WATCH NOW: Is Toronto's Housing Market Turning a Corner?

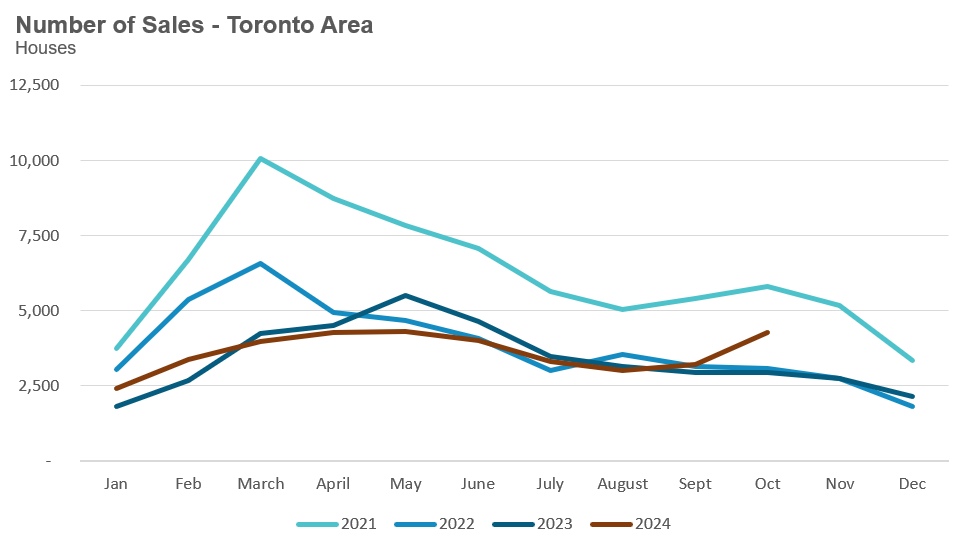

After six sluggish months, Toronto’s housing market finally turned a corner as sales surged 45% year over year for low-rise homes and 32% for condominiums in October.

It’s worth noting that the strong growth in sales is partly a function of the fact that sales volumes last year were close to 20-year lows.

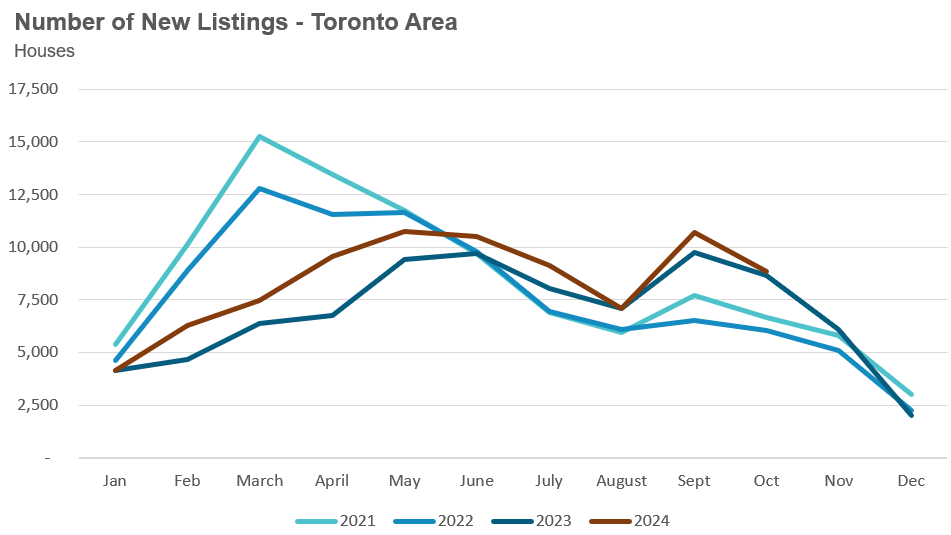

But more important than the increase in sales is that sales grew faster than new listings, which means that inventory levels are falling. When the months of inventory falls, it’s a signal that sales are outpacing new listings and that the market is gradually heating up - which is exactly what happened in October for houses and condos.

What’s behind this market rebound? While lower rates are a factor, I believe the bigger factor is that today’s buyers anticipate that the housing market will be busy in the spring due to even lower rates and the federal government’s changes to insured mortgages. They’re jumping in today to take advantage of what is still a relatively sluggish market.

While sales are up significantly over last year, and the market is gradually heating up, it’s important to note that the market is still quite slow. It’s like the market was moving at a slow 20 km/h in September, and increased speed to 30 km/h. Yes, we have picked up speed, but we’re still moving slowly.

