WATCH NOW: Toronto’s Spring Housing Market Is Dead on Arrival

The spring housing market in Toronto has officially stalled.

The latest data for May paints a bleak picture. Condo sales are down 23% year-over-year, with prices falling 7%. Inventory has climbed to nearly 8 months’ worth of supply—a clear sign that listings are far outpacing buyer demand.

The market for houses isn’t much stronger. While sales are down a more modest 5% compared to last year, this marks the fourth consecutive month of 30-year lows in sales activity. To put it in perspective: more homes sold in May 1996 than in May 2025.

Even downtown neighbourhoods that were seeing strong demand and multiple offers just a couple of months ago have cooled noticeably. Offer nights are increasingly unsuccessful, and homes are sitting on the market longer than sellers expected.

This isn’t just a story about the housing market. It’s a reflection of broader economic unease. Rising global uncertainty and growing concerns about job security are pushing would-be buyers to the sidelines. People don’t tend to make major financial decisions—like buying a home—when they’re worried about their income or employment.

When that confidence will return is anyone’s guess. Until then, expect continued weakness in Toronto’s housing market.

LIVE MARKET UPDATE: WATCH REPORT HIGHLIGHTS & Q/A - THURSDAY JUNE 12th 12PM ET

Join John Pasalis, report author, market analyst and President of Realosophy Realty, in a free monthly webinar as he and his guests discus key highlights and answers your questions. A must see for Toronto area real estate consumers!

Over the past few weeks, I’ve spoken with several small builders in Toronto who are weighing whether to move forward with new multiplex projects. One of the key challenges they’re grappling with is reconciling the desire to add much-needed rental supply with the reality that average rents across the GTA are declining.

But the problem with using citywide rent averages to make decisions is that they obscure the true story.

Toronto’s rental market isn’t moving in lockstep. There are significant differences in rent performance depending on geography, housing type, and even unit size. In other words, what’s happening with micro condos in the city is not what’s happening with large family-sized homes in the suburbs.

To illustrate this, I looked at average rents in the City of Toronto (not the GTA) and broke them down into more meaningful categories:

I then compared how average rents for each category have changed over two key periods: from May 2019 to May 2025, and from the peak in August 2023 to today.

Here’s what the data shows:

These numbers paint a clear picture: demand - and pricing power - has been far more resilient for larger, family-sized rentals.

This divergence is a direct consequence of policy failure. For years, Ontario’s housing strategy prioritized the rapid production of micro condos, fuelled by speculative investor demand, while neglecting the creation of family-oriented housing. The result is a surplus of tiny units with softening rents and a shortage of larger homes where rental demand remains strong.

For builders planning new multiplexes today, this cross-sectional view of the market is critical. Projects that meet the needs of families - particularly in the form of well-designed, larger units in central locations - are likely to remain more stable, even as smaller rental units face downward pressure.

In the years ahead, I expect this trend to continue: rents for family-sized homes will remain resilient, while oversupplied micro-units will see further declines. Builders and policymakers alike would be wise to take note.

“The driving factor is supply restrictions. The 5 years of process it takes to build anything in much of Ontario or BC is a real problem. Cities like Edmonton see little speculative financialization because supply meets demand and 2.8% ⬆️ prices per year is a bad investment.”

- Robert Summers

This is a common narrative among economists and housing advocates - that Edmonton has effectively "solved" housing by removing regulatory barriers to supply. In particular, the city is often praised for its 2023 move to legalize 8-unit multiplexes on every residential lot.

But there's a clear disconnect between this narrative and the actual data.

If we look at the decade leading up to the 2020s, Edmonton’s housing market was already showing very modest price growth—even before zoning reforms. Between 2010 and 2020, Edmonton’s seasonally adjusted benchmark home prices rose just 12%, compared to a 64% increase nationally. The explanation for this wasn’t that Edmonton had already adopted abundant zoning, but that it was never a major magnet for national or global investment capital in the first place.

Which brings us to a more puzzling trend.

Over the past 12 months—after multiplexes were legalized—Edmonton’s benchmark prices have surged by 11%, even as Canadian home prices have declined by 3%. Put another way, Edmonton saw nearly as much price growth in a single year after upzoning as it did in the entire decade before.

This raises an important question: if zoning reform has allowed supply to meet demand in Edmonton, as Professor Summers suggests, why are home prices rising more rapidly today than they were during the years when zoning was more restrictive?

To be clear, I don’t claim to have all the answers—Edmonton is not a market I follow closely. But I do think it’s time we move past simplistic, one-size-fits-all explanations for housing affordability. Zoning reform is likely a necessary part of the solution in many cities, but it’s not sufficient on its own—and in some markets, it may not even be the primary driver of affordability.

The Edmonton case deserves a more nuanced analysis than it’s currently getting in policy circles and housing Twitter.

Monthly Statistics

House sales (low-rise freehold detached, semi-detached, townhouse, etc.) in the Greater Toronto Area (GTA) in May 2025 were down 5% compared to the same month last year but at their lowest levels in thirty years, aside from the first months of the COVID lockdowns in 2020.

New house listings in May were up 23% compared to last year.

