“If CMHC Is In fact worried about home prices falling, then policies that make It harder for home buyers to obtain a mortgage only amplify these downside risks”

-

“When the demand shock from COVID unwinds and once owners have experienced life at the cottage during the winter, we will see If the prices reached as a result of this exogenous demand shock can be maintained”

-

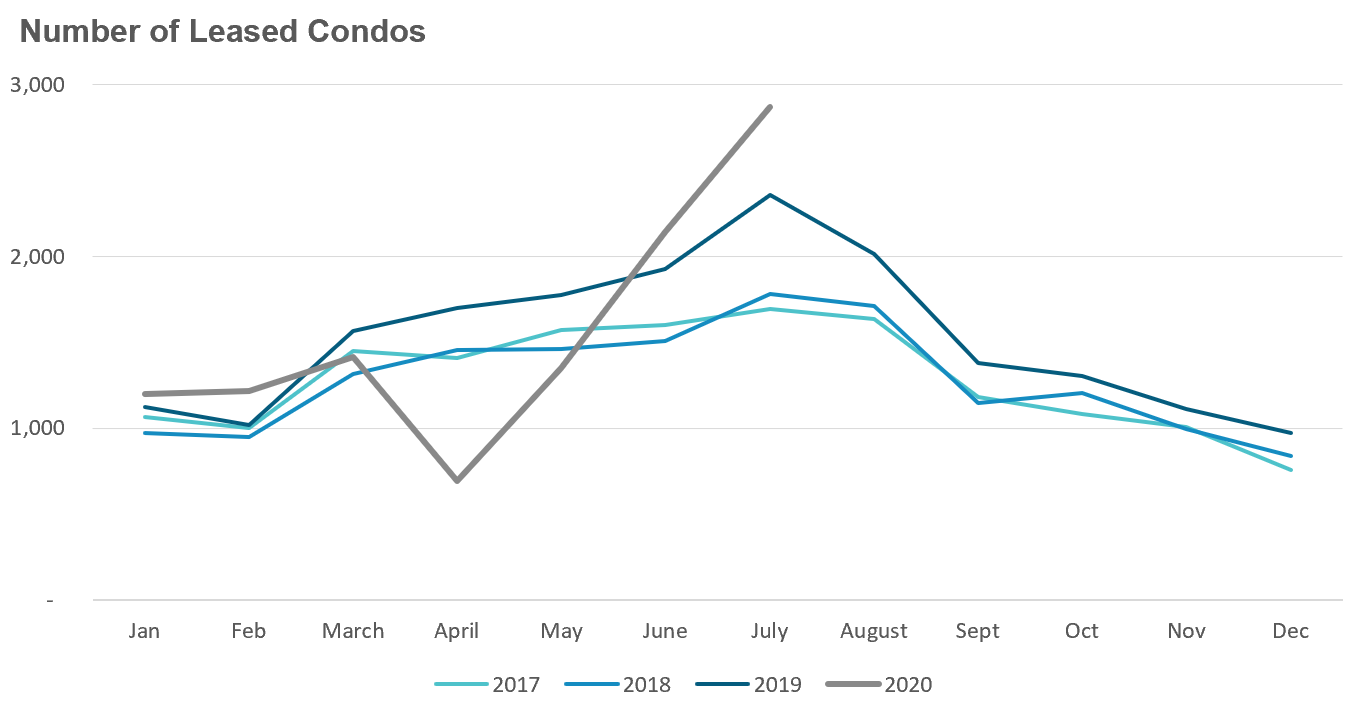

The big trend we are seeing in the condo rental market is declining rents. Average rents in Central Toronto (the old City of Toronto) peaked at $2,721 in September 2019 and have since declined 14% to $2,343 in July,2020.

What's Interesting about this trend is that it's not really driven by a decline in demand. Year to date the total number of condos leased is only down 5% compared to last year.