But the anxiety many potential home buyers are feeling right now is quite high. Virtually every buyer my team and I have met with over the past month is extremely anxious that if they don’t buy a home now, they’re not going to be able to afford one in the spring market when they believe prices are going to surge.

Even though we advise them that most experts are not expecting prices to increase rapidly in the new year, buyers are reluctant to sit around and wait. Many paused their home search at the start of COVID when CMHC predicted home prices would fall. These buyers sat on the sidelines and watched home prices surge out of reach.

Many are tired of waiting and tired of putting their family’s housing needs on hold, hoping that maybe housing will become more affordable in the future.

LIVE MARKET UPDATE: WATCH REPORT HIGHLIGHTS & Q/A - THURSDAY NOVEMBER 14th 12PM ET

Join John Pasalis, report author, market analyst and President of Realosophy Realty, in a free monthly webinar as he and his guests discus key highlights and answers your questions. A must see for Toronto area real estate consumers!

Houses

House sales (low-rise freehold detached, semi-detached, townhouse, etc.) in the Greater Toronto Area (GTA) in October 2024 were up 45% compared to the same month last year.

New house listings in October were up 2% compared to last year.

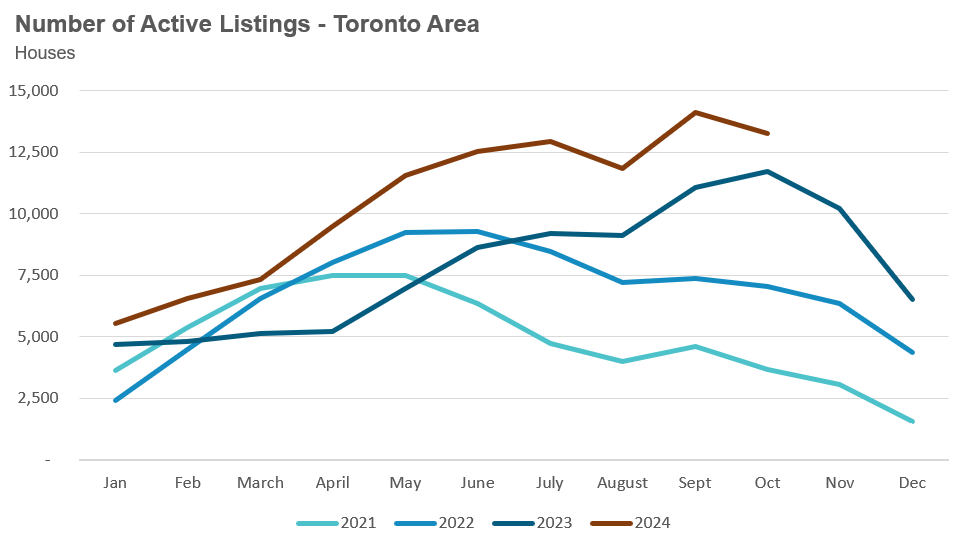

The number of houses available for sale (“active listings”) was up 14% in October compared to the same month last year.

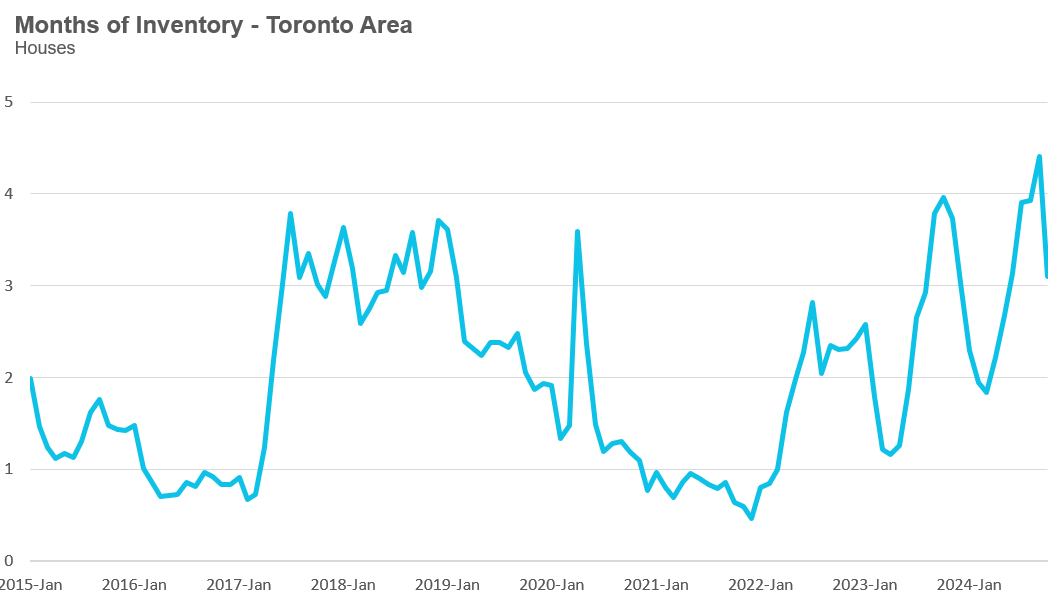

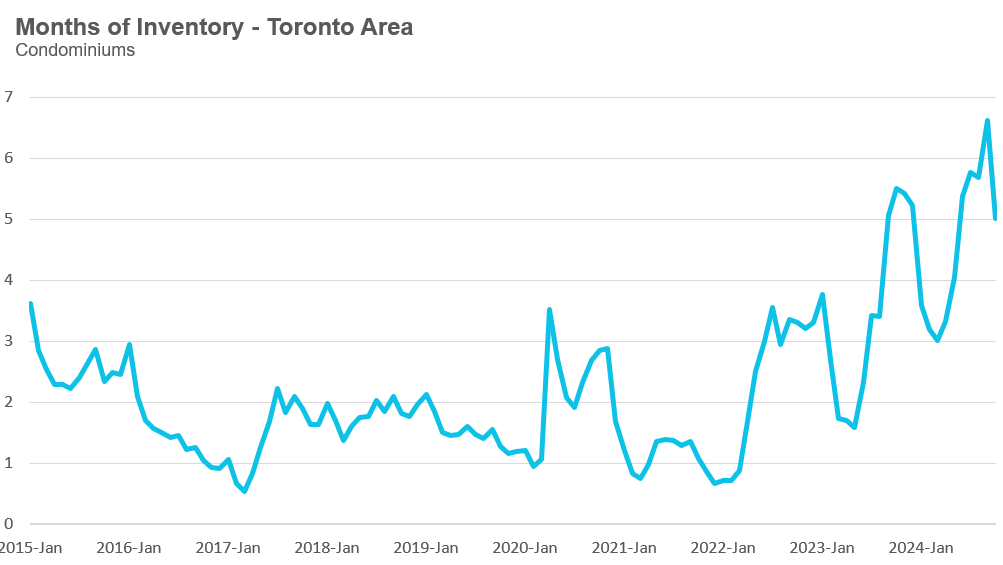

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number of homes sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell, given the current level of demand? The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

While the current level of MOI gives us clues into how competitive the market is on-the-ground today, the direction it is moving in also gives us some clues into where the market October is heading.

The MOI for houses fell to 3.1 for October.

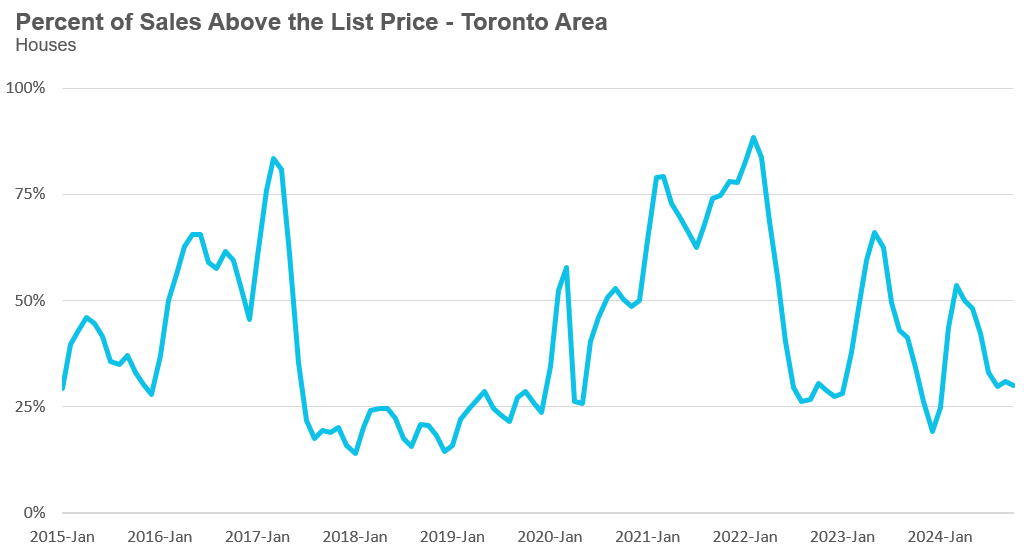

The share of houses selling for more than the owner’s list price fell to 30% in October.

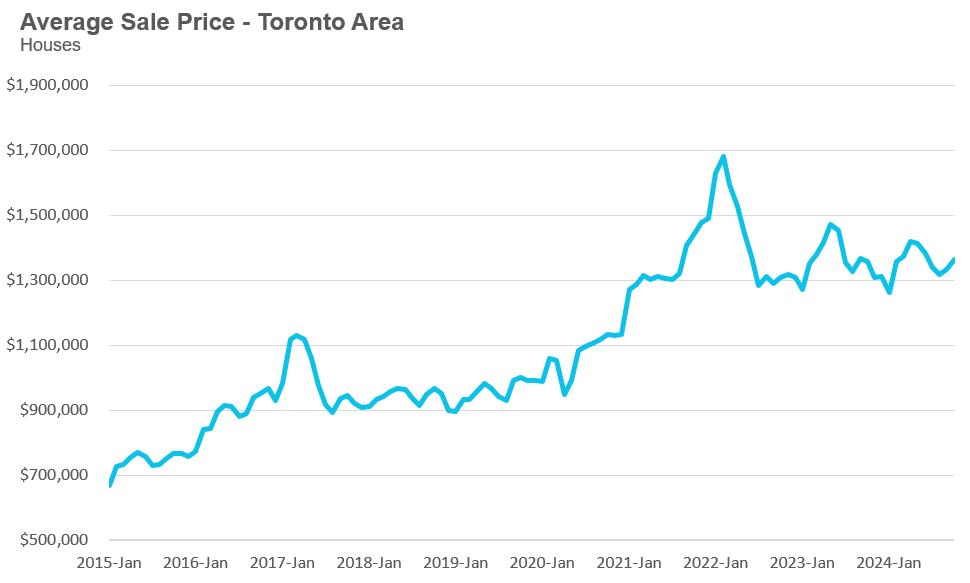

The average price for a house in October 2024 was $1,362,505, unchanged from the same month last year.

The median house price in October was $1,154,000, down 2% over last year.

The median is calculated by ordering all the sale prices in a given month and then selecting the price at the midpoint of that list such that half of all home sales are above that price and half are below that price. Economists often prefer the median price over the average because it is less sensitive to big increases in the sale of high-end or low-end homes in a given month, which can skew the average price.

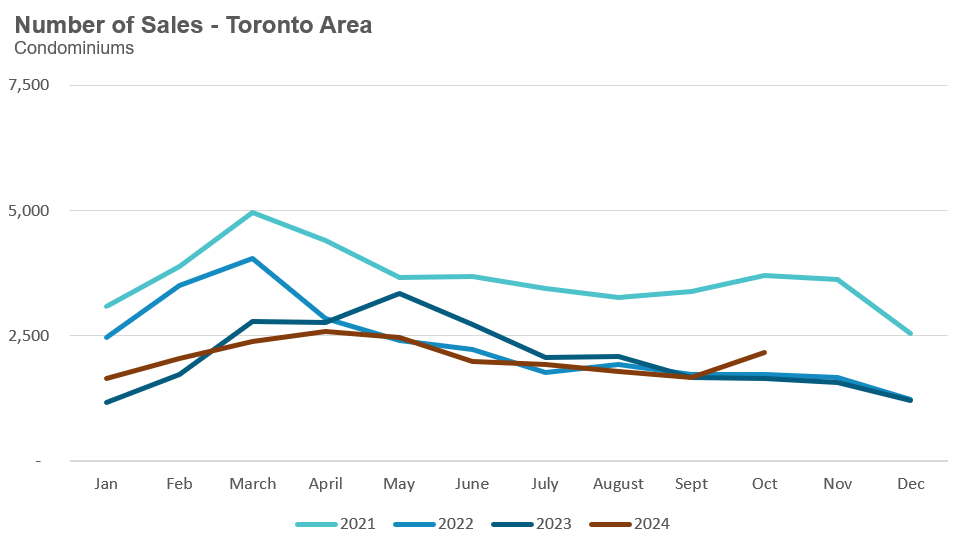

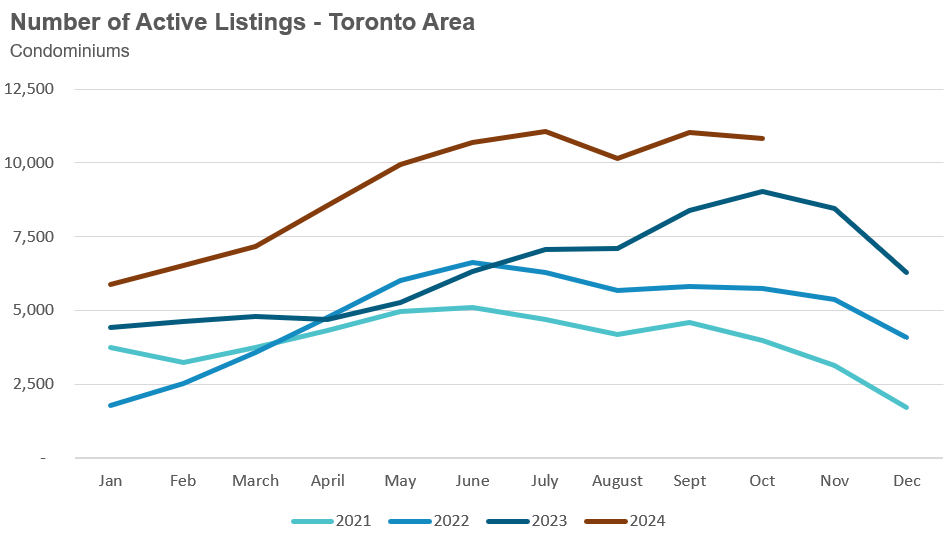

Condo (condominiums, including condo apartments, condo townhouses, etc.) sales in the Toronto area in October 2024 were up 32% compared to the same month last year.

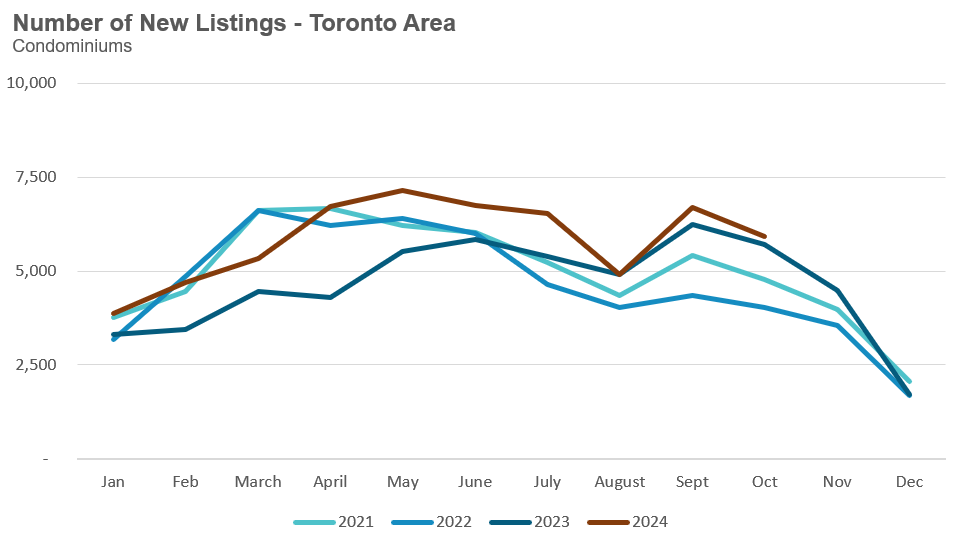

New condo listings were up 4% in October over last year.

The number of condos available for sale at the end of the month, or active listings, was up 20% over last year.

Condo months of inventory decreased to 5 MOI in October.

The share of condos selling for over the asking price was unchanged in October.

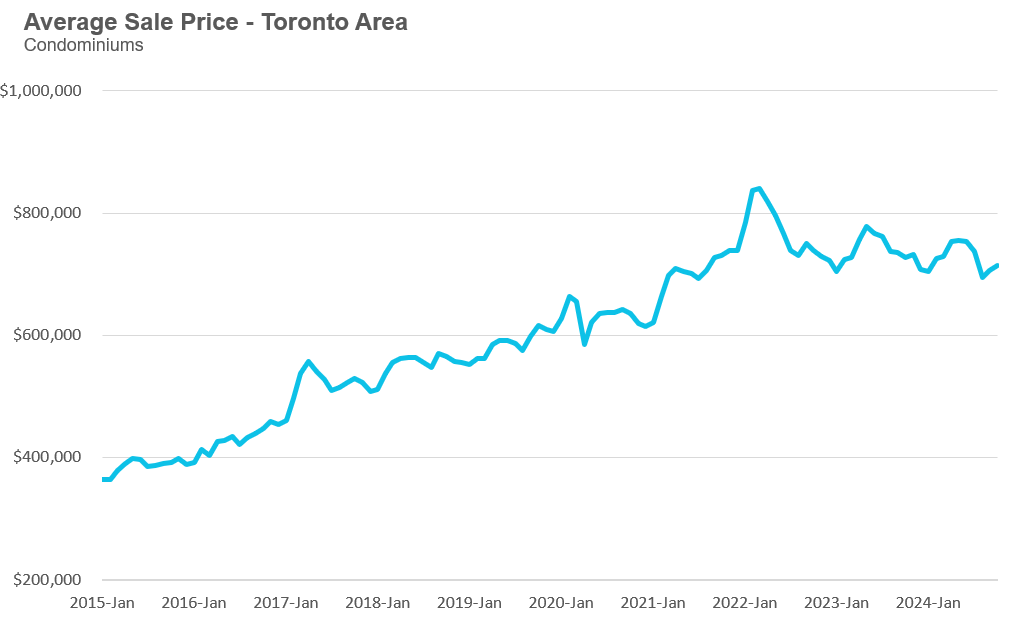

The average price of a condo in October was $713,546, down 2% from last year. The median price was $640,000, down 4% from last year.

Houses

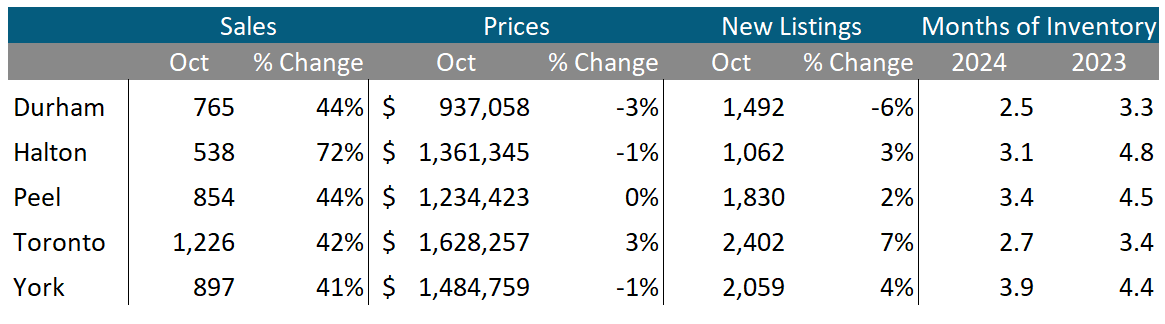

Sales were up by over 40% across all five regions, with Halton seeing a 72% increase in sales. Average prices were down 6% in Durham but up in the other four regions. Months of inventory were lower than last year in all regions.

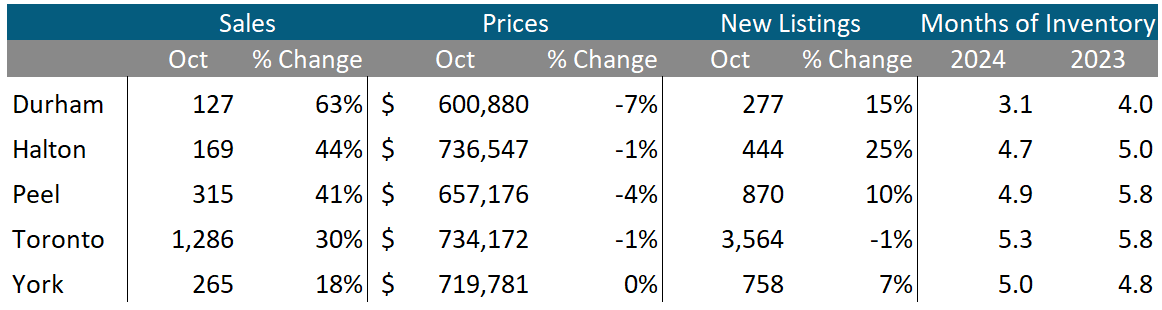

Condos

Condo sales were up in all five regions with Durham Halton and Peel seeing the biggest increase in sales. Average prices were flat in York but down in the other four regions. New listings were up by double digits in Durham, Halton and Peel and down slightly in Toronto. The MOI was down across all five regions when compared to last year.

See Market Performance by Neighbourhood Map, All Toronto and the GTA

Greater Toronto Area Market Trends