WATCH NOW: Mixed Signals Amidst Sales Growth - Toronto Housing Market November 2024

Toronto's housing market in November 2024 painted a complex picture, balancing robust sales activity against lingering sluggishness due to high inventory levels. Here's a closer look at the key trends:

Strong Sales Growth but Persistent Sluggishness

House and condo sales surged year-over-year, reflecting increased buyer activity spurred by lower borrowing costs. However, the relatively high number of active listings continued to dampen market momentum. This glut of inventory is keeping market conditions less competitive despite a decline in the months of inventory (MOI), which measures the balance between supply and demand.

Moderation in Competition

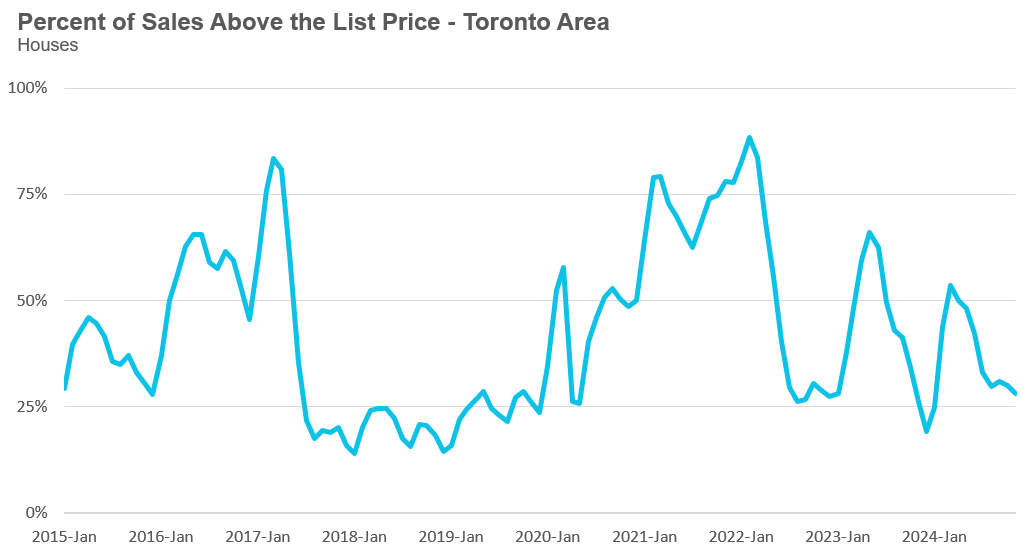

The decrease in MOI from earlier in the fall has not significantly intensified competition. The percentage of homes selling over the asking price has remained stable, signaling a market where buyers still hold some negotiation power. This restrained competitiveness is contributing to longer-than-usual days on the market for many listings.

Diverging Price Trends for Houses and Condos

House and condo prices moved in opposite directions in November 2024. House prices increased by 5% year-over-year, driven by sustained demand for detached homes, particularly in Toronto’s urban areas. Condo prices declined by 4% annually as high inventory levels and cautious investor sentiment weighed on this segment. Buyers continue to have leverage, with ample options and steady price declines.

The Toronto housing market remains in flux, offering opportunities for buyers and challenges for sellers in an evolving landscape.

LIVE MARKET UPDATE: WATCH REPORT HIGHLIGHTS & Q/A - THURSDAY DECEMBER 12th 12PM ET

Join John Pasalis, report author, market analyst and President of Realosophy Realty, in a free monthly webinar as he and his guests discus key highlights and answers your questions. A must see for Toronto area real estate consumers!

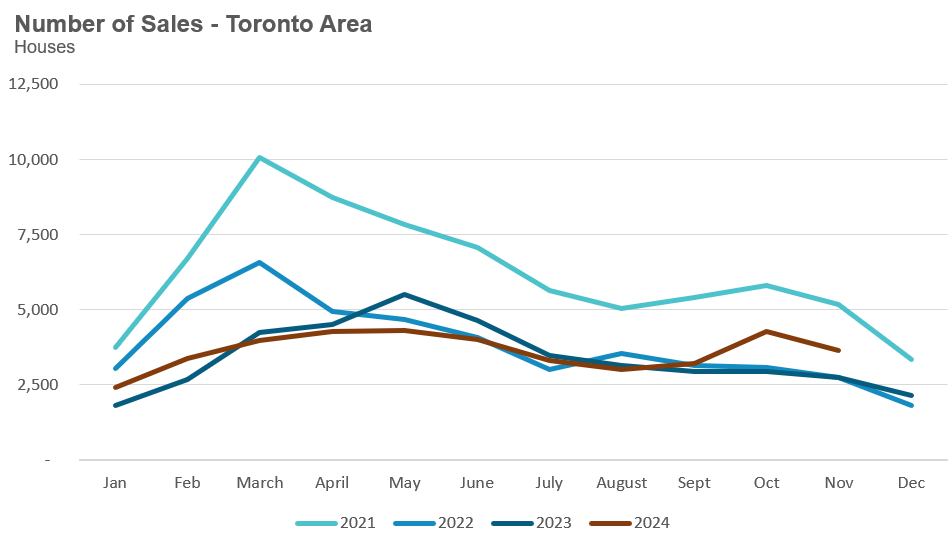

Houses

House sales (low-rise freehold detached, semi-detached, townhouse, etc.) in the Greater Toronto Area (GTA) in November 2024 were up 34% compared to the same month last year.

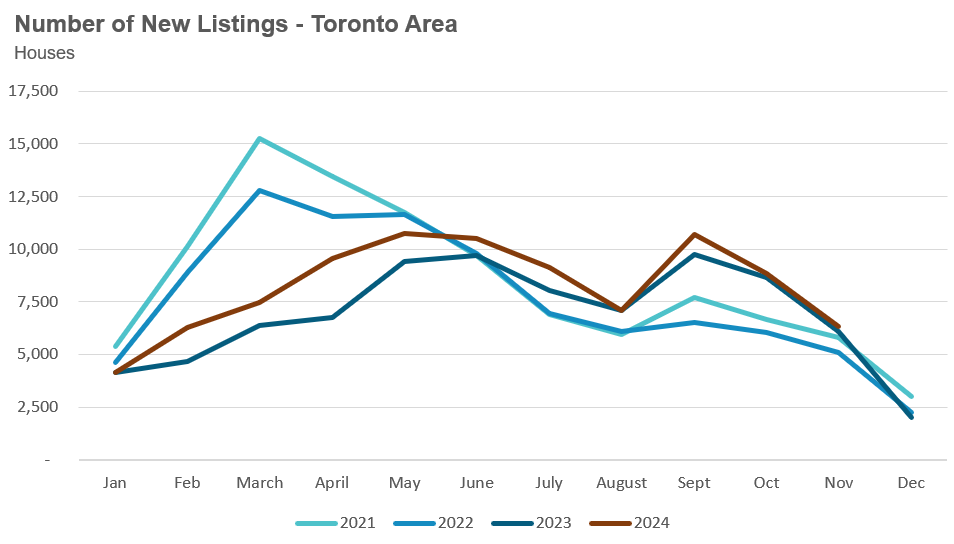

New house listings in November were up 4% compared to last year.

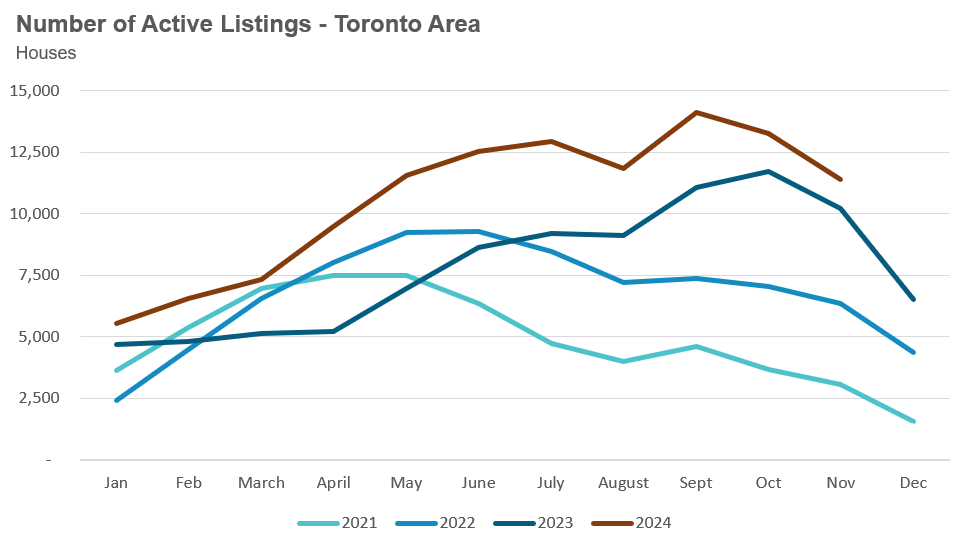

The number of houses available for sale (“active listings”) was up 12% in November compared to the same month last year.

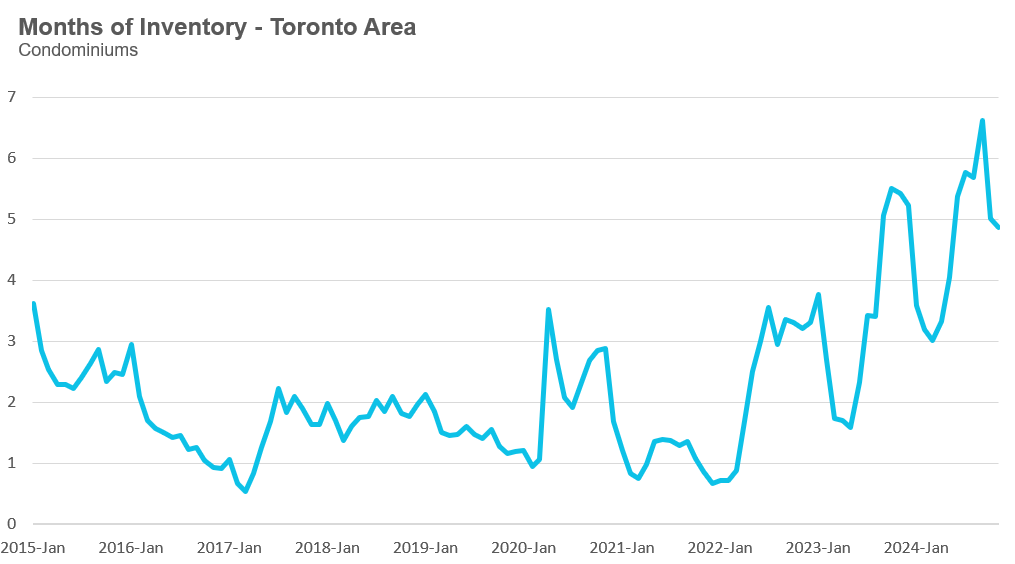

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number of homes sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell, given the current level of demand? The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

While the current level of MOI gives us clues into how competitive the market is on-the-ground today, the direction it is moving in also gives us some clues into where the market November is heading.

The MOI for houses was unchanged at 3.1 for November.

The share of houses selling for more than the owner’s list price fell to 28% in November.

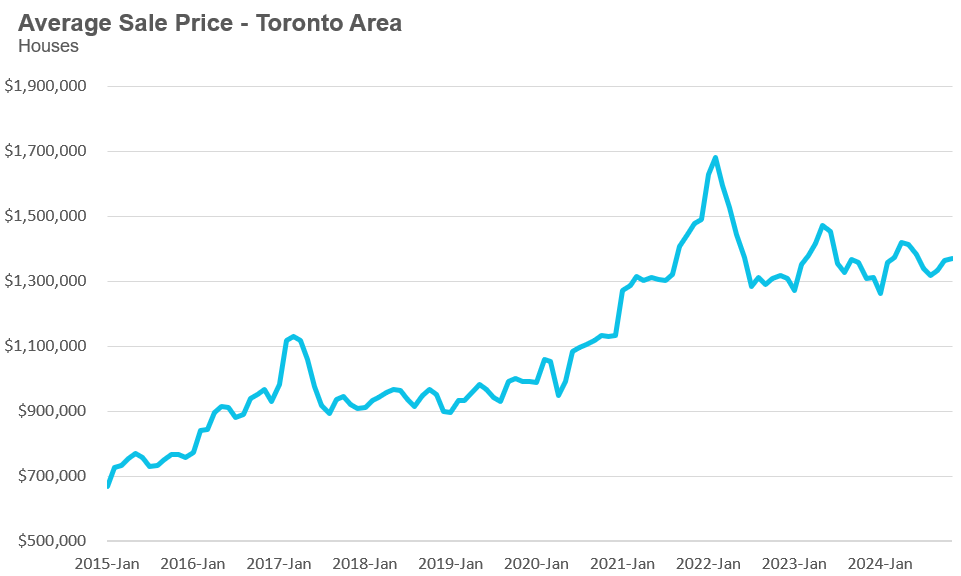

The average price for a house in November 2024 was $1,370,641, up 5% from the same month last year.