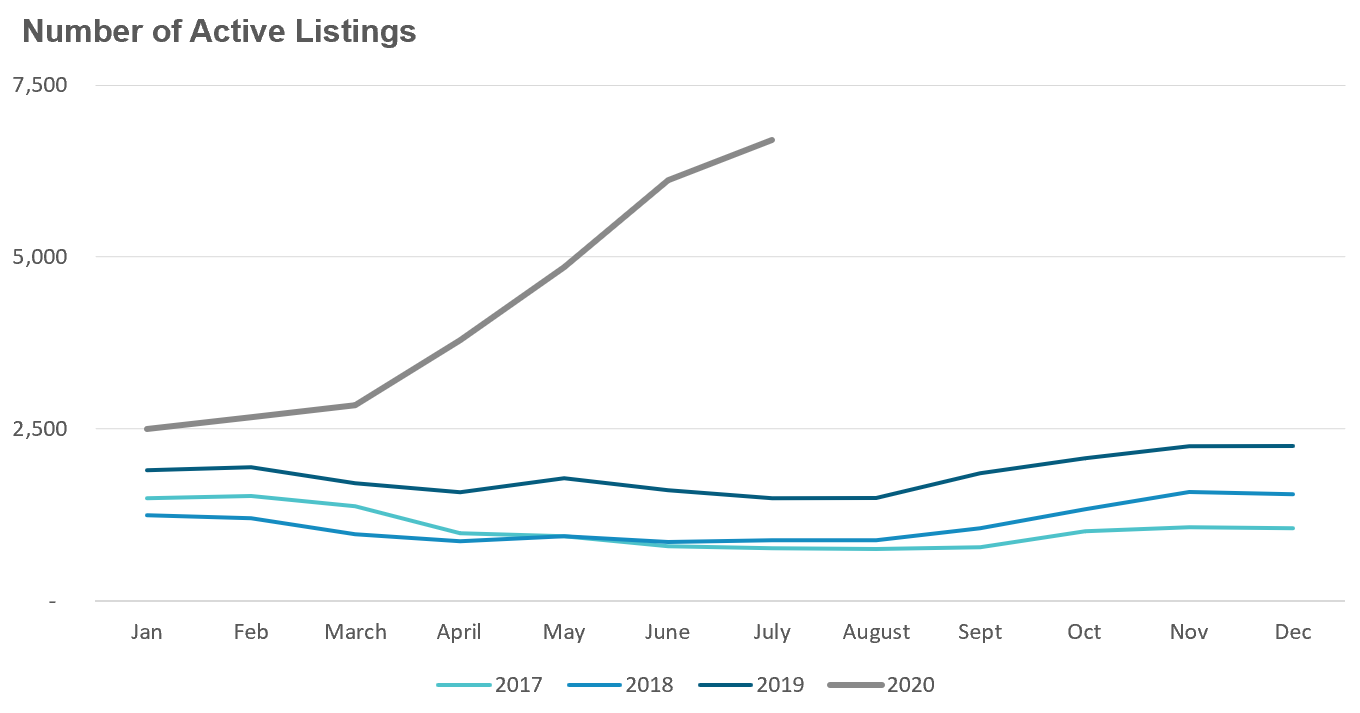

What's driving this decline in rents is a surge In condo rental listings. In July 2020 there were 6,697 condominiums available for lease compared to just 1,492 last year, a 350% increase.

What's driving this spike in listings? A combination of factors.

Firstly, according to condo research firm Urbanation, nearly 11,000 new condominiums were completed during the first half of 2020 many of which were purchased by investors and made their way Into the pool of condo rentals. We have also seen an Increase In listings from condominiums that were previously being rented as short term rentals on websites like Airbnb but have since been moved to the long term rental market.

Students who leased out condominiums for the upcoming school year but have decided to stay home are now trying to get out of their leases. In these situations the landlord is obligated to list those units for lease In order to mitigate the tenant's damages. Finally, we are also hearing that some condo tenants are leaving large crowded buildings In favour of renting in houses with more outdoor space or moving out of the city entirely, a reaction to the COVID pandemic.

In the months ahead we'll be monitoring whether condo rental listings continue to outpace demand for rentals which could put further downward pressure on rents and what impact if any this might have on the resale condo market.

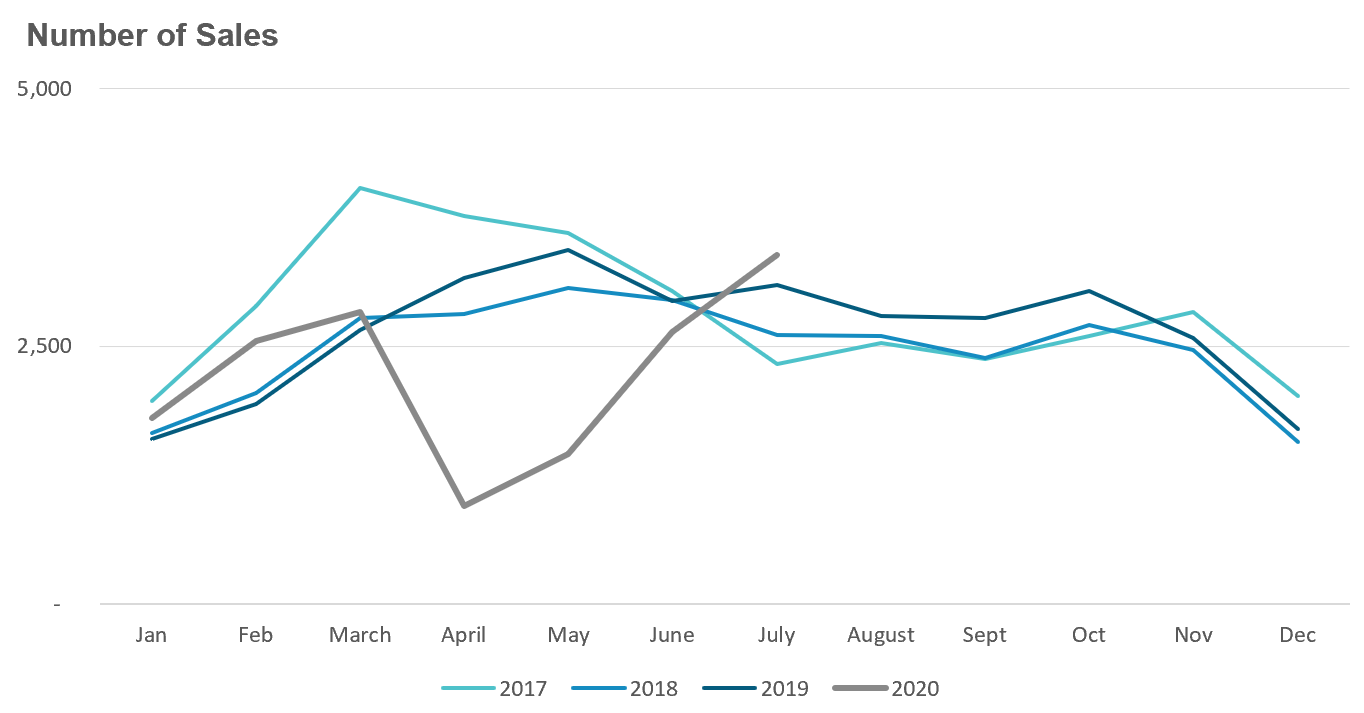

While year over year comparisons are slightly misleading, the rebound In sales Is still an encouraging sign that home buyers are confident and have returned to the market.

