FREE PUBLIC WEBINAR: WATCH REPORT HIGHLIGHTS & Q/A - Thursday June 15th 12PM ET

Join John Pasalis, report author, market analyst and President of Realosophy Realty, in a free monthly webinar as he discusses key highlights from this report, with added timely observations about new emerging issues, and answers your questions. A must see for well-informed Toronto area real estate consumers.

Toronto’s housing downturn didn’t last very long.

Toronto area house prices peaked in February 2022 at $1,679,429; by July 2022, prices had fallen by 23% to $1,285,222. Average prices remained flat for the second half of 2022, but accelerated in 2023. The average house price in May was $1,472,879, up by $200K since January and up 2% over last year.

This dramatic rebound in house prices has largely been due to a shortage of listings. Last month there were 5,474 active detached listings available for sale in the Greater Toronto area. That was the second-lowest number of active listings for May going back to 1996.

The lack of inventory is driving the intense competition we continue to see on the ground, with two-thirds of all houses selling above the seller’s list price.

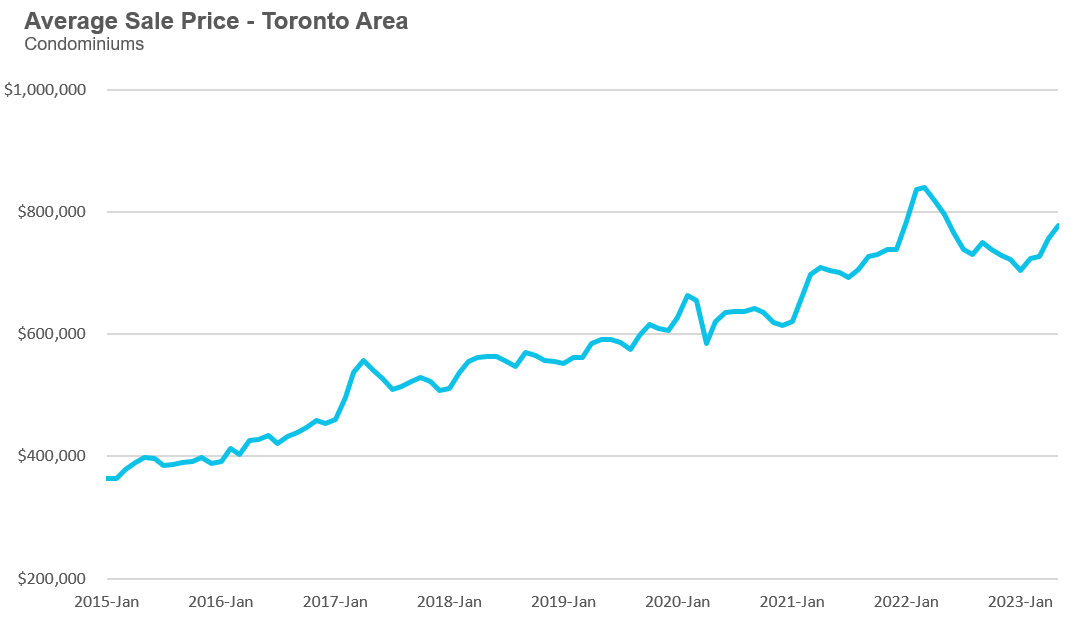

Condos have also seen prices recover, with the average sale price of a condo up 10% since the start of the year and down just 2% over last year. While the condo market is still a seller’s market, it is less competitive than the market for houses.

In spite of this run up in prices, I expect the market to start to cool down and price growth to moderate in the months ahead. The summer months are typically much slower than the spring market; many active buyers pause their search to take a break after months of frantic searching and lost offer nights.

And beyond these reoccurring seasonal trends, the Bank of Canada’s (BoC) decision to increase its policy rate by 25 basis points this month will likely put a bit of a chill on Canada’s housing market.

Typically, a single 25 basis point increase in the BoC’s policy rate should not impact the housing market much, especially when most buyers are getting fixed-rate rather than variable-rate mortgages. But this increase is having two negative side effects on the housing market.

Firstly, bond yields (and, by extension, fixed mortgage rates) have been trending up over the past month, and this recent BoC rate increase caused bond yields to increase even further. Fixed mortgage rates are now well into the 5% range, which will increase borrowing costs, making it harder for some buyers to qualify for a mortgage.

Secondly, this increase will likely have an even more significant impact on market sentiment. When buyers rushed back into the market at the start of 2023, the sentiment was positive because most buyers believed that the BoC was done hiking interest rates and that rates would start to decline sooner rather than later. Buyers hoped that by jumping in while rates were still high, they would avoid any price acceleration caused by any future interest rate cuts. But this demand boom caused prices to accelerate even as rates remained at their elevated levels.

However, the latest increase, and the possibility of another increase later this year, is making it more apparent that not only is the BoC not done raising rates, but that interest rates will likely stay high for longer than many households expected. The recent increase in home prices and the expectation that interest rates will not be cut any time soon will help cool the urgency we saw from buyers earlier in the year.

While I’m not expecting any dramatic shifts in the market any time soon as inventory levels are still at historic lows, we should see the competition in the market moderate in the months ahead.

“We need to build 5.8 M units to restore affordability, that’s what the CMHC tells us. That works out to 760K units a year. We’ve never built more than 250-260K units a year. That’s insane!”

- Scott Aitchison

The Conservative’s “insane” plan to restore housing affordability is to triple the number of homes Canada builds each year. And how do the Conservatives plan to do that exactly? They have offered several ideas, including:

Now, if you’re thinking to yourself, the Conservative’s housing plan sounds a lot like the Liberal’s housing plan, you would be correct. The Liberals also promise to solve Canada’s housing crisis (although their government refuses to call it a crisis) by significantly increasing the housing supply.

The Conservative’s idea to give financial bonuses to cities that encourage more housing is also known as the Housing Accelerator Fund launched by the Trudeau Liberals. Almost everything the Conservatives have proposed to solve our housing crisis is borrowed from the Liberals.

This raises an important question: why does the Conservative message on housing appear to be resonating with younger voters?

To start, the Conservatives are competing against an incumbent government that has done more to inflate the cost of owning and renting a home than any previous government in recent generations. It doesn’t matter what the Liberals say regarding housing — their record speaks for itself.

Voters are connecting with the Conservative message partly out of desperation and hope that a new government will make housing affordable again. But the Conservative's approach to making this connection with voters is more of an exercise in political theatre than actual policy.

To make their approach to the housing crisis resonate with voters in spite of their policies being similar to those proposed by the Liberal government, the Conservatives have zeroed in on three keywords to make their message stick.

Gatekeepers

Canadian households are feeling tremendous stress due to skyrocketing housing costs. The Conservatives realized that the anxiety and anger Canadians feel needs to be directed towards someone or some group of people.

People need someone to blame for this crisis.

Blaming Prime Minister Trudeau for our housing crisis would have been predictable and not have resonated with voters as effectively. Instead, Pollievre’s team found another villain to blame — the Gatekeepers.

Who exactly are these Gatekeepers? Anyone who gets in the way of building more housing, including municipal politicians and so-called “not in my backyard” or NIMBY members of the public (more on NIMBYs below).

The Conservatives have achieved three important goals by blaming municipal politicians and NIMBYs for our housing crisis.

First and foremost, they found a worthy villain. With countless experts arguing that Canada needs to increase the housing supply, it makes sense to blame the people often seen as the barriers to new housing.

Second, by blaming municipalities and NIMBYs, Pollievre is trying to give voters the impression that he understands the housing crisis far better than our prime minister because he has done something Trudeau hasn’t, which is identifying the alleged root cause of the crisis.

Finally, by shifting the blame for Canada’s housing crisis to municipalities, Pollievre can deflect any questions about the role Canada’s population boom is having on the housing market. This is critical for Pollievere because he appears to want to maintain the current pace of Canada’s population boom of over 1 million people per year, triple the level of historical trends.

Fines

The Conservatives are also promising to issue fines to cities that block housing construction.

By promising to fine cities, the Conservatives are trying to position Pollievre as a political strongman who will stand up to municipalities, something they argue Trudeau doesn’t have the guts to do.

The fact that the federal government cannot issue fines to municipalities for their local zoning and planning decisions doesn’t matter because the Conservative’s housing plan is not about actual policy, but about giving voters the impression their leader can do what Trudeau can’t.

NIMBYs

The last keyword the Conservatives have integrated into their communication strategy regarding housing is incorporating the term NIMBY. An acronym for ‘Not In My Back Yard’, NIMBY is a pejorative term for any person opposing new housing construction in their neighbourhood.

Conservative housing critic Scott Aitchison posted a thread on Twitter this month arguing that NIMBYs are among the gatekeepers preventing the supply of new housing. While there is some truth to this, as local homeowners can have far too much influence over the types of homes that get built via the municipal planning and appeal process, the Conservative’s decision to target NIMBYs may eventually be problematic down the road.

By focusing much of their communication strategy on NIMBYs, the Conservatives are dog-whistling to a particular group of voters, the large cohort of YIMBYs (‘Yes In My Back Yard’ advocates) living in Toronto and Vancouver who believe that if municipalities reformed their zoning policies to allow for more housing to be built, there would be no limit to how many homes Canada could build. And Pollievre’s message appears to be connecting with this young voters.

But by positioning themselves as YIMBYs, the Conservatives may find themselves trying to attract two groups of voters with very different views on housing policies. YIMBYs aren’t just fighting for more condos; they want municipalities to end exclusionary zoning policies that only allow the construction of single-family homes in most neighbourhoods. The City of Toronto’s recent decision to allow up to four homes (4-plexes) to be built on a single family lot anywhere in the City of Toronto is a good example of the type of reform that YIMBYs want. But is this the type of reform the majority of the Conservative voter base wants to see from municipalities?

Likely not.

A recent tweet by Conservative member of parliament Greg McLean reflects how many suburban voters feel about a mini-apartment building going up across the street from them. They don’t want them to be legal as of right. Neighbours want to be consulted whenever someone wants to build a fourplex - a process that makes building this type of housing more challenging.

If the answer is yes, they may make some strides By appealing to YIMBY voters, the Conservatives risk alienating the suburban voters they depend on.

The Conservatives are walking a slippery slope.

In Conclusion

There are plenty of reasons for Canadians to be angry with and distrust the current federal Liberal government regarding the high cost of housing. But those hoping that Pollievre’s Conservatives will do a better job of improving housing affordability need to ignore the strongman rhetoric and take a moment to look closer at what the Conservatives are actually proposing. There are few ideas or policies materially different from what the Liberal government is already doing. And all the talk in the world about Gatekeepers, Fines and NIMBYs will likely do little to move the needle on housing affordability.

House sales (low-rise freehold detached, semi-detached, townhouse, etc.) in the Greater Toronto Area (GTA) in May 2023 were up 18% over the same month last year.

New house listings in May were down 19% over last year and well below historic new listing volumes for the month of May.

The number of houses available for sale (“active listings”) was down 25% when compared to the same month last year.

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number of homes that sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell, given the current level of demand? The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

While the current level of MOI gives us clues into how competitive the market is on-the-ground today, the direction it is moving in also gives us some clues into where the market may be heading.

The MOI for houses remained relatively flat at 1.3 MOI in May. This puts the market for houses deep into seller’s market territory.

The share of houses selling for more than the owner’s asking price increased to 66% in May.

The average price for a house in May was $1,472,879 in May 2023, well below the peak of $1,679,429 reached in February 2022 but up 2% when compared to the same month last year.

The median house price in May was $1,295,000, up 4% over last year, but below the peak of $1,485,000 reached in February 2022.

The median is calculated by ordering all the sale prices in a given month and then selecting the price that is in the midpoint of that list such that half of all home sales were above that price and half are below that price. Economists often prefer the median price over the average because it is less sensitive to big increases in the sale of high-end or low-end homes in a given month which can skew the average price.