The median house price in November was $1,171,000, up 3% over last year.

The median is calculated by ordering all the sale prices in a given month and then selecting the price at the midpoint of that list such that half of all home sales are above that price and half are below that price. Economists often prefer the median price over the average because it is less sensitive to big increases in the sale of high-end or low-end homes in a given month, which can skew the average price.

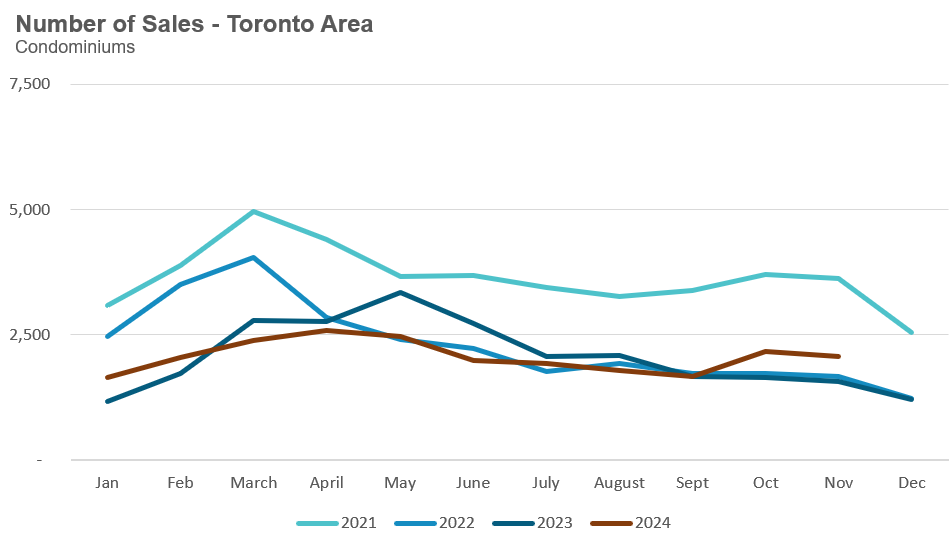

Condo (condominiums, including condo apartments, condo townhouses, etc.) sales in the Toronto area in November 2024 were up 32% compared to the same month last year.

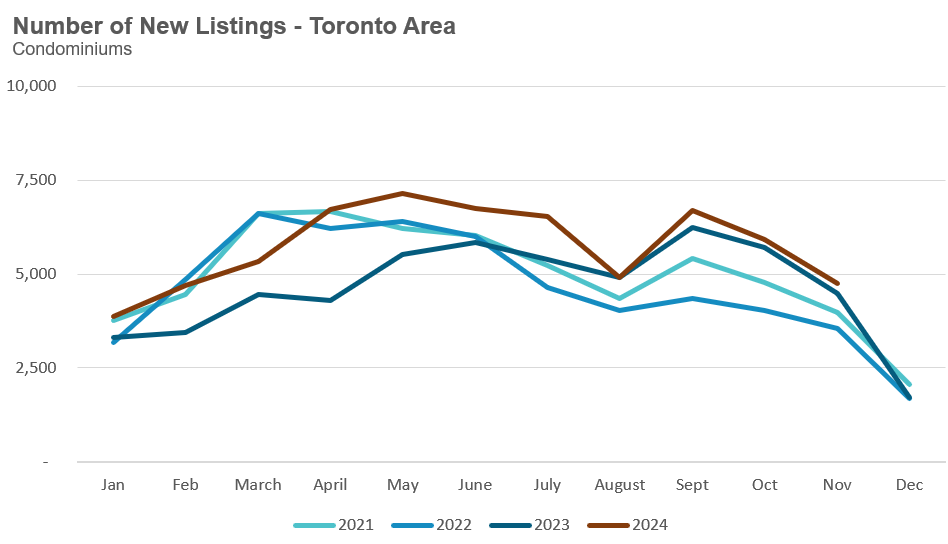

New condo listings were up 6% in November over last year.

The number of condos available for sale at the end of the month, or active listings, was up 19% over last year.

Condo months of inventory decreased to just under 5 MOI in November.

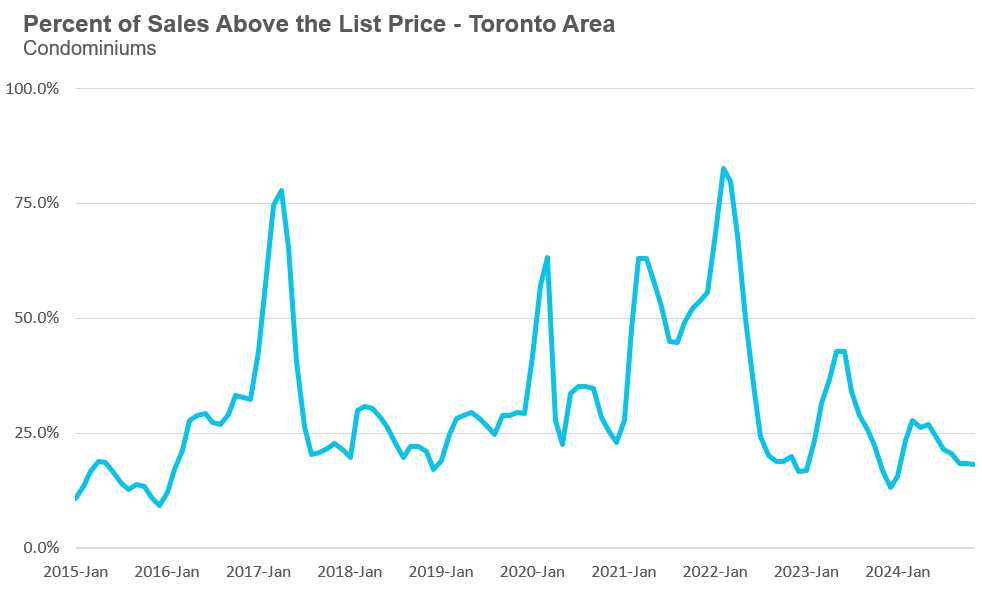

The share of condos selling for over the asking price was unchanged in November.

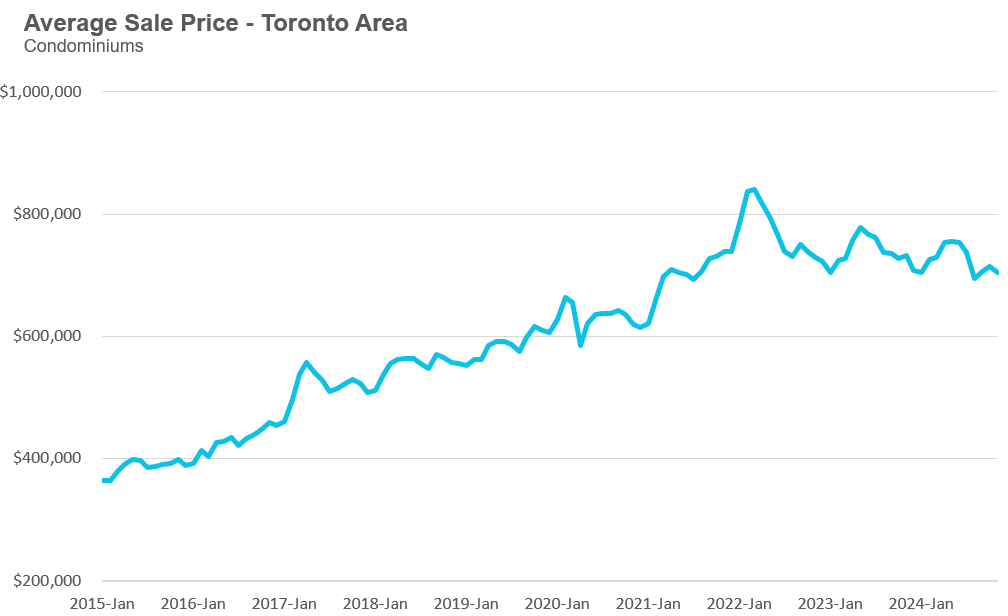

The average price of a condo in November was $705,036, down 4% from last year. The median price was $638,888, down 2% from last year.

See Market Performance by Neighbourhood Map, All Toronto and the GTA

Greater Toronto Area Market Trends