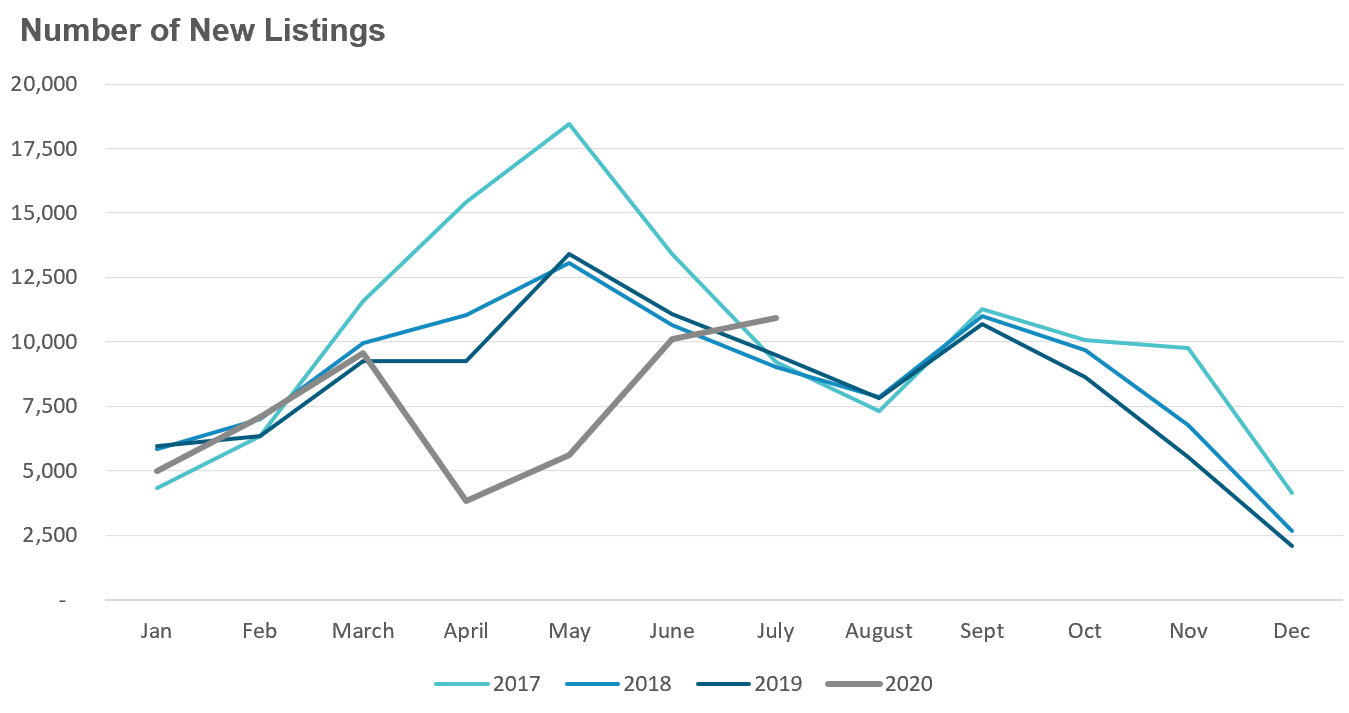

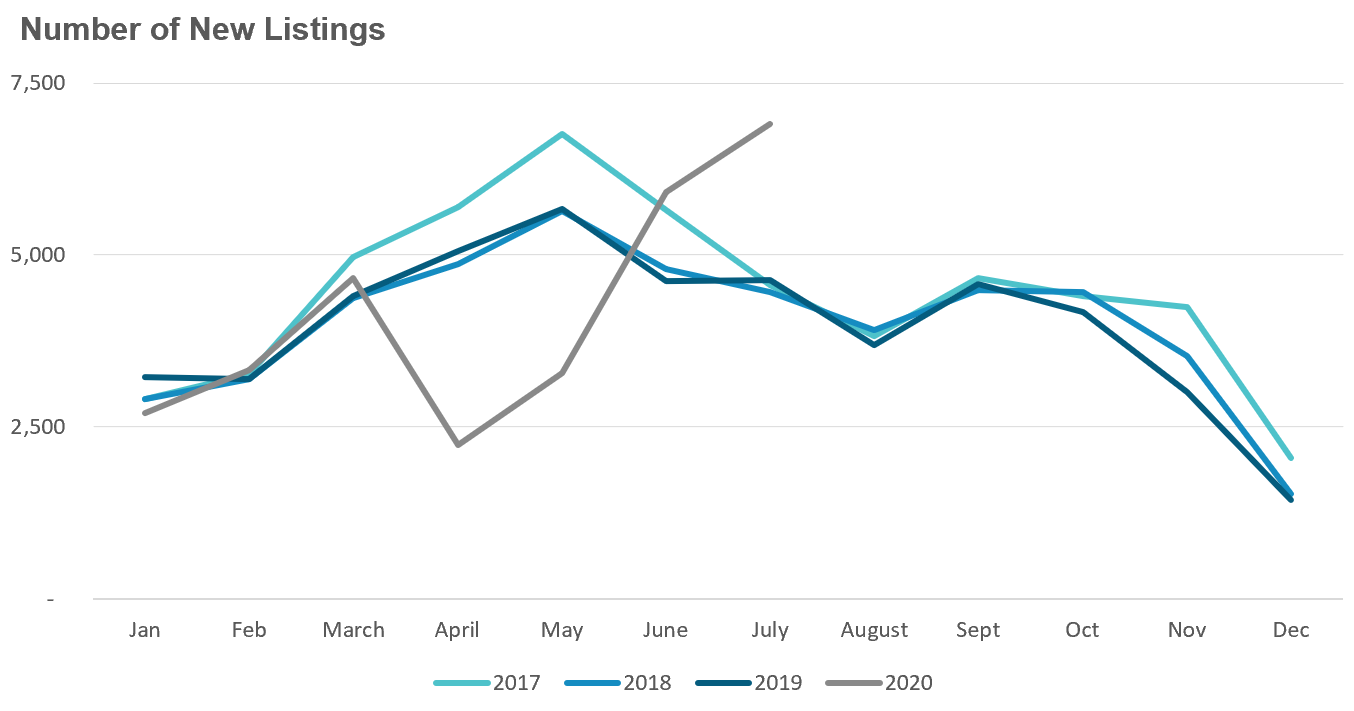

While we did see a 15% increase in the number of new low-rise listings in the Toronto area in July, there were still 30% fewer homes available for sale in July then there were the same month last year.

