Home sales in the Greater Toronto Area have fallen to their lowest level in nearly 30 years, underscoring the impact of mounting economic uncertainty—particularly around U.S. trade and fiscal policy—on buyer sentiment. With more prospective buyers staying on the sidelines, inventory continues to build across the region.

Active listings for detached homes have reached their highest level in 15 years, and the condo market has hit a new record with 8,659 units available for sale—well above the 10-year average of 3,728.

At the same time, prices are softening. Median prices for both houses and condos have declined by 4% or more for the second consecutive month, reinforcing the shift in market conditions. Sellers are facing longer listing times and increased competition, while buyers have more leverage than they've had in years.

Unless there is a material improvement in the broader economic outlook—particularly with greater clarity around U.S.-Canada trade relations—this cautious tone is likely to continue. If such clarity emerges in the near term, there’s potential for the market to see a modest pickup in the second half of the year.

LIVE MARKET UPDATE: WATCH REPORT HIGHLIGHTS & Q/A - THURSDAY APRIL 10th 12PM ET

.png?width=600&height=300&name=Live%20Update%20-%20March%202025%20-%20MS%20600%20x%20300%20(2).png)

Join John Pasalis, report author, market analyst and President of Realosophy Realty, in a free monthly webinar as he and his guests discus key highlights and answers your questions. A must see for Toronto area real estate consumers!

Monthly Statistics

House sales (low-rise freehold detached, semi-detached, townhouse, etc.) in the Greater Toronto Area (GTA) in March 2025 were down 24% compared to the same month last year.

New house listings in March were up 31% compared to last year.

The number of houses available for sale (“active listings”) was up 81% in March compared to the same month last year.

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number of homes sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell, given the current level of demand? The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

While the current level of MOI gives us clues into how competitive the market is on-the-ground today, the direction it is moving in also gives us some clues into where the market March is heading.

The MOI for houses was unchanged at 4.4 in March.

The share of houses selling for more than the owner’s list price decreased to 36% in March.

The average price for a house in March 2025, $1,335,496, was down 3% from the same month last year.

The median house price in March was $1,175,000, down 4% over last year.

The median is calculated by ordering all the sale prices in a given month and then selecting the price at the midpoint of that list such that half of all home sales are above that price and half are below that price. Economists often prefer the median price over the average because it is less sensitive to big increases in the sale of high-end or low-end homes in a given month, which can skew the average price.

Condo (condominiums, including condo apartments, condo townhouses, etc.) sales in the Toronto area in March 2025 were down 26% compared to the same month last year.

New condo listings were up 27% in March over last year.

The number of condos available for sale at the end of the month, or active listings, was up 59% over last year.

Condo months of inventory increased to 6.5 MOI in March.

The share of condos selling for over the asking price increased to 20% in March.

The average price of a condo in March was $708,084, down 3% from last year. The median price was $635,000, down 5% from last year.

See Market Performance by Neighbourhood Map, All Toronto and the GTA

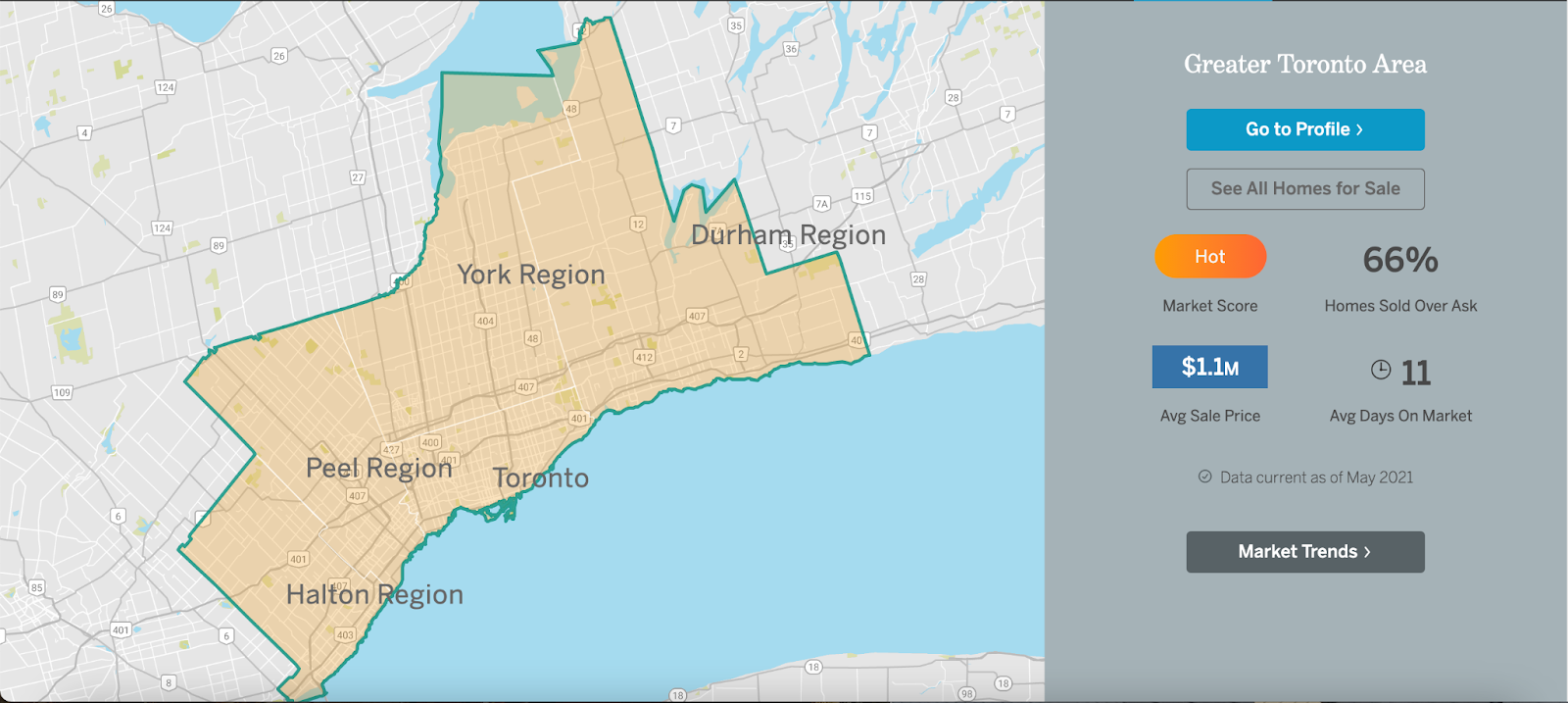

Greater Toronto Area Market Trends