Toronto’s housing market began 2025 on a muted note, with home sales continuing to hover near 20-year lows. Both house and condo sales declined compared to January of last year, reflecting ongoing cautiousness among buyers. While many in the industry—including myself—expected a slight uptick in demand this year, escalating economic uncertainty, fueled in part by the U.S.'s latest tariff threats on Canada, appears to have sidelined many prospective buyers.

At the same time, the number of homes available for sale has surged. The supply of houses on the market has climbed significantly year-over-year, though it remains in line with the levels Toronto saw in 2018 and 2019. The condo segment, however, is experiencing a more dramatic shift. New condo apartment listings hit an all-time high of 4,590, far surpassing the 10-year average of 2,751, while active listings surged to 6,913, more than double the historical average of 3,176.

This spike in condo inventory suggests that investors are increasingly looking to exit the market. With prices stagnating, rents softening, and interest rates still elevated, many are likely cashing out, adding further downward pressure on prices.

As we move further into 2025, the big question remains: how will the economic uncertainty, particularly the ripple effects of Trump’s renewed trade threats, shape the trajectory of Toronto’s housing market in the months ahead?

LIVE MARKET UPDATE: WATCH REPORT HIGHLIGHTS & Q/A - THURSDAY FEBRUARY 13th 12PM ET

.png?width=600&height=300&name=Live%20Market%20Update%20-%20True%20Size%20HS%20600-300%20(2).png)

Join John Pasalis, report author, market analyst and President of Realosophy Realty, in a free monthly webinar as he and his guests discus key highlights and answers your questions. A must see for Toronto area real estate consumers!

“Donald Trump’s 25% tariffs on Canada’s and Mexico’s exports, along with the 10% tariff on China’s, change the world.”

- Martin Wolf

Monthly Statistics

House sales (low-rise freehold detached, semi-detached, townhouse, etc.) in the Greater Toronto Area (GTA) in January 2025 were down 9% compared to the same month last year.

New house listings in January were up 56% compared to last year.

The number of houses available for sale (“active listings”) was up 59% in January compared to the same month last year.

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number of homes sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell, given the current level of demand? The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

While the current level of MOI gives us clues into how competitive the market is on-the-ground today, the direction it is moving in also gives us some clues into where the market January is heading.

The MOI for houses increased to 4 in January.

The share of houses selling for more than the owner’s list price fell to 29% in January.

The average price for a house in January 2025, $1,274,541, was up 1% from the same month last year.

The median house price in January was $1,130,000, up unchanged over last year.

The median is calculated by ordering all the sale prices in a given month and then selecting the price at the midpoint of that list such that half of all home sales are above that price and half are below that price. Economists often prefer the median price over the average because it is less sensitive to big increases in the sale of high-end or low-end homes in a given month, which can skew the average price.

Condo (condominiums, including condo apartments, condo townhouses, etc.) sales in the Toronto area in January 2025 were down 11% compared to the same month last year.

New condo listings were up 41% in January over last year.

The number of condos available for sale at the end of the month, or active listings, was up 46% over last year.

Condo months of inventory increased to 5.9 MOI in January.

The share of condos selling for over the asking price fell to 15% in January.

The average price of a condo in January was $699,645, down 1% from last year. The median price was $632,000, unchanged from last year.

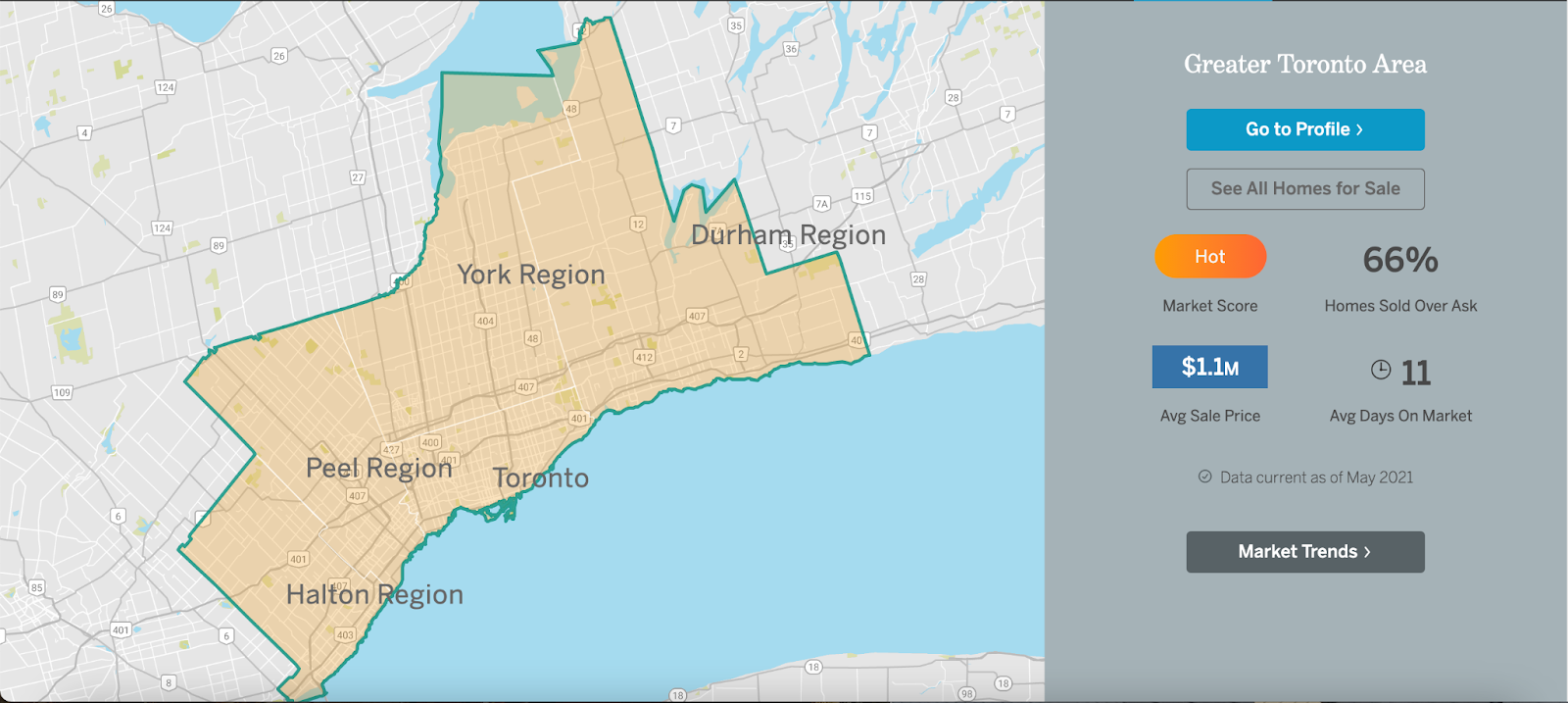

See Market Performance by Neighbourhood Map, All Toronto and the GTA

Greater Toronto Area Market Trends