Home sales across the Toronto area remained historically low in April, tracking near 30-year lows outside of the brief collapse in 2020 at the start of the COVID lockdowns. We’re now starting to see this weakness reflected in prices. Average and median home prices are down about 6–7% for both houses and condos compared to last year.

But these headline numbers mask a bigger story—one of growing regional divergence.

While sales are slow across the board, low-rise homes in the City of Toronto are holding up far better than those in the suburbs. The city has just 3.5 months of inventory for low-rise houses—well below Peel and York Regions, where inventory levels are above 5 months. That tighter supply is helping keep prices more stable in the city.

If we track month-over-month changes in median prices over the first four months of this year, Toronto’s low-rise market has moved within a narrow range—no more than 2% up or down in any given month. The suburban regions are telling a different story. In April alone, median prices fell 10% in Halton, 9% in Peel, and 7% in York.

On the ground, the contrast is even more stark. Buyers looking in central Toronto are still facing multiple offers in some neighbourhoods—something that feels totally out of step with the broader narrative of a soft market. Urban homes are clearly outperforming the suburbs, and that’s creating a disconnect between the headlines and what active buyers are actually experiencing.

LIVE MARKET UPDATE: WATCH REPORT HIGHLIGHTS & Q/A - THURSDAY MAY 15th 12PM ET

Join John Pasalis, report author, market analyst and President of Realosophy Realty, in a free monthly webinar as he and his guests discus key highlights and answers your questions. A must see for Toronto area real estate consumers!

Economist Mike Moffatt often goes out of his way to downplay a critical trend shaping Canada’s housing market: the growing share of homes being purchased by investors, a shift that is making it increasingly difficult for Canadian households to own a home of their own.

Recently, Mike argued that the reason people have been buying investment properties is because of a boom in non-permanent residents. But this claim doesn’t hold up to scrutiny.

First, the surge in non-permanent residents is a relatively recent phenomenon, with most of the increase occurring over the past four years. In contrast, the share of homes bought by investors has been rising steadily for over two decades. This long-term trend has been a key factor behind the decline in Canada’s homeownership rate since 2011.

While the recent population boom may have made real estate more appealing to investors, it wasn’t the only—or even the main—factor driving investor activity. There are a number of reasons why investor demand has grown over the past two decades, but one of the most important was the prolonged period of ultra-low interest rates following the global financial crisis and again during the COVID pandemic. These low rates pushed investors to seek out alternative assets that offered stable, long-term returns—and housing fit that bill. We’ve seen this not only in Canada, but also in the United States, where Wall Street firms have raised billions to buy single-family homes—even in markets with abundant housing supply and no comparable surge in non-permanent residents.

I’ve followed Mike’s work for many years and appreciate his contributions to the housing debate. But this is one area where his analysis misses the mark. Investor demand isn’t a recent phenomenon, and it certainly can’t be reduced to a single factor like the growth in non-permanent residents. The rise of investors in Canada’s housing market is a long-running trend—one that predates the recent population surge by well over a decade. It’s been driven by a mix of structural factors: decades of falling interest rates, favourable tax policies, weak regulation, and the growing view of housing as a financial asset rather than a place to live.

Dismissing this long-running shift as a recent response to population growth overlooks the deeper structural forces that have been transforming Canada’s housing market for decades—and obscures the reality that these trends are not only shutting an entire generation out of homeownership, but also fueling a widening divide between those who own property and those who don’t.

Watch Now: The Great Sell Off Presented on YouTube

This is the executive summary of The Great Sell-Off, a report exploring how housing in Canada has shifted from a source of shelter to a driver of wealth—and what that means for affordability, inequality, and the future of Canadian Society.

Every election, we hear the same promises: more housing, more affordability. But for the next generation, homeownership is slipping further into fantasy.

I’ve been in the real estate business for over twenty years, and in that time, I’ve seen young homebuyers lose hope - and parents wonder why their children can’t afford what once seemed attainable. For decades, the benchmark for affordability was simple: a home should cost no more than four times a

household’s income. Today, that number is closer to ten in Toronto and twelve in Vancouver - a level once considered unthinkable.