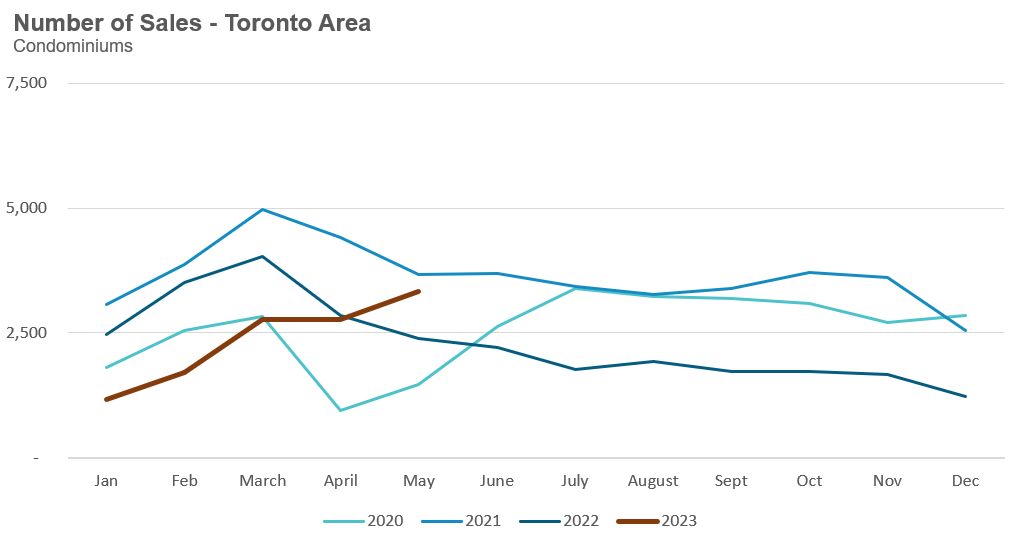

Condo (condominiums, including condo apartments, condo townhouses, etc.) sales in the Toronto area in May 2023 were up 39% over the same month last year.

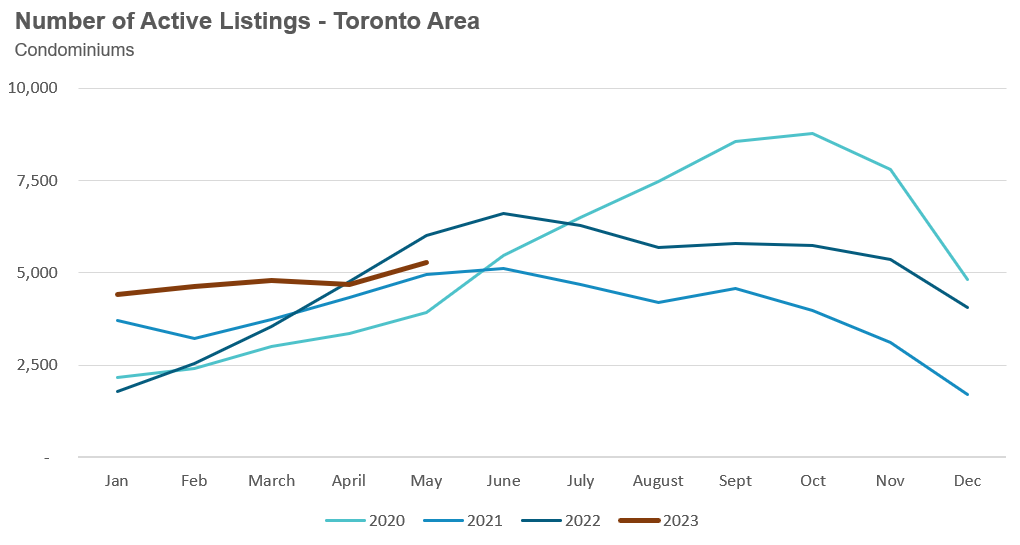

New condo listings were down 14% in May over last year.

The number of condos available for sale at the end of the month, or active listings, was down 12% over last year.

Condo months of inventory remained relatively flat at 1.6 MOI in May, which puts the condo market in seller’s market territory.

The share of condos selling for over the asking price remained unchanged at 43% in May.

The average price for a condo in May was $778,428, down from the peak of $840,444 in March 2022, and down 2% over last year. The median price for a condo in May was $700,000, down 3% over last year, and down from the March 2022 peak of $777,000.

Across the GTA, new listings are down by double digits while sales are up over last year which has helped push prices up year-over-year in four out of the five regions.York Region is one of the hottest regions in the GTA right now for houses with sales up 45% over last year and prices up 5% over last year.

Condo sales are up anywhere from 23% in Durham to as much as 92% in York. New listings are down over last year across all regions, with York Region seeing only a modest decline. Average prices are down slightly over last year.

See Market Performance by Neighbourhood Map, All Toronto and the GTA

Greater Toronto Area Market Trends