Toronto's housing market is typically very competitive which means it can take many months and many bidding wars for a buyer to successfully purchase a home. For this reason, buyers often buy a new home first and then list their current home for sale, ensuring that they have a place to live before selling their home which shouldn't be a problem in a hot market.

But I train my agents at Realosophy Realty to caution home buyers that selling a home after can expose you to considerable risk. If a home is not getting many showings and no offers, buyers will feel significant pressure to reduce their price well below what the property is worth in order to secure the sale that they need to make their new purchase work.

In some cases, sellers cannot reduce their price that much because they need to sell their home at a certain price in order to afford the home they just bought.

If a seller can't sell their home for the price they need, they will typically be unable to obtain financing on the home they just purchased and will have to default on that transaction which may result In legal action against them from that seller.

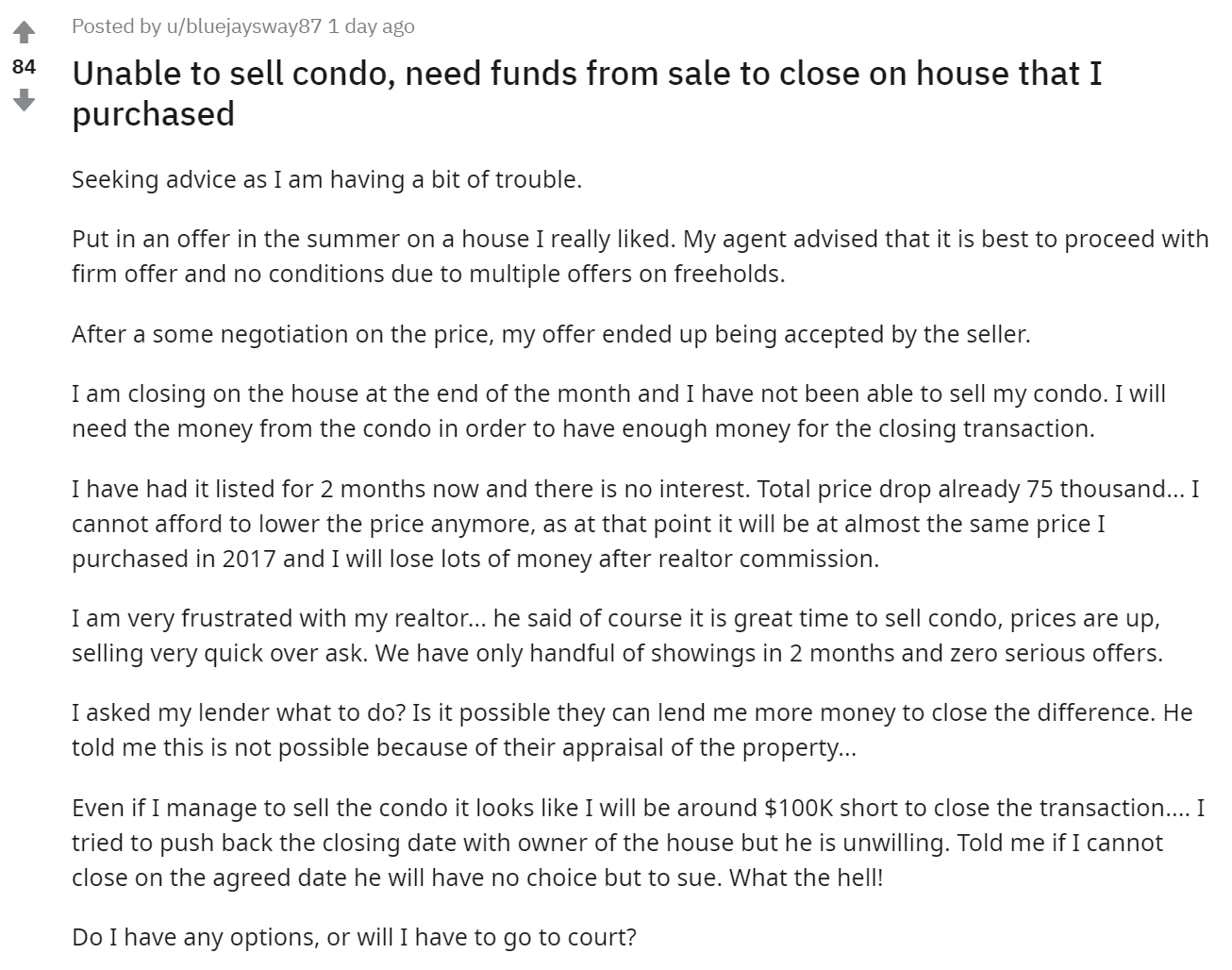

As Toronto’s market sees a widening gap between a competitive market for houses and a cooling market for condos (more on this further in this report), this risk has become even more acute, as detailed in this recent post on Reddit which gives us a very visceral real life look at the risks and challenges that a buyer-seller could face in this type of situation.