We’re told this is just “basic economics” - a supply problem easily fixed by building more homes. But this narrative oversimplifies the issue and masks a more fundamental transformation. Homes are not like widgets from a factory. They’re a basic human need and a financial asset that appreciates over time.

When a good becomes both a necessity and a financial investment, the usual rules of supply and demand begin to break down.

Contrary to what many suggest, home prices in Canada didn’t explode because cities stopped building. In fact, many metropolitan areas have seen a steady pipeline of new housing. What’s changed is the role that housing plays in our financial system. We’ve moved from one economic reality to another - a full

paradigm shift.

In the old housing paradigm, home prices were anchored by incomes. Households saved for a down payment, qualified for a mortgage based on what they earned, and bought homes to live in. That world was governedby an internal logic: prices couldn’t rise far beyond what people could

reasonably afford.

But in the new paradigm, that anchor has been severed. Housing is no longer just about shelter - it’s a financial instrument. Prices are no longer constrained by income but driven by capital flows. Homes are bought not just by Canadian households but by investors - some domestic, some global - whose purchasing power is shaped not by salaries but by access to wealth, credit, and leverage.

This shift began in the 1990s when the federal government, grappling with a fiscal crisis, encouraged households to borrow against home equity to stimulate spending. What started as a strategy to support consumption and home renovations soon evolved into a means of financing the purchase of additional properties. Then came the 2008 financial crisis and, more recently, the COVID-19 pandemic - both marked by ultra-low interest rates. As yields on traditional investments dried up, real estate emerged as a safe and lucrative store of value.

Today, investors account for nearly one in three home purchases in Canada. As their presence has grown, so too has the disconnect between home prices and the real economy. A house is no longer just a place to live - it’s a wealth-generation tool, often wielded by those who already hold significant financial advantages.

This has created two serious challenges. First, it has pushed housing further out of reach for younger Canadians, many of whom no longer see a realistic path to ownership. Unlike earlier generations, they are not just up against peers with similar means - they are up against capital-rich investors whose buying power is unconstrained by income. Second, it has distorted the allocation of capital across the economy. Money that could be funding innovation, productivity, and job creation is instead being poured into the ownership of multiple properties. Canada has built an economy where the best way to get rich isn’t to invent, create, or build anything - it’s to own houses and wait for prices to rise.

Recognizing this paradigm shift is the first step toward real reform. If we continue designing housing policy for a system that no longer exists, we’ll keep getting the same results: higher prices, deeper inequality, and a generation locked out.

If we want a resilient economy and a housing market in which the next generation has a real shot at owning a home, just as previous generations did, we must rethink what we reward. That means redirecting capital toward sectors that drive innovation, competitiveness, and good jobs instead of propping up a system that treats housing as a shortcut to easy wealth.

Monthly Statistics

House sales (low-rise freehold detached, semi-detached, townhouse, etc.) in the Greater Toronto Area (GTA) in April 2025 were down 17% compared to the same month last year.

New house listings in April were up 15% compared to last year.

The number of houses available for sale (“active listings”) was up 65% in April compared to the same month last year.

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number of homes sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell, given the current level of demand? The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

While the current level of MOI gives us clues into how competitive the market is on-the-ground today, the direction it is moving in also gives us some clues into where the market April is heading.

The MOI for houses was unchanged at 4.4 in April.

The share of houses selling for more than the owner’s list price decreased to 35% in April.

The average price for a house in April 2025, $1,328,957, was down 6% from the same month last year.

The median house price in April was $1,150,000, down 7% over last year.

The median is calculated by ordering all the sale prices in a given month and then selecting the price at the midpoint of that list such that half of all home sales are above that price and half are below that price. Economists often prefer the median price over the average because it is less sensitive to big increases in the sale of high-end or low-end homes in a given month, which can skew the average price.

Condo (condominiums, including condo apartments, condo townhouses, etc.) sales in the Toronto area in April 2025 were down 29% compared to the same month last year.

New condo listings were up 5% in April over last year.

The number of condos available for sale at the end of the month, or active listings, was up 47% over last year.

Condo months of inventory increased to 6.9 MOI in April.

The share of condos selling for over the asking price decreased to 17% in April.

The average price of a condo in April was $703,153, down 7% from last year. The median price was $638,000, down 7% from last year.

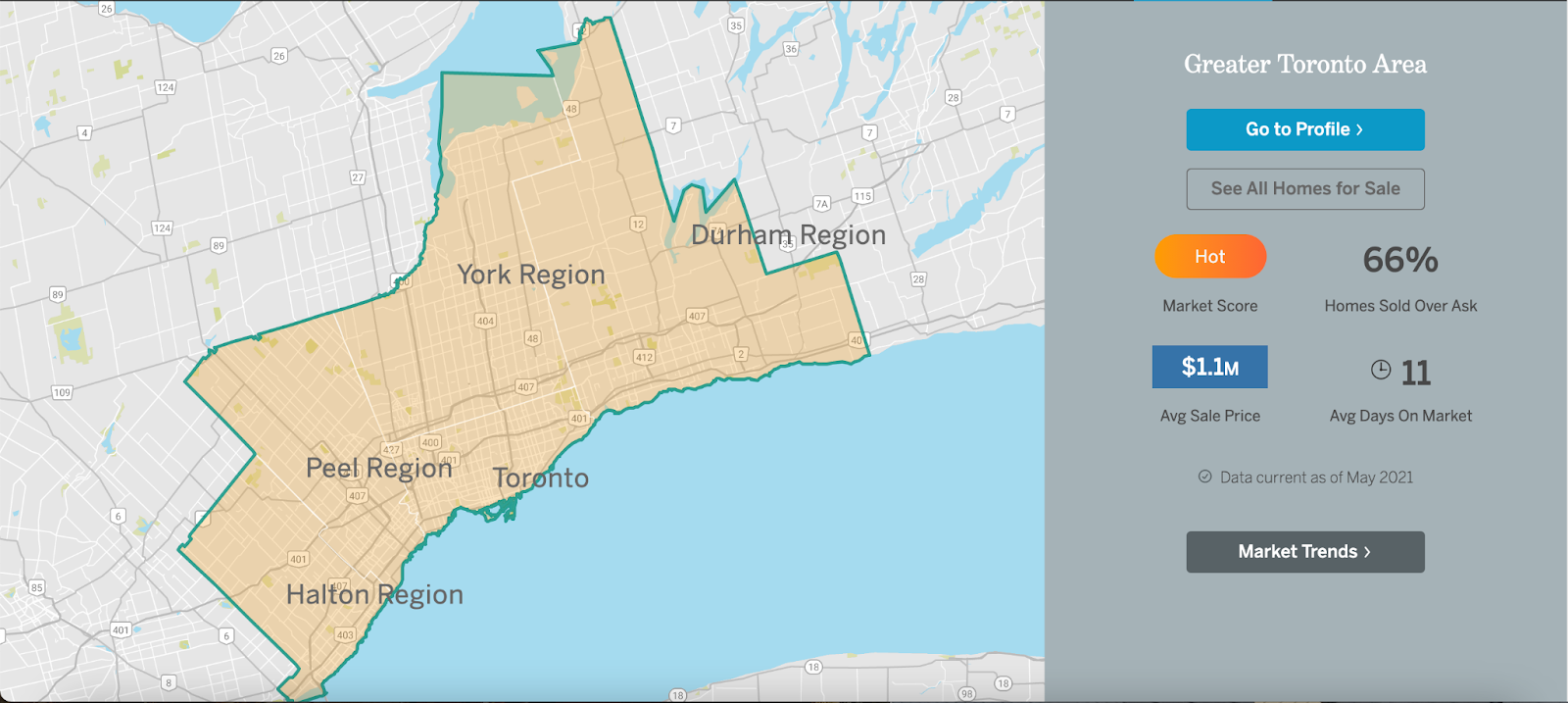

See Market Performance by Neighbourhood Map, All Toronto and the GTA

Greater Toronto Area Market Trends