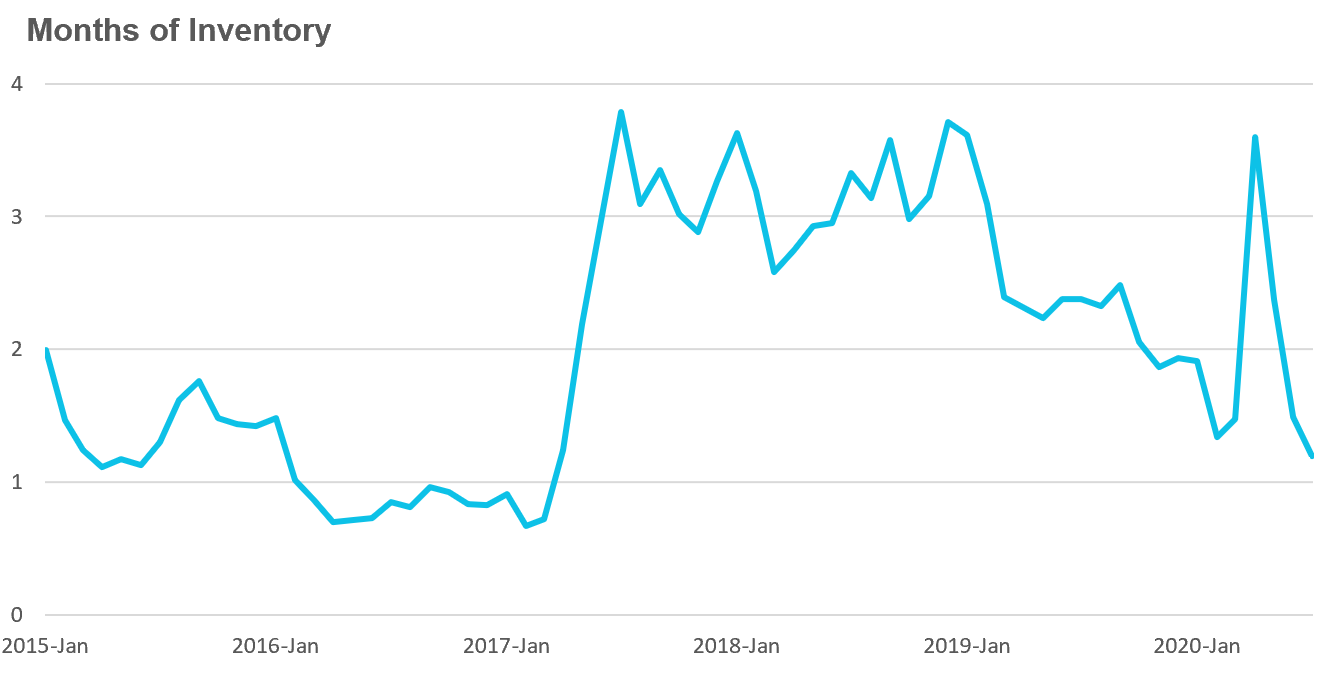

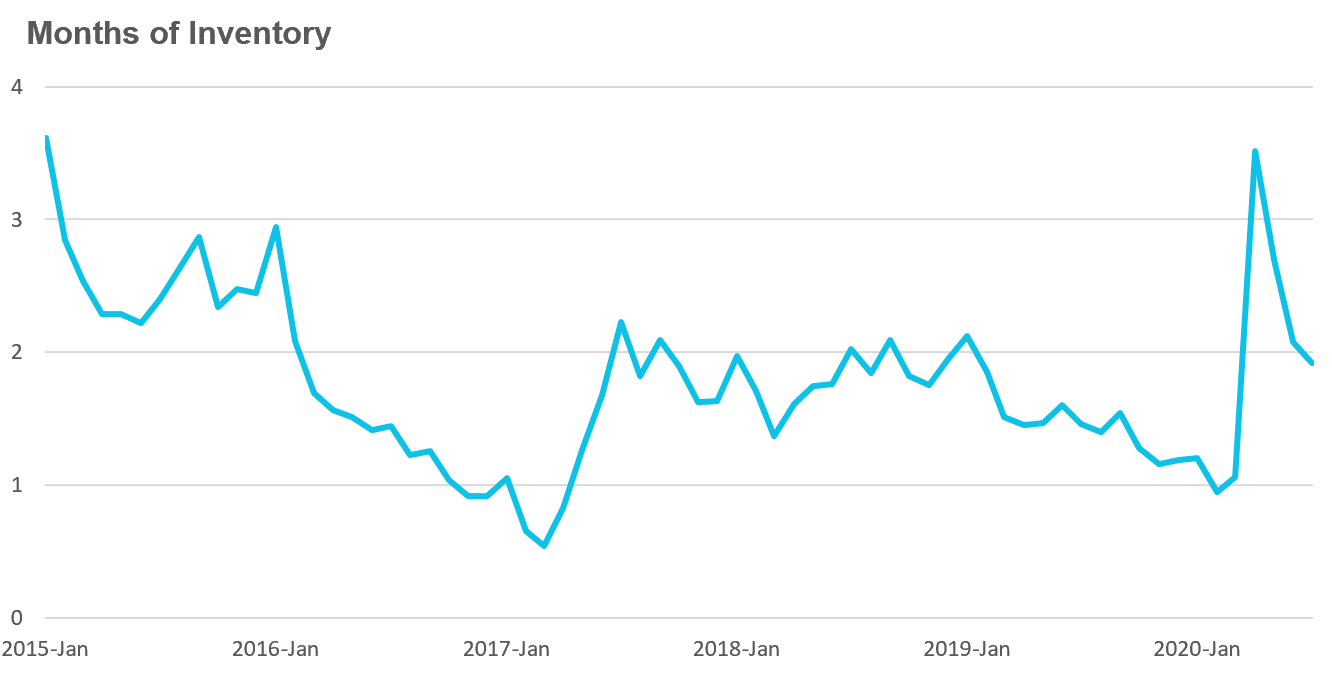

The Months of Inventory (MOI) looks at the number of homes available for sale In a given month divided by the number homes that sold In that month. It answers the question, If no more home homes came on the market for sale how long would It take for all the existing homes to sell given the current level of demand.

The higher the MOI the cooler the market Is. A balanced market (a market where prices are neither rising or falling) Is one were MOI is between 4-6 months. The lower the MOI the more rapidly we would expect prices to rise.

In April the MOI spiked to 3.6 months, not because the number of houses on the market surged but because demand plummeted. This resulted In a far cooler market than we saw during the first couple of months of the year. Since then, the surge In demand and the muted new listings volume has pushed the MOI to just over one month making the market for houses Incredibly competitive right now.

While the current level of the MOI gives us clues Into how competitive the market Is on the ground today, the direction It's moving In also gives us some clues Into where the market may be heading and right now the real estate market Is still heating up. We'll need to see the MOI Increase In the months ahead for house price appreciation to cool.

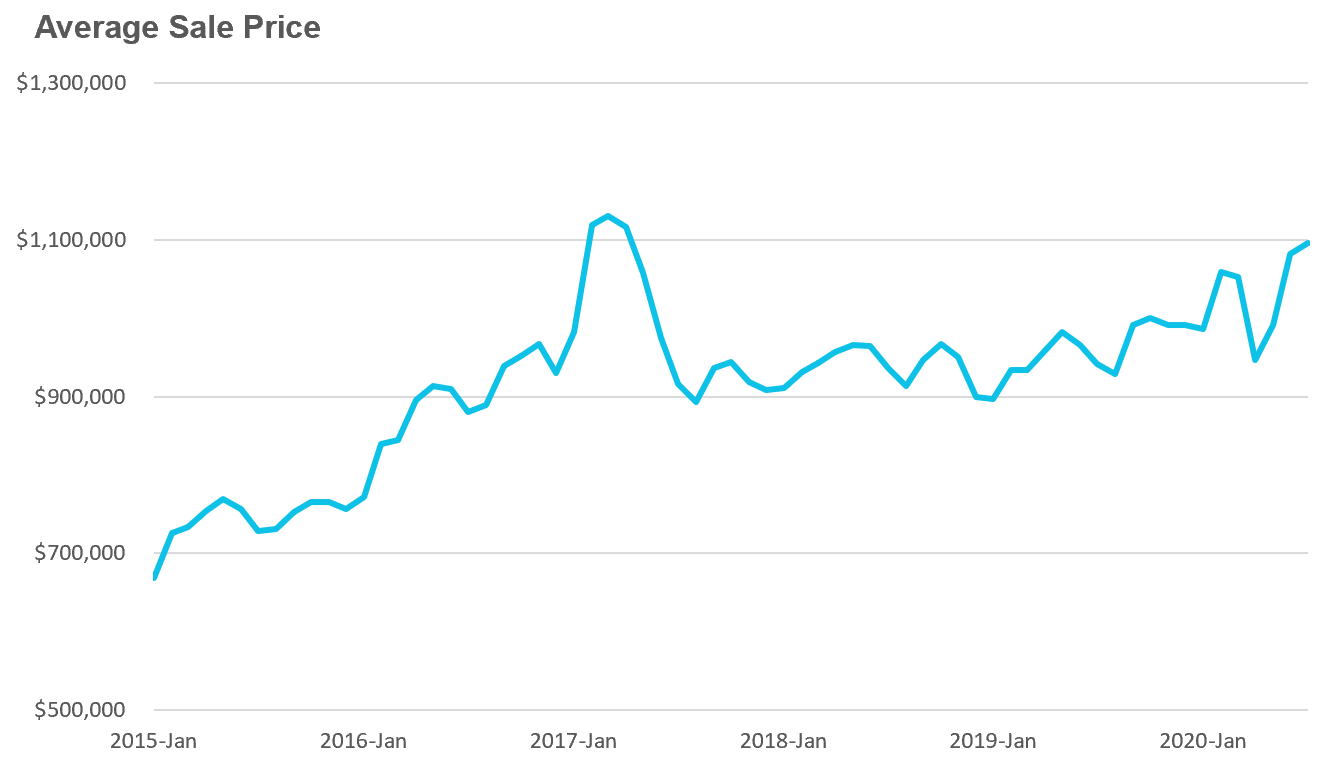

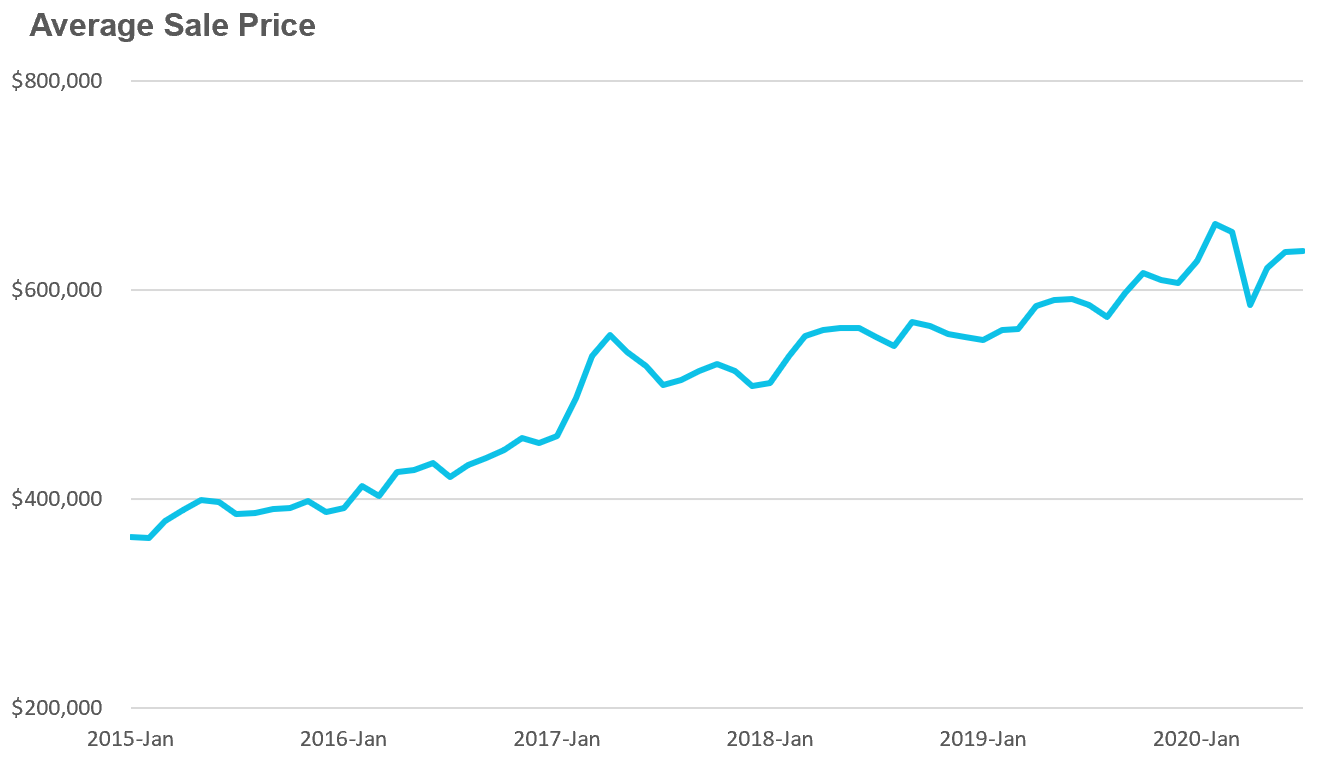

Strong demand coupled with very low Inventory levels helped push average house prices up 16% over last year.

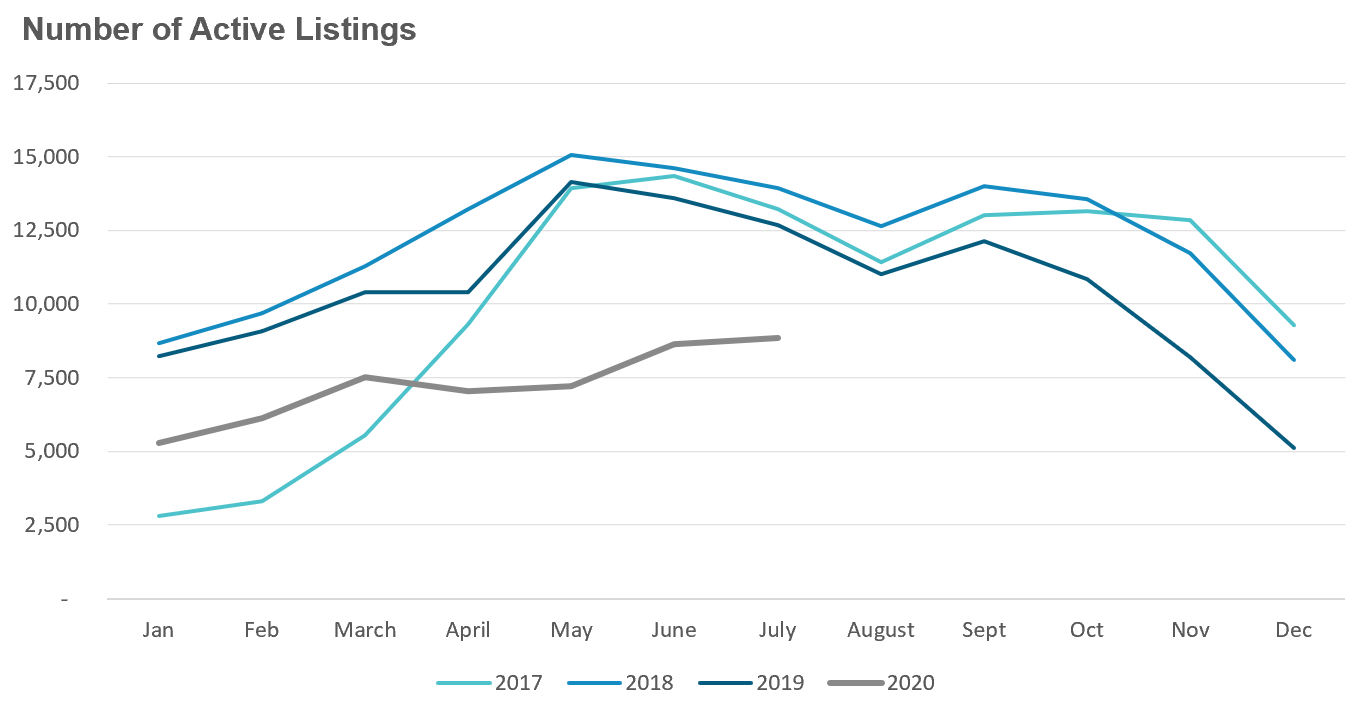

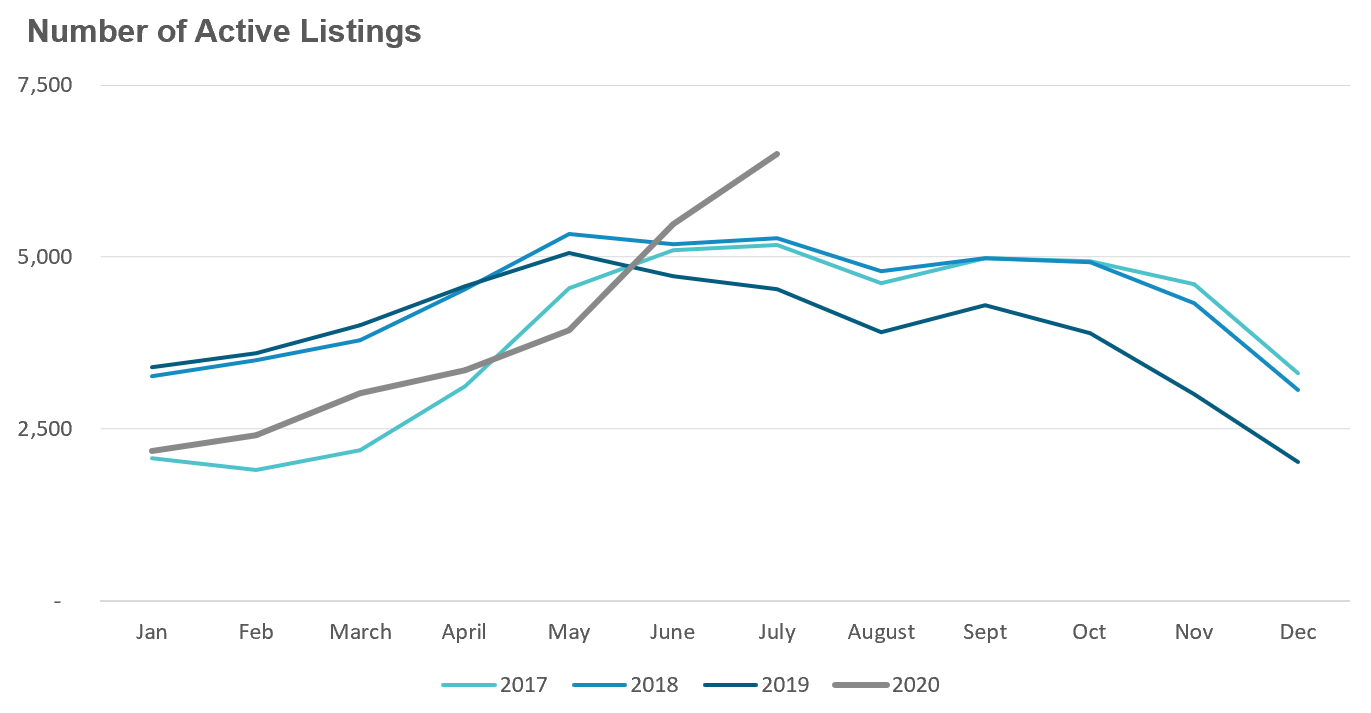

New condo listings surged by 49% In July which pushed the active number of condos available for sale In July (inventory) up by 43%.

Despite the surge In Inventory, the condo market was more competitive In July than It was three months ago because sales Increased at a faster rate than Inventory. The