The way to avoid this type of stress is to sell your home first and then start your search to buy your next home. The risk to this approach is that if your home search takes longer than planned, you would need to move into a short-term rental or stay with family or friends for that period of time.

Weighing the risks against each other, of course, moving into a short term rental is not that bad when compared to incurring significant financial losses due to a botched home sale.

In a volatile market like we are seeing in the Toronto area today where behaviours in and beliefs about the economy and housing market can change overnight, the risks of buying a home before selling have perhaps never been higher.

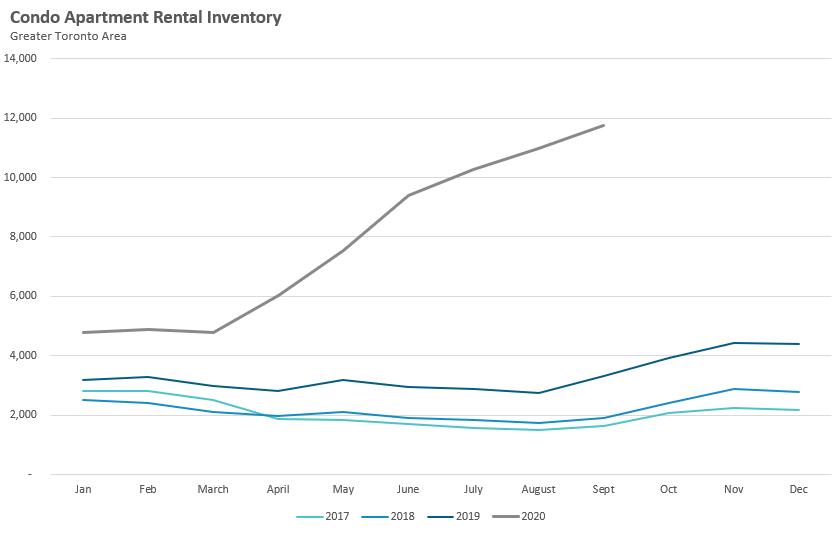

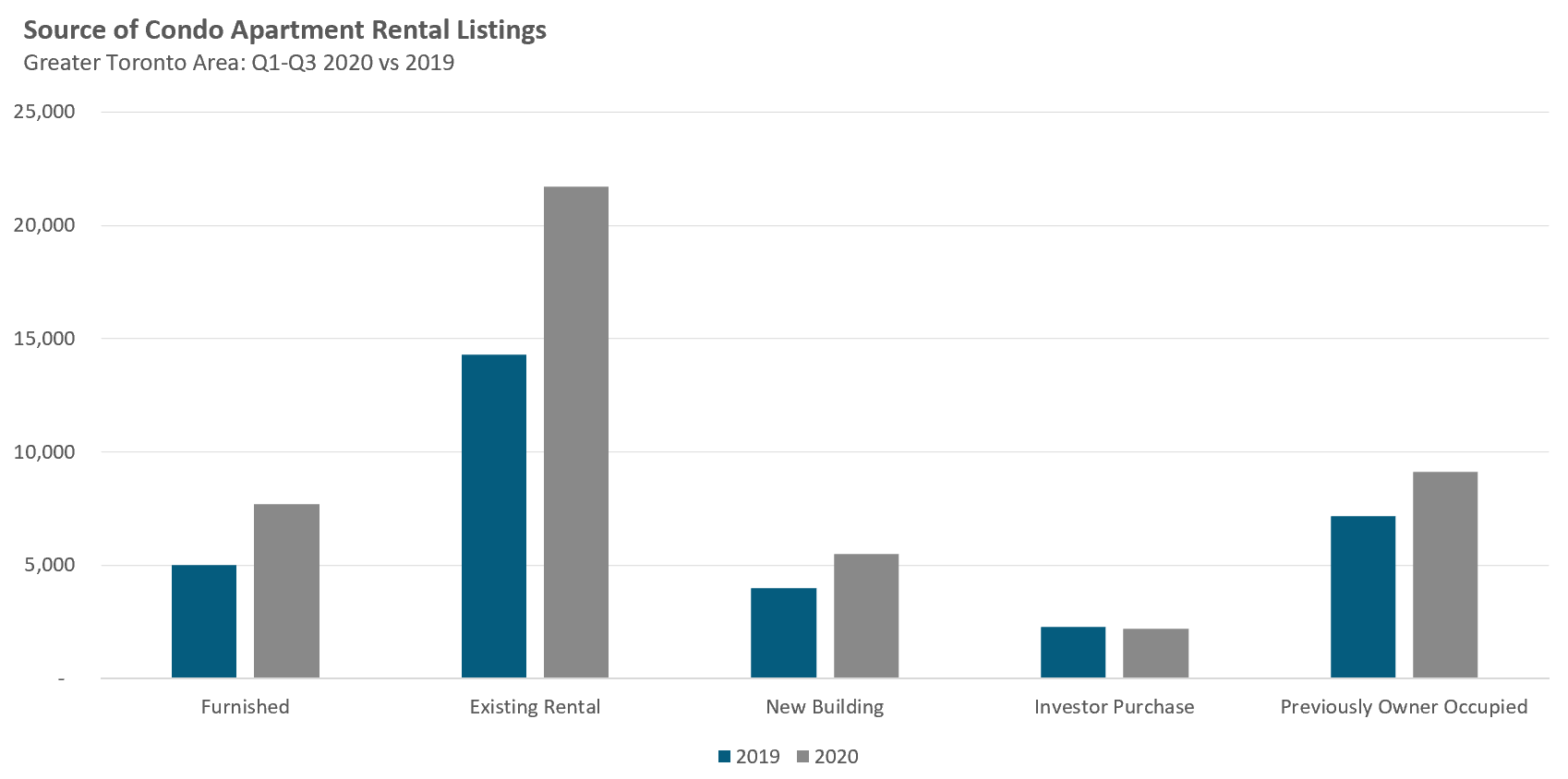

In September, there were just under 12,000 condo apartments listed for lease on Toronto's MLS system compared to just 3,332 last year.

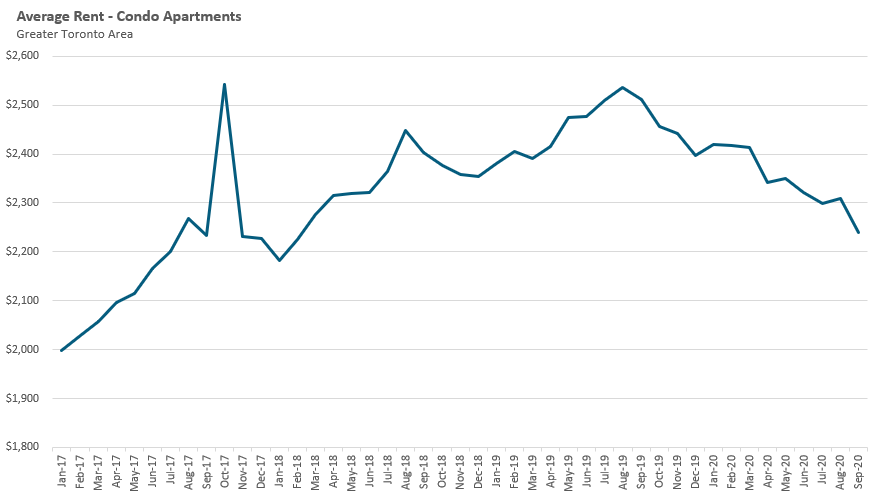

This has pushed average rents for the Greater Toronto Area down 12% from their peak last year in August. The downtown core is seeing an even bigger decline in prices with the old City of Toronto seeing average rents down 16% over last year, returning to prices last seen in early 2017.

One question I have been getting a lot Is: Where are all these condo rental listings coming from?

Is this the product of falling demand due to decline in immigration rates and foreign students due to Covid-19 travel restrictions? Or is there something on the supply side that is driving up inventory, like the number of new condo completions or former Airbnb units moving to long-term rentals as tourism drops and the City of Toronto has introduced tougher regulations? (Watch our Toronto Summit interview between Move Smartly’s Urmi Desai and Urbanation’s Shaun Hillebrand for a discussion of these factors back in July.)

To answer this question, we first look at demand numbers. While there is no price measure of rental demand, the number of leased transaction can serves as a reasonable, though imperfect proxy. When we compare the number of leased condo apartments during the first 3 quarters of 2020 to the same period In 2019, leased transactions are actually up 5% over last year.

This suggests that it is supply that has risen so this analysis will largely focus on trying to quantify the source of the rental supply that is coming on the market.

Background

Toronto's real estate market is a bit unique In that a significant number of condo rental transactions are listed for lease with real estate agents on the Toronto Regional Real Estate Board's MLS system which offers us a deep dataset that we can analyze to help find some answers to our questions (this is as opposed to many markets in which agents do not assist with as many condo rentals and so no such data is captured on MLS systems).

Between January and September 2020 there were a total 46,193 unique condominium apartments listed for lease In the Greater Toronto Area, compared to 32,735 units during the same months In 20191.

This means there were an additional 13,458 condos listed for lease during the first three quarters of this year compared to last year.

To answer the question of where this supply surge is coming from, we are going to analyze all the rental listings in each year and categorize them into one of five categories based on their current and historical MLS data.

For all unfurnished rentals, we will effectively look back in time to see whether the last transaction on that unit in the MLS system was a sale or lease and we will note when that transaction occurred. We will also be referring to the completion date of the condominium in cases where there were no previous transactions for a given unit.

The five categories we'll segment rental listings into are described below:

Furnished Rentals

Most long-term rentals (with a minimum 1-year lease) are typically leased unfurnished. Furnished rentals are typically for shorter periods of between one to six months, but more recently they are being advertised for longer terms. Because this suggests that units that were previously being rented out on third-party short-term rental websites like Airbnb which were typically furnished are now being offered for longer term rent on the MLS, we will categorize furnished rental separately; for the purposes of this analysis furnished includes any units that were either fully or partially furnished.

Existing Rental

If the last completed transaction on the MLS system for a current rental listing was a lease, then it suggests that this unit was occupied by a tenant who decided to vacate the unit. Since this unit was occupied by a tenant already, this unit is considered to be part of the existing condominium rental pool.

All other units fall into one of these remaining categories:

New Building

Any rental that is in a condominium that was completed within the past 12 months is classified as a rental listing in a new building and considered to be part of new rental supply coming on the market, provided that the unit does not fall into the Existing Rental category above.

Investor Purchased

If a unit listed for lease was purchased within the past twelve months, it suggests that this unit was purchased by an Investor as an income property.

Previously Owner-Occupied

Many condo owners who move out of their units into a house often keep their condo as an income property (i.e., to rent out to tenants). Any unit where the last completed transaction on the MLS was a sale more than a year ago or if there are no completed transactions on the MLS for the unit (e.g., as in the case where the unit was bought pre-construction and the owner moved directly into it) It is considered to be previously owner-occupied.

While this analysis categorizes every listing into one of the above categories, it is important to note that these categories are rough estimates; there are gaps and assumptions in this data and analysis.

For example, a condominium that was completed five years ago and was listed for lease for the first time this year would fall into the "Previously Owner Occupied" category. But we don't know If the owner occupied the unit – we are assuming that they did. The owner could have instead kept the unit empty for five years, rented it out on private (non-MLS) listing websites or they could have been using it as a short-term rental on websites like Airbnb.

That being said, the risk of misallocating a particular unit should apply equally to both periods in our year over year analysis. To mitigate the risk that units are being misallocated differently across time, we have observed and tested for changes in the distribution of key parameters across time.

Results

The chart below shows the source/category of each rental listing for the first three quarters of 2020 compared to the first three quarters

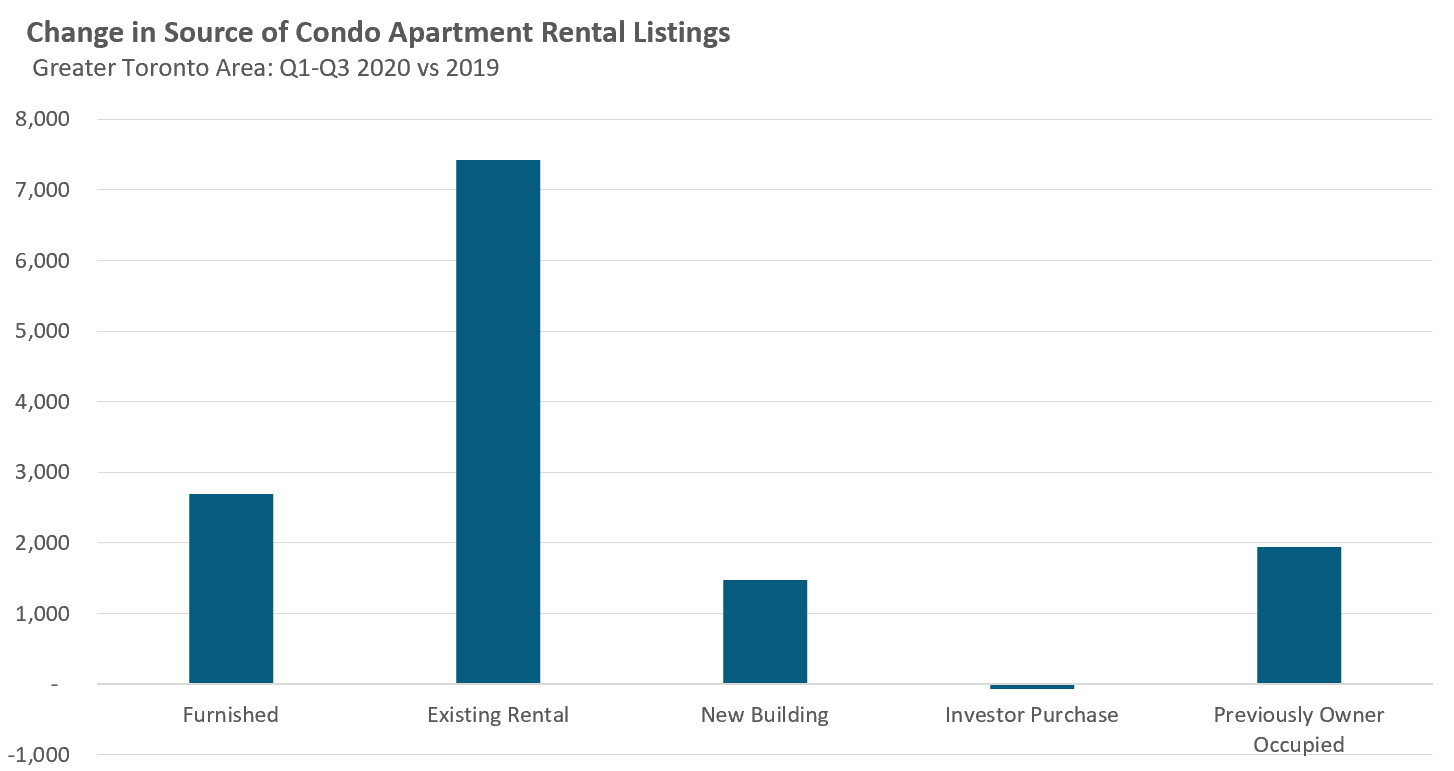

Focusing on the change (or difference) in the source of rental listings between 2020 and 2019 will give us a clearer picture of where the additional 13,458 condominiums listed for lease in 2020 came from.

There were an additional 2,686 furnished rentals listed for lease in 2020 vs. 2019 accounting for 20% of the increase in new rental listings. Recall that longer-term furnished rentals are normally much rarer compared to their non-furnished counterparts on the MLS. It is assumed that many of these additional furnished rentals on the MLS were units that were previously being rented out as shorter-term furnished rentals on websites like Airbnb.

However, the bigger story is the majority of the increase (55%) in new rental listings appears to be units that were previously rented to tenants who have decided to vacate their units; the vast majority of these units are in the City of Toronto.

There are few factors likely driving the increase in renters vacating their units, particularly in Toronto.

Firstly, renters were disproportionately impacted by the economic shocks of the Covid-19 pandemic, many of whom tend to work in hard hit sectors like hospitality, travel and tourism which have seen a sharp reduction in hours worked or outright job losses. Those affected would need to look to more affordable living arrangements including moving back home with family, a trend that is common during recessions.

But job loss is not the only reason to move back home with family. Many millennials who are able to work from home have left their rentals to move back in with parents in order to save money now that Covid-19 has wiped out the main motivators for paying downtown rents – avoiding long commutes to jobs and benefiting from the downtown lifestyle of cultural amenities and night life. In some cases, students who were living in downtown condos owned by their parents have left them for their family homes as classes have moved online.

In addition, the specific dangers posed by Covid-19 has many renters wary of densely populated high rise buildings with many shared indoor communal areas. Rentals in low-rise duplexes or triplexes offer more seclusion and more outdoor space and it is noteworthy that average rents for units in houses have not seen a decline in prices so far.

So it appears that the main driver of new rental listings supply is not from a “new” source of supply such as units previously being rented out as Airbnbs or, as we will look at next, newly completed condo buildings being rented out by investors or owners, but existing supply being vacated. The increase in condo rental listings is mainly due to a sharp decline in demand for condo rentals due to the Covid-19 pandemic, