WATCH NOW: Toronto’s Fall Housing Market Remains Cool As Rate Cuts Not as Certain

While the Toronto area experienced an unseasonably warm September this year, the housing market remained cool.

Sales are up modestly over last year, but the overall dynamics remain the same — homes and condos are seeing far fewer showings from buyers when compared to six months ago, and new listing volumes continue to grow faster than sales which is contributing to inventory levels increasing.

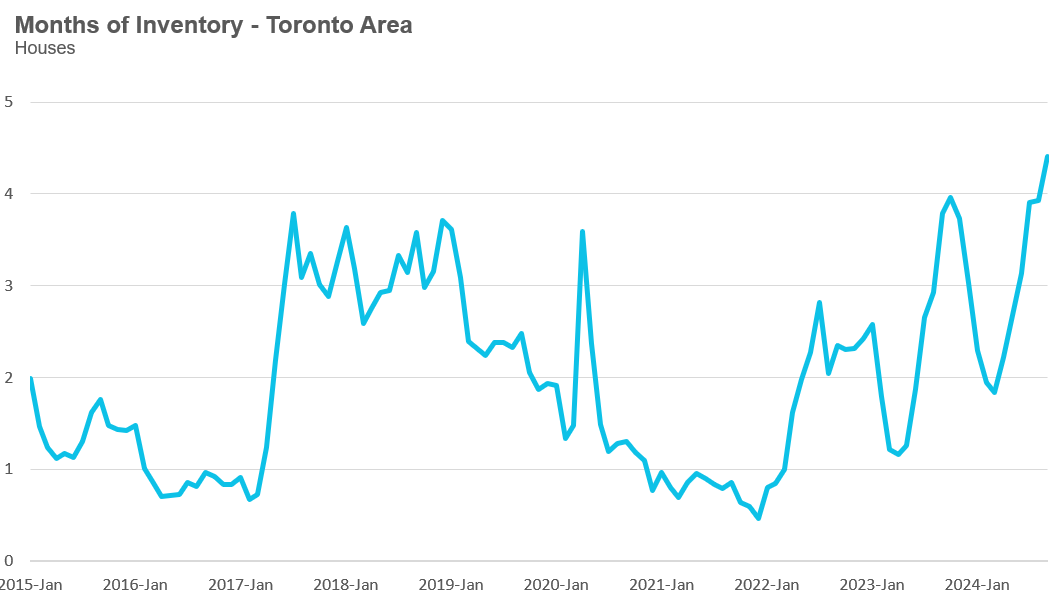

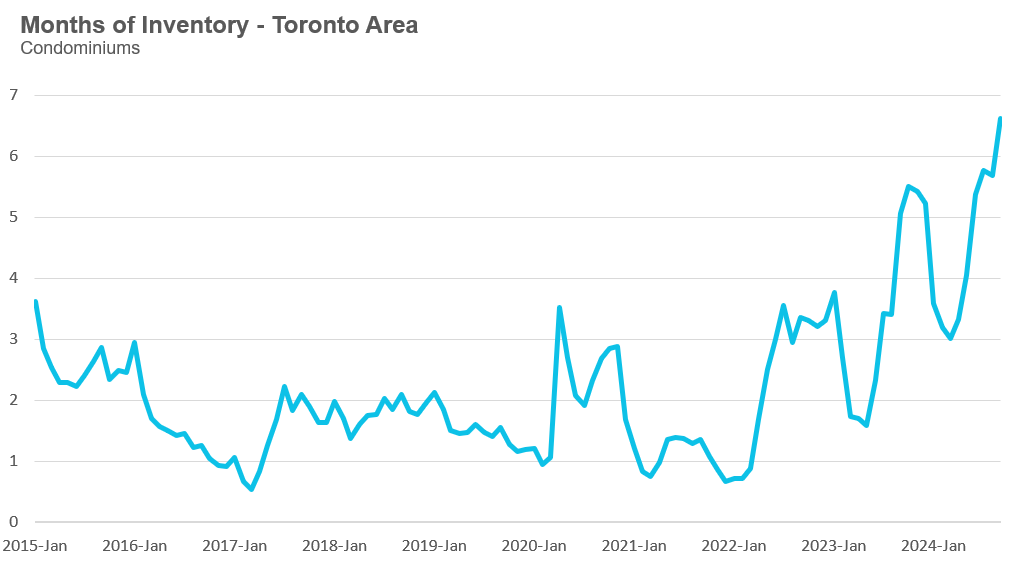

The condo market has reached 6.6 months of inventory (MOI) in September, while the market for houses reached 4.4 MOI. This is a dramatic increase from six months ago, and the next section , I will unpack some of the dynamics behind this sudden shift in the Toronto area’s housing market.

Over the past month, I have been suggesting that the housing market is likely to be far more competitive in the new year than it is today.

I suggested this when it appeared at the time that the Bank of Canada was going to cut rates three times between now and January, with one of those cuts possibly being a 50 basis point cut. Fixed rates also appeared to be trending down, suggesting a high likelihood that fixed-rate mortgages would be in the 3% range at the start of the spring market. Lower rates combined with the federal government’s changes to insured mortgages, increasing the cap on insured mortgages to $1.5M from the previous $1M and extending amortizations for first-time buyers to 30 years were all factors that would likely stimulate buyers to jump back into the market.

But this past week has shown us that the factors that determine the future path of interest rates can turn on a dime.

Two weeks ago, the United States had a very strong jobs report adding 254,000 jobs in September which made the markets less certain that the Federal Reserve would cut interest rates as aggressively as markets were predicting. A reminder that when the economy is booming, the central bank has less incentive to lower rates aggressively since lower rates will stimulate the economy even further.

The strong US jobs report caused 5-year bond yields to trend up, and because Canada’s bond market is highly correlated with the US bond market, Canada also saw 5-year bond yields surge by 35 basis points.

Suddenly, fixed-rate mortgages might be trending up in the near term, not down.

While a lot can change in the months ahead, this dramatic shift in sentiment is just a reminder that there is still a lot of uncertainty regarding economic conditions, the future path of interest rates and the housing market.

This uncertainty has elevated recently due to geopolitical risks in the Middle East. If Israel decides to retaliate against Iran by targeting their oil facilities, this could lead to a surge in oil prices, which would make it even harder for central banks to cut rates when energy prices are surging.

In short, it’s possible that some combination of robust economic conditions in North America coupled with rising energy prices may lead to far fewer interest rate cuts than markets were expecting, which would impact the future path of the housing market in 2025.

LIVE MARKET UPDATE: WATCH REPORT HIGHLIGHTS & Q/A - THURSDAY OCTOBER 10th 12PM ET

Join John Pasalis, report author, market analyst and President of Realosophy Realty, in a free monthly webinar as he and his guests discus key highlights from this report, with added timely observations about new emerging issues, and answers your questions. A must see for Toronto area real estate consumers!

WATCH NOW: Why Has Toronto’s Real Estate Market Suddenly Hit the Brakes?

The Toronto area's housing market has made a complete 180-degree turn over the past six months. Why?

In March of this year, things were pretty competitive. Homes were selling quickly and often with multiple offers. Fast forward to today, and things are a lot slower. We're seeing more for sale signs and far fewer sold signs; homes and condos are getting far fewer showings. Inventory is piling up. What is behind this relatively sudden shift in the market?

Last month I had the pleasure of speaking at an event hosted by Bank of America. Once a year, they have their Canada Banks Day, where many of their top clients meet with the CEOs and executives of Canada's top banks. The evening before that day, they hosted a private dinner and invited me to discuss Canada's housing market. I've been speaking at this event for several years, and it's always a great experience because they ask fantastic questions, which makes me think harder about our housing market.

One of their questions prompted this post. One of the questions they asked me before the event was about what had happened to Toronto's market over the past six months.

While I have been discussing the slowdown in the Toronto area’s housing market for a number of months in my reports, I have not yet dug into the data further to try to explain why things have slowed down, what is behind this and what is happening.

While I can't offer concrete reasons for the motivations of buyers and sellers in the entire Toronto area, I can share some thoughts on what might be behind some of these trends based on the data, on-the-ground anecdotes, and my observations.

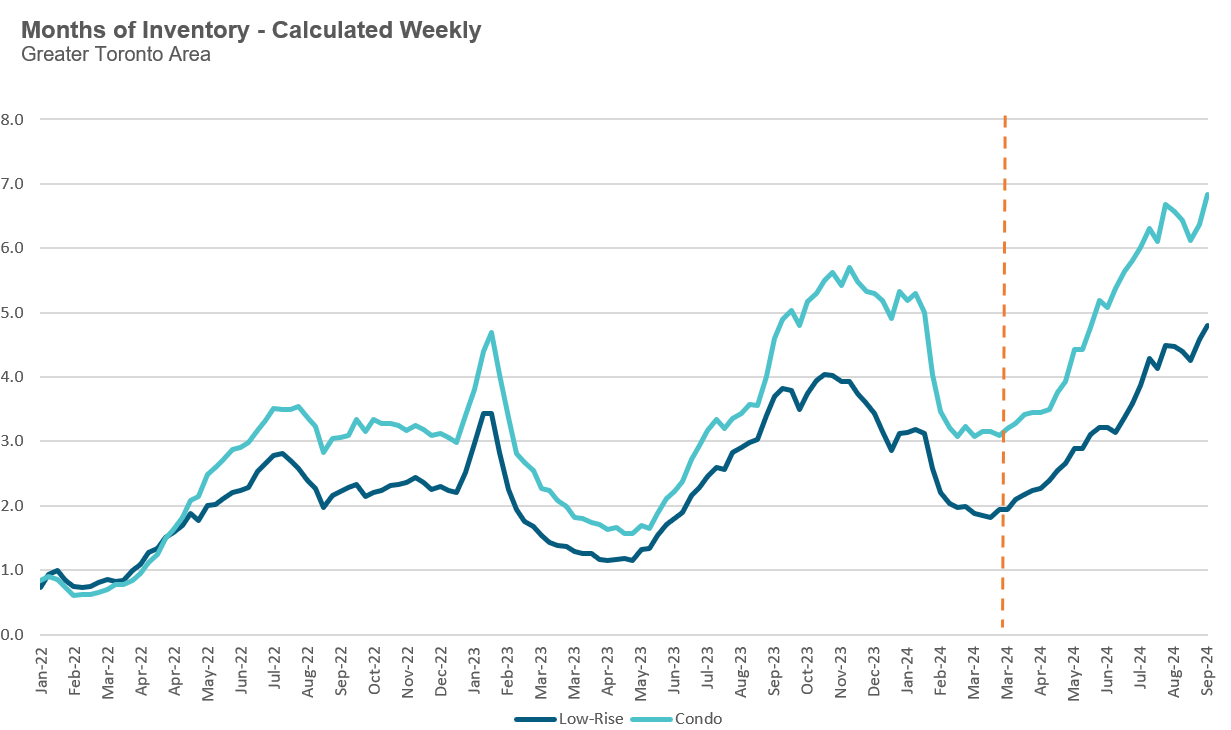

The best way to see the shift in Toronto’s housing market over the past six months is to look at a metric called the months of inventory (MOI), which measures the balance between supply and demand. We look at the number of homes available for sale, and we divide that by the number of sales over the past 30 days, and it tells us how quickly it would take the market to clear all the inventory, if nothing else, at the market. So, a market with two months of inventory is competitive. A market with six months of inventory is a lot slower. With six months of inventory we are going to see more for sale signs than sold signs.

This next chart looks at the months of inventory weekly. This is calculated by using the active number of listings each week and dividing it by the number of sales over the previous 30 days.

The housing market normally doesn’t change quickly enough to require a weekly analysis, but things have been volatile over the past couple of years, and a weekly analysis allows you to spot sudden changes in the direction of the market, which you can see in the chart above.

The dashed red line represents where the market was six months ago, at the end of March. Houses (i.e.,low-rise) are represented by the dark blue line had just 1.9 months of inventory, while condominiums (condos) had about 3.2 months of inventory. Since then, inventory has piled up in both segments. Houses have 4.7 months of inventory, and condominiums have 6.7 months of inventory.

So, what caused this change? Why did inventory start to pile up? Is this driven by a decline in sales or a surge in new listings, and what might be behind these trends?

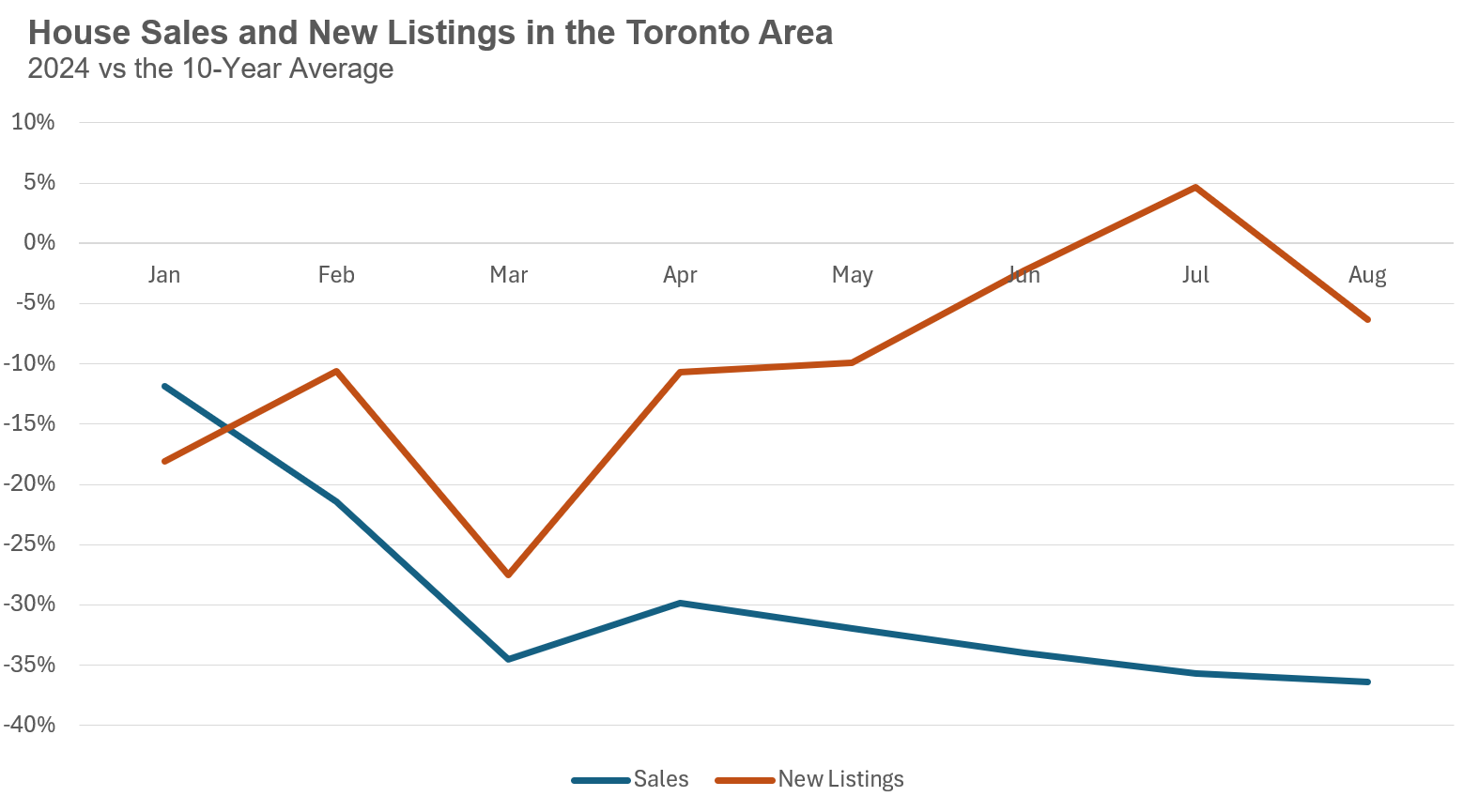

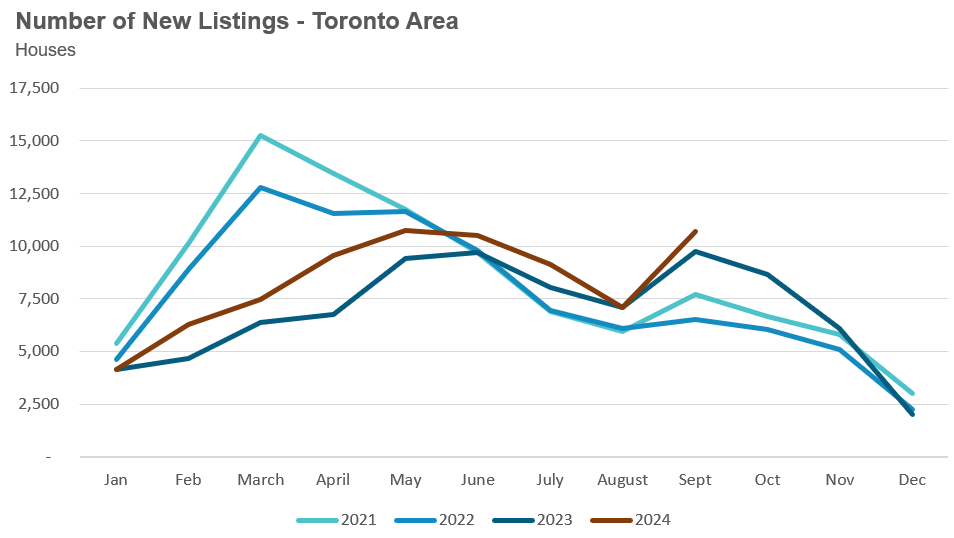

To better understand how things have evolved this year, I decided to look at the current sales and new listings volumes for each of the months between January and August 2024 and compare them to their respective 10-year averages.

The idea is to understand better how sales and new listings this year compare to historical trends. It also gives us some insight into how things have changed between the start of the year and the second half of the year, which is what we are trying to understand.

In the chart above, we look at trends for houses, and it shows sales in dark blue and new listings in red. It’s worth mentioning here that when these metrics are at 0%, it means the sales or new listings in that given month for 2024 are equal to the 10 year average. If the measure is -20% it means that sales or new listings are 20% below the 10 year average.

One thing that stands out is that sales started the year in January 12% below the 10-year average but began to plummet after that, and by March, they were down 35%. For the rest of the year, sales remained between 30 to 35% below the 10 year average. Home sales started 2024 with sales volumes close to their longer-term average, and then things gradually got worse.

When we look at the volume of new listings for houses, we see they were also below their 10-year average. And in particular, between January to March. In January, they were 18% below the 10-year average, 11% in February and by March, new listings were 28% below the 10-year average. So even though sales were down, new listings were also soft, well below their average, contributing to a relatively competitive market.

But things changed as we moved into the second half of the year. Not only were sales staying well below the historical trends, but new listings were moving up, and we can see on the chart that they're moving closer to their historical average. By July, we were slightly above the 10-year average.

So, new listing volumes for houses are closer to historical norms for the second half of the year, whereas the sales volumes were way below historical trends. This is why the market for low-rise houses has seen inventory levels accelerate in the second half of the year.

What might be driving some of these trends?

Firstly, it’s important to note that new listing volumes in 2023 were quite low relative to historical norms, with many months reaching 20-year lows in new listings. Some owners who wanted to sell may have put their plans on hold, waiting for market conditions to improve. And while market conditions are not much better this year, their patience to wait out the market may have reached its limit.

The other important factor behind the uptick in new listings is that some of these households face financial distress and need to downsize their debt. While some housing commentators and media analysts focus on analyzing the number of homes under power of sale as a signal of distress, they may be missing the entire story here.

At a recent housing conference hosted by Veritas Investment Research, Veritas Senior Investor Analyst Nigel D’Souza reminded me of an important nuance when considering distressed households in Canada.

Canada is unlikely to see a surge in homeowners defaulting on their mortgages because most Canadian homeowners have a lot of equity in their homes. House prices today are still substantially higher than they were pre-COVID. When a household with a lot of equity in their home faces financial distress and can no longer afford their mortgage payments, they are more likely to simply list their home for sale and move out of their home on their terms than to default on their mortgage.

This process of owners self-curing their mortgage debt may be one factor behind the increase in new listings during the second half of 2024.

When considering the decline in sales volumes, we see many buyers sitting on the sidelines, waiting for interest rates to drop further to afford to spend more on their next home. While rates have declined since the summer, buyers are hoping for much lower rates by the start of the new year.

However, Toronto’s cooling housing market has pushed more buyers to the sidelines for another reason. Many households that plan to upsize typically buy their next home first and then list their current home for sale. This is the typical trend in the Toronto area because it’s more challenging to buy a home — it’s a process that often takes months, while homes in Toronto typically sell in weeks. But as the market started to cool, people started to see more For Sale signs on their street and far fewer Sold signs. This has left some potential upsizers feeling more uncertain about the market conditions for the sale of their home. Some are rightfully concerned that their home may not sell for the price they need to afford their next home or, in a worst-case scenario, may not sell at all. This uncertainty has pushed some upsizing buyers to the sidelines.

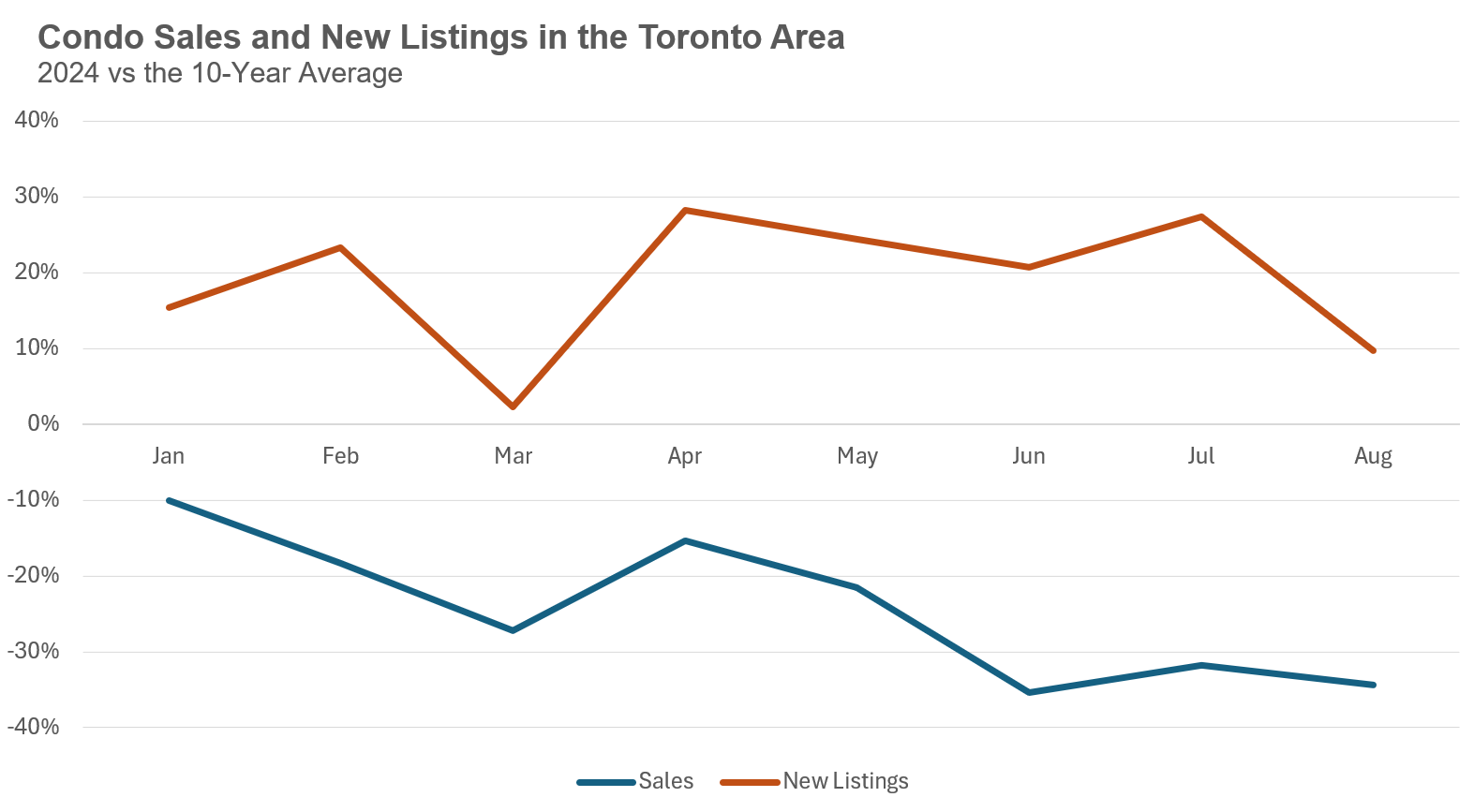

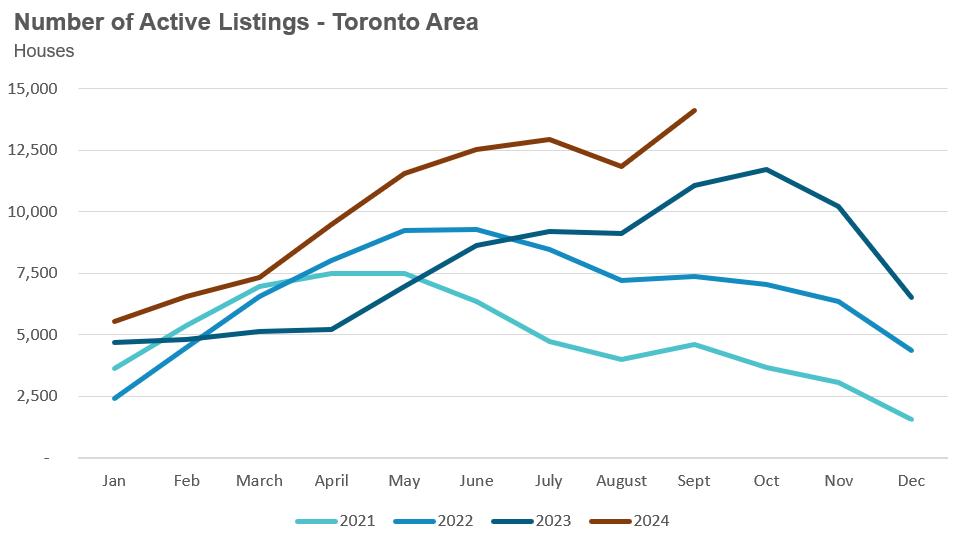

Looking at the same statistics but for the condo market reveals slightly different trends.

As we see in the chart above, condo sales in blue started the year 10% below the 10-year average and gradually declined as we moved to the second half of the year. It’s worth noting that the decline in sales is not as pronounced as it is for houses, and this may be due to the fact that houses are significantly more expensive, which is having a bigger impact on a household’s ability to buy.

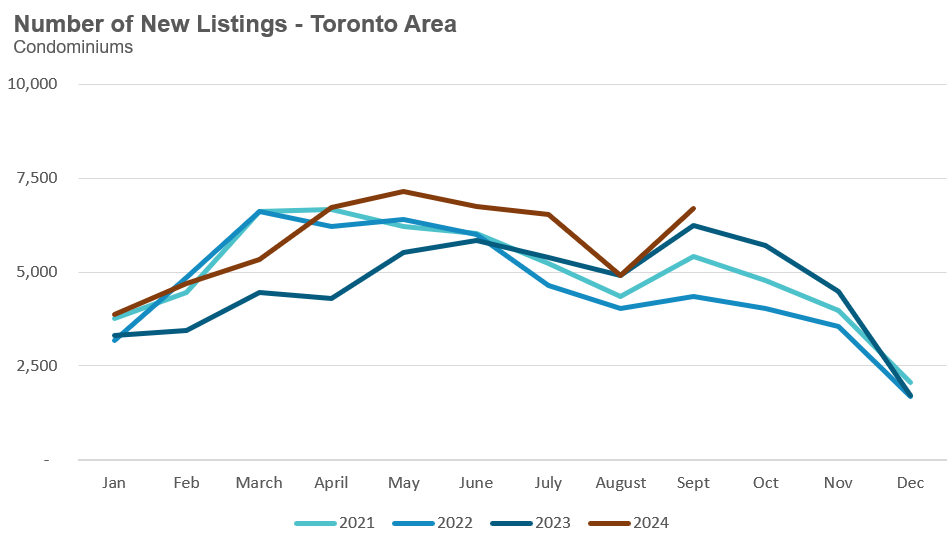

New condo listings have been well above the 10-year average, with March the only outlier, when volumes were roughly in line with the 10-year average.

The motivating factors behind the decline in sales and spike in new listings are likely very similar for condos as for houses, with one exception.

Investors own a much larger share of Toronto’s condo stock than their share of ownership for low-rise houses. Investors tend to be more leveraged than non-investors and their desire to sell one or more of their investment properties to deleverage may be one of the factors behind the elevated listing volumes in 2024.

So where does the market go from here?

I don’t expect to see any dramatic changes in the market this calendar year, but if inventory levels continue to trend up we may begin to see some downward pressure on prices.

Monthly Statistics

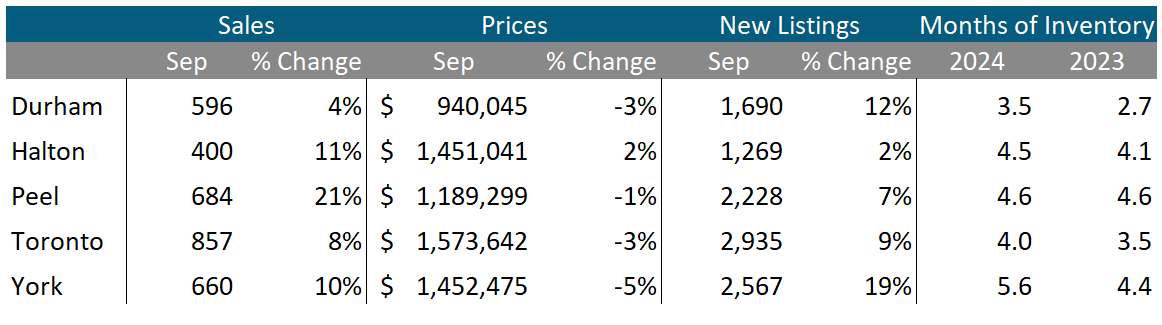

House sales (low-rise freehold detached, semi-detached, townhouse, etc.) in the Greater Toronto Area (GTA) in September 2024 were up 9% compared to the same month last year.

New house listings in September were up 10% compared to last year.

The number of houses available for sale (“active listings”) was up 27% in September compared to the same month last year.

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number of homes sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell, given the current level of demand? The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

While the current level of MOI gives us clues into how competitive the market is on-the-ground today, the direction it is moving in also gives us some clues into where the market September is heading.

The MOI for houses was up to 4.4 for September.

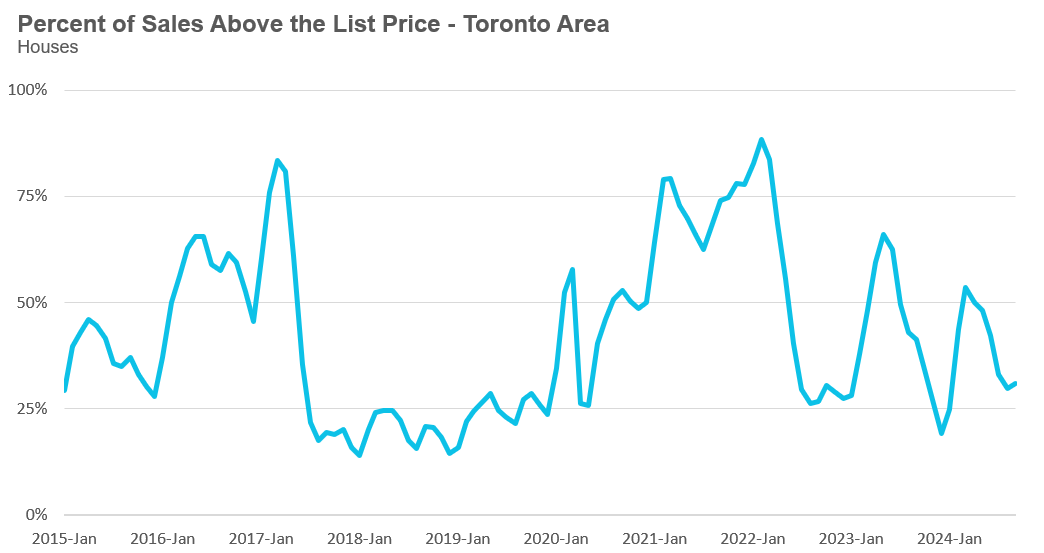

The share of houses selling for more than the owner’s list price increased to 31% in September.

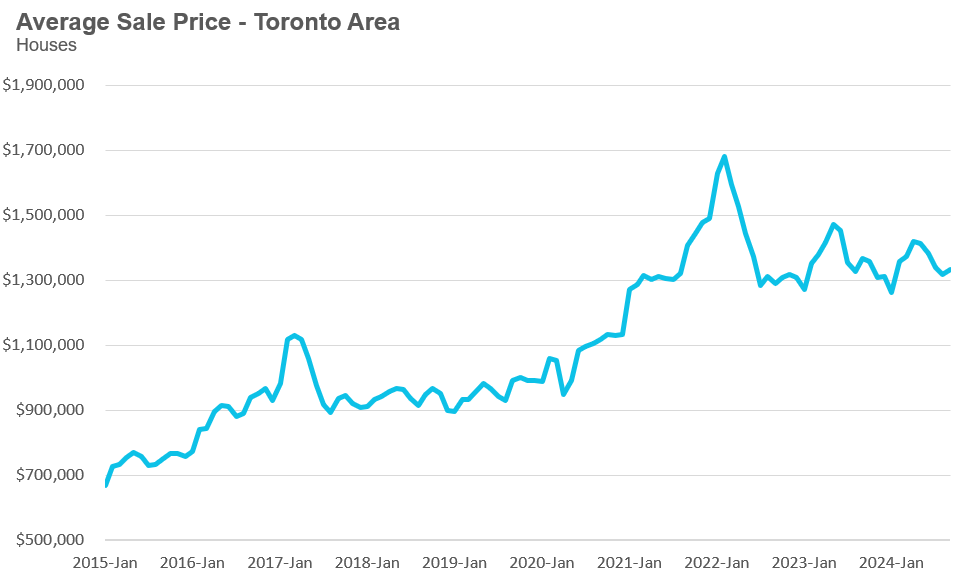

The average price for a house in September 2024 was $1,332,940, down 2% from the same month last year.

The median house price in September was $1,150,000, down 3% over last year.

The median is calculated by ordering all the sale prices in a given month and then selecting the price at the midpoint of that list such that half of all home sales are above that price and half are below that price. Economists often prefer the median price over the average because it is less sensitive to big increases in the sale of high-end or low-end homes in a given month, which can skew the average price.

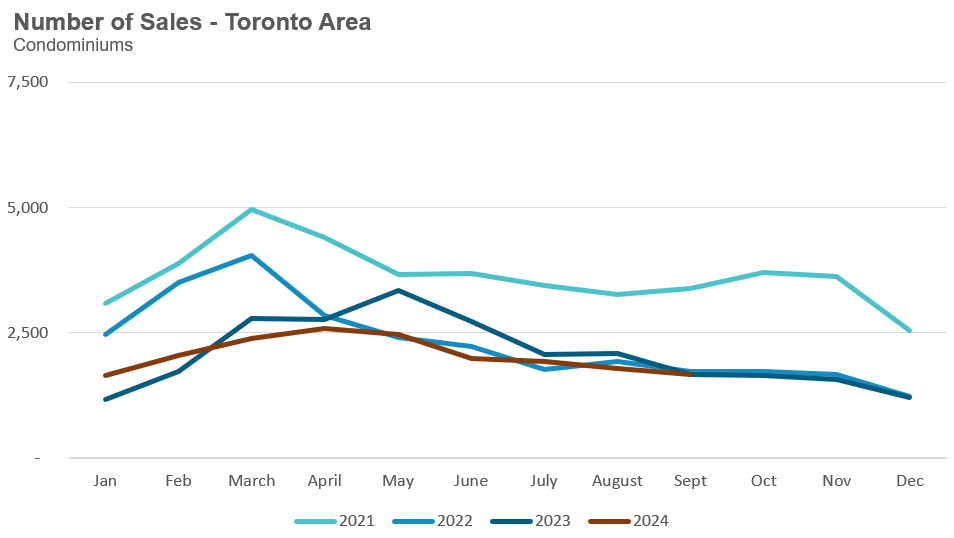

Condo (condominiums, including condo apartments, condo townhouses, etc.) sales in the Toronto area in September 2024 were unchanged compared to the same month last year.

New condo listings were up 7% in September over last year.

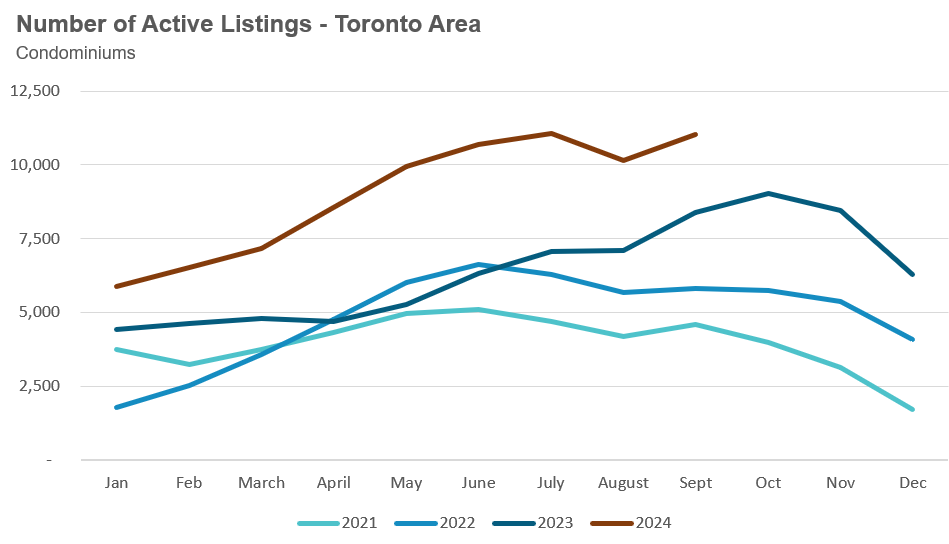

The number of condos available for sale at the end of the month, or active listings, was up 32% over last year.

Condo months of inventory decreased slightly to 6.6 MOI in September.

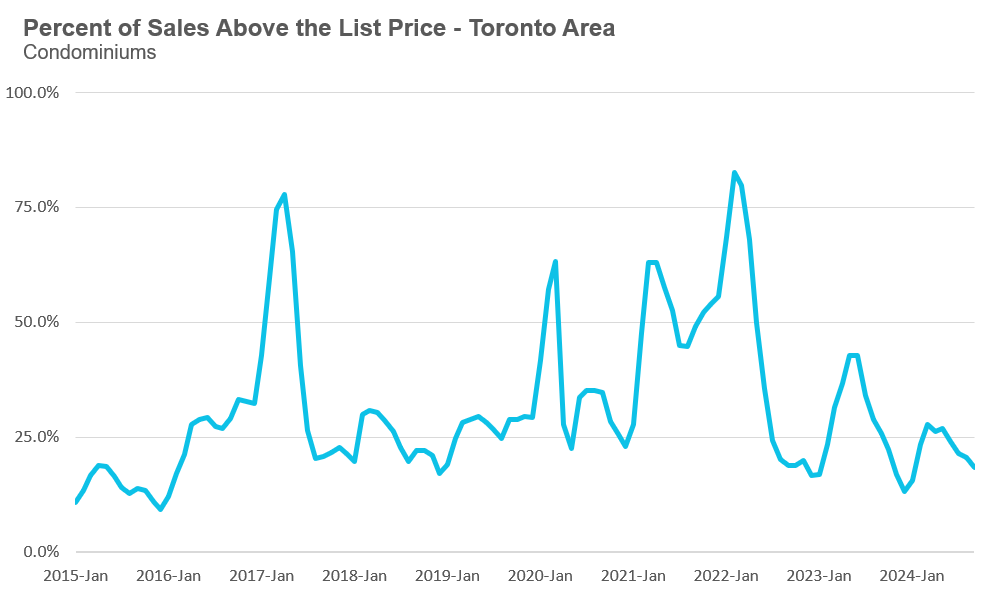

The share of condos selling for over the asking price decreased to 18% in September.

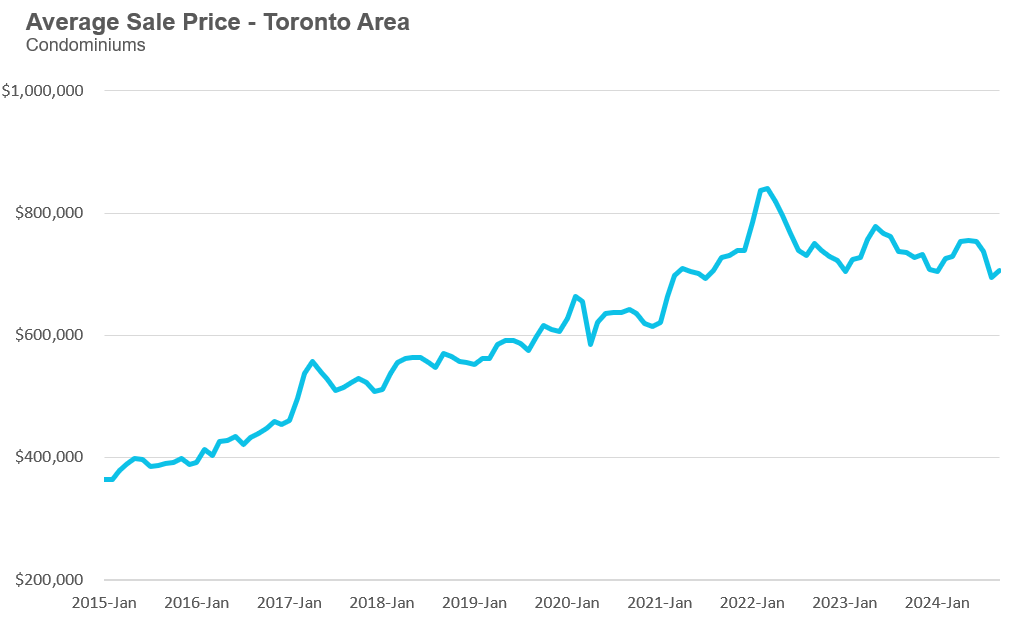

The average price of a condo in September was $706,625, down 4% from last year. The median price was $637,250, down 5% from last year.

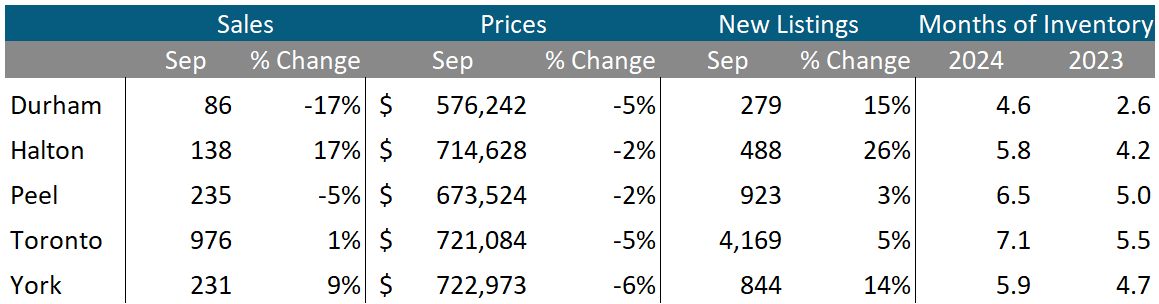

Houses

Sales were up by 21% in Peel followed by Halton at 11% and York at 10%. Average prices were up by 2% in Halton but down modestly across the other four regions. New listings were up across all four regions with York seeing the biggest increase at 19%. Months of inventory were up across all regions.

Condos

Condo sales were up by 17% and 9% in Halton and York regions, respectively while Durham saw the sharpest decline in sales at 17%. Average prices were down across the GTA. New listings and MOI were well above last year’s level for all regions. The City of Toronto has the highest MOI across all five regions.

See Market Performance by Neighbourhood Map, All Toronto and the GTA

Greater Toronto Area Market Trends