading.

The MOI for houses increased to 3.9 in July.

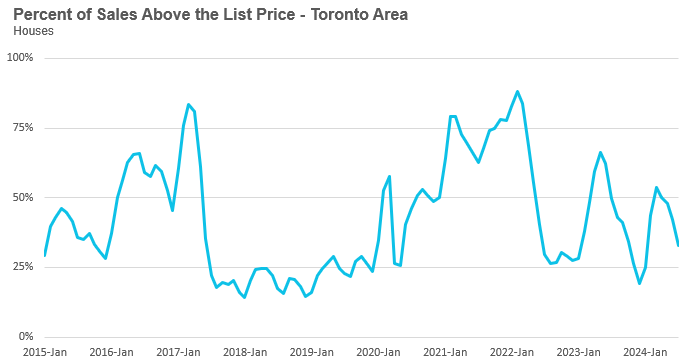

The share of houses selling for more than the owner’s list price decreased to 33% in July.

The average price for a house in July 2024 was $1,338,418, down 1% from the same month last year.

The median house price in July was $1,150,000, down 3% over last year.

The median is calculated by ordering all the sale prices in a given month and then selecting the price at the midpoint of that list such that half of all home sales are above that price and half are below that price. Economists often prefer the median price over the average because it is less sensitive to big increases in the sale of high-end or low-end homes in a given month, which can skew the average price.

Condo (condominiums, including condo apartments, condo townhouses, etc.) sales in the Toronto area in July 2024 were down 7% compared to the same month last year.

New condo listings were up 21% in July over last year.

The number of condos available for sale at the end of the month, or active listings, was up 57% over last year.

Condo months of inventory increased to 5.8 MOI in July.

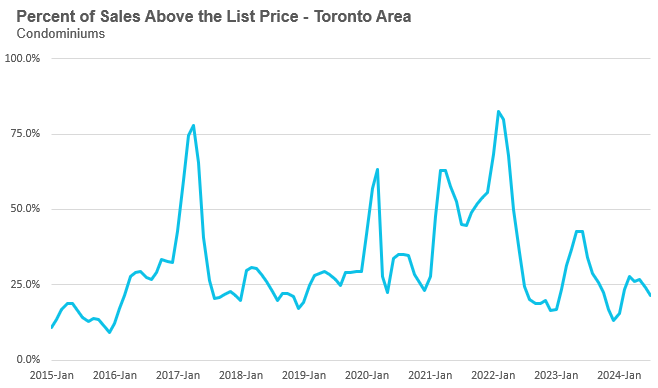

The share of condos selling for over the asking price increased slightly to 21% in July.

The average price of a condo in July was $736,850, down 3% from last year. The median price was $665,000, down 4% from last year.

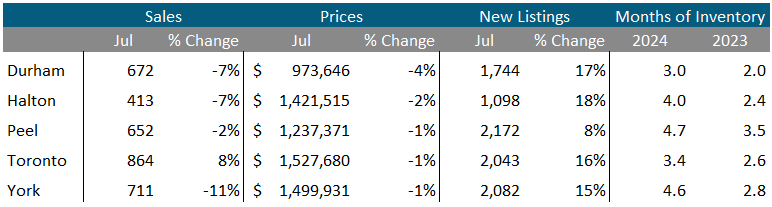

Sales were up by 8% in Toronto, but down in the GTA’s four suburban regions. Average prices were down modestly across all five regoins. New listings were up by 8% in Peel and over 15% in the other four regions. Months of inventory was up across all regions, with Peel (4.7) and York (4.6) seeing the highest MOI of houses in the Greater Toronto Area.

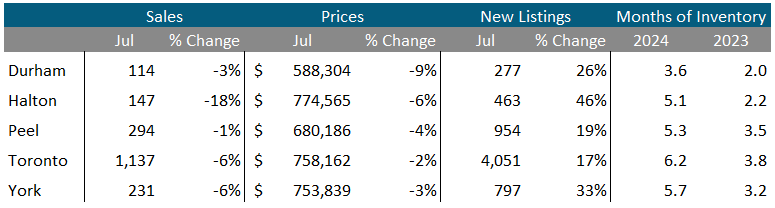

Condo sales were down in all five regions with Halton seeing the biggest decline. Average prices were also down across the GTA with Durham seeing the sharpest decline at 9%. New listings and MOI were well above last year’s level for all regions. The City of Toronto has the highest MOI across all five regions.

See Market Performance by Neighbourhood Map, All Toronto and the GTA

Greater Toronto Area Market Trends