MOI declined from 3.5 months In April to just under 2 months In July.

The tight Inventory In the condo market helped push average prices up 9% over last year

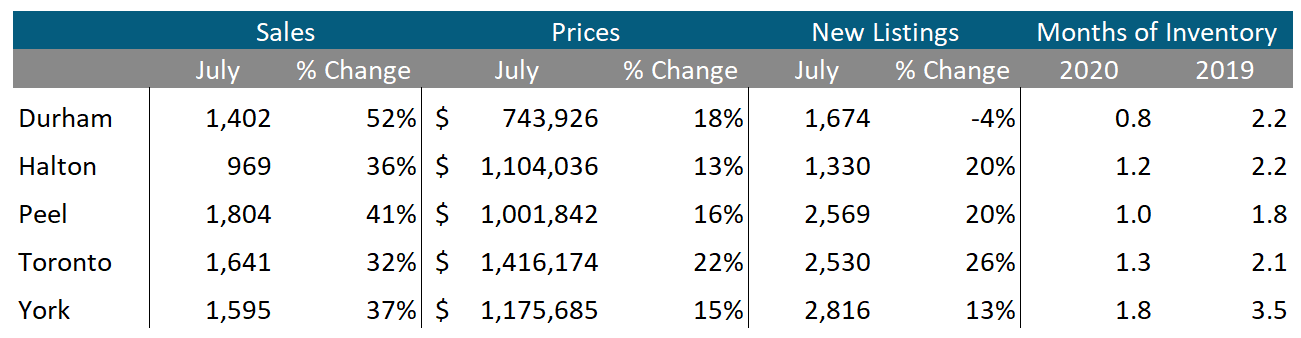

We can see that sales and prices are up across all five regions In the Toronto Area. New listings were up In all regions aside from Durham which saw listings fall 4% over last year.

The MOI Is down significantly In all five regions when compared to last year which tells us the market Is more competitive than It was a year ago.

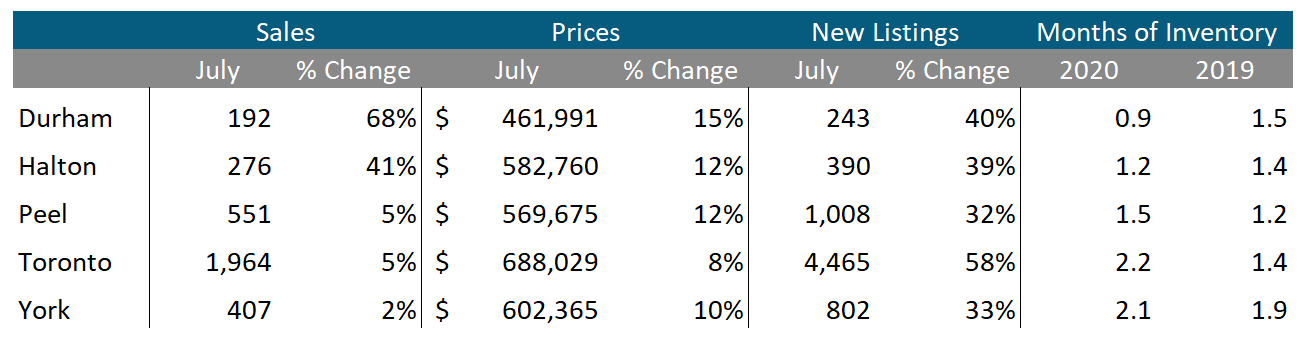

Condo sales saw big Increases In Durham and Halton but both are relatively small markets for condominiums. The MOI for Toronto's condo market Increased from 1.4 months last year to 2.2 months this year showing that the condo market was cooler last month than It was a year ago.

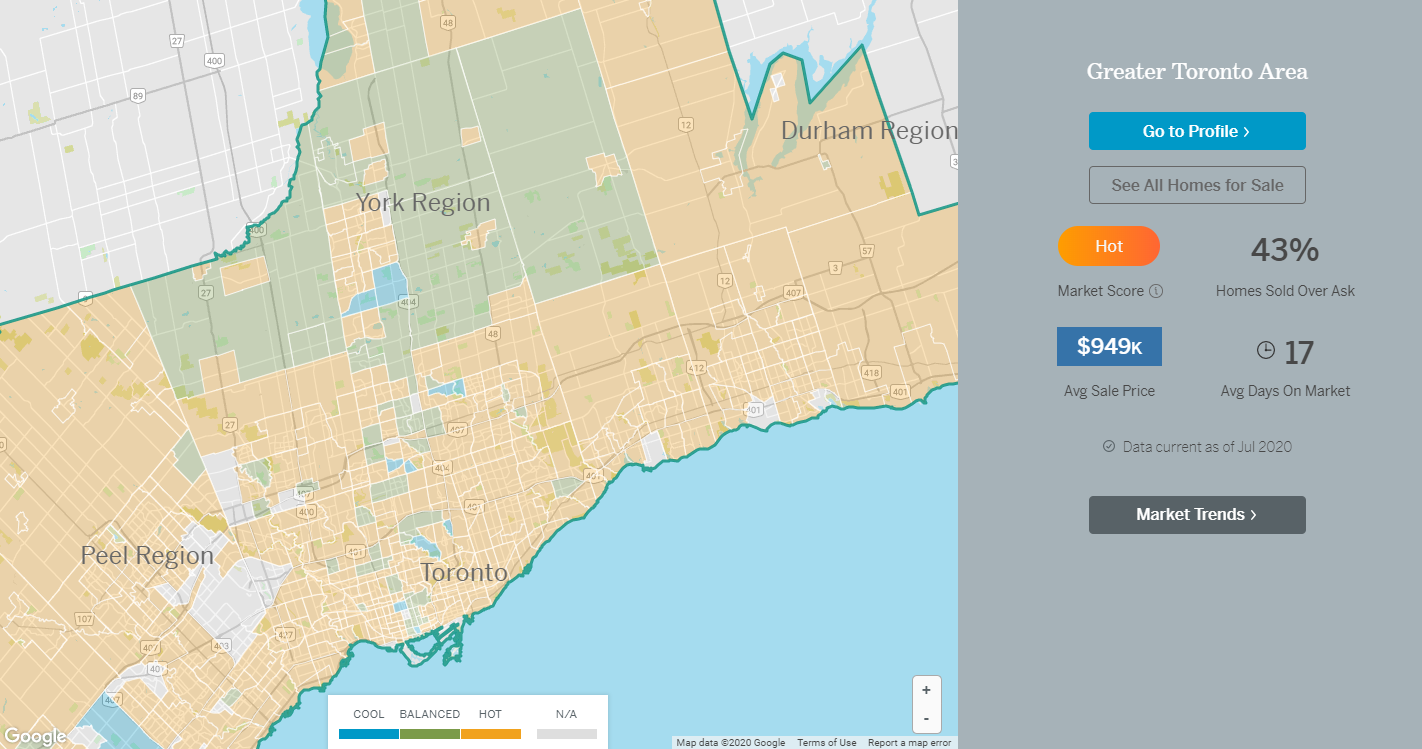

Greater Toronto Area Market Trends