The number of houses available for sale (“active listings”) was up 52% in May compared to the same month last year.

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number of homes sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell, given the current level of demand? The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

While the current level of MOI gives us clues into how competitive the market is on-the-ground today, the direction it is moving in also gives us some clues into where the market May is heading.

The MOI for houses was down slightly at 4.3 in May.

The share of houses selling for more than the owner’s list price decreased to 32% in May.

The average price for a house in May 2025, $1,326,418, was down 6% from the same month last year.

The median house price in May was $1,150,000, down 7% over last year.

The median is calculated by ordering all the sale prices in a given month and then selecting the price at the midpoint of that list such that half of all home sales are above that price and half are below that price. Economists often prefer the median price over the average because it is less sensitive to big increases in the sale of high-end or low-end homes in a given month, which can skew the average price.

Condo (condominiums, including condo apartments, condo townhouses, etc.) sales in the Toronto area in May 2025 were down 23% compared to the same month last year and at their lowest level in twenty years, aside from the first months of the COVID lockdowns in 2020.

New condo listings were up 8% in May over last year.

The number of condos available for sale at the end of the month, or active listings, was up 36% over last year.

Condo months of inventory increased to 7.2 MOI in May.

The share of condos selling for over the asking price increased modestly to 18% in May.

The average price of a condo in May was $702,389, down 7% from last year. The median price was $625,000, down 7% from last year.

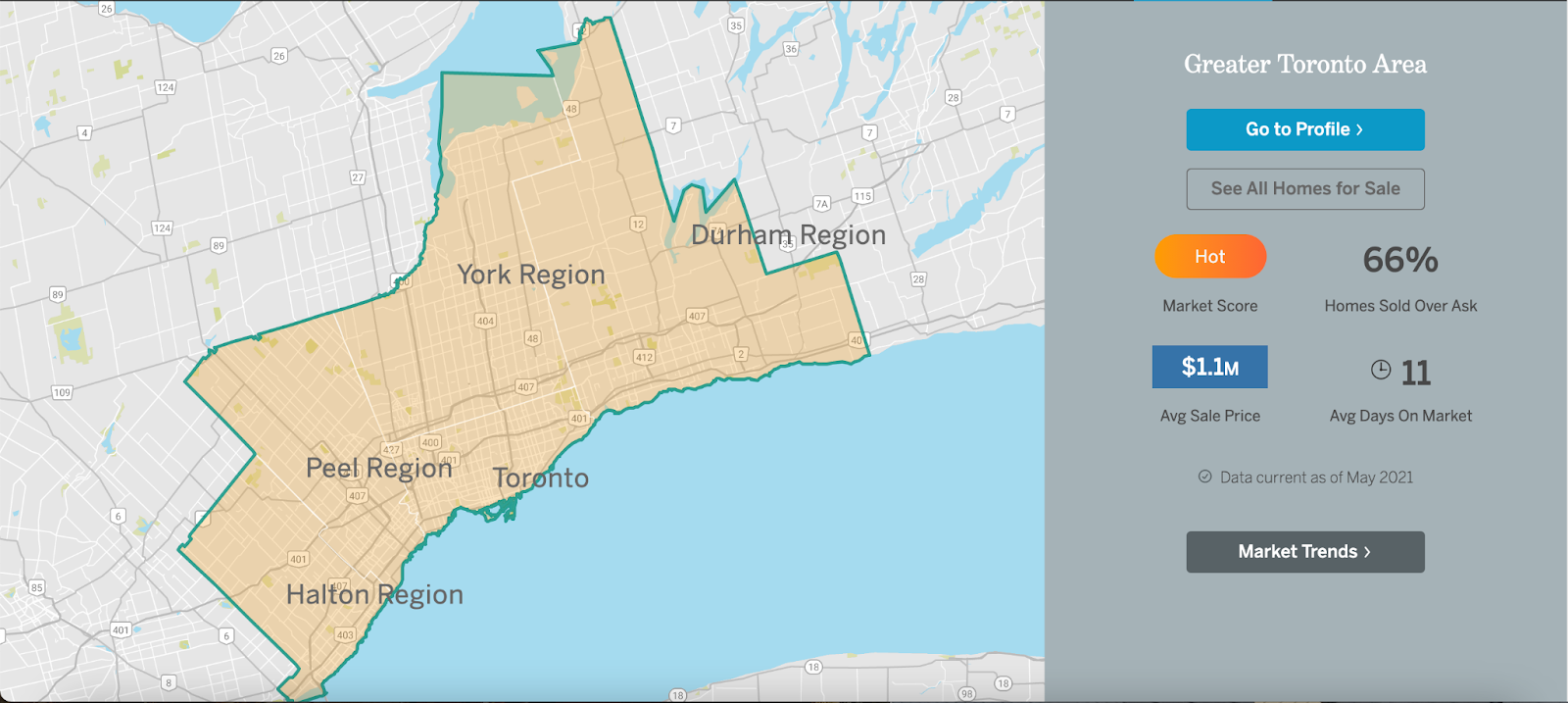

See Market Performance by Neighbourhood Map, All Toronto and the GTA

Greater Toronto Area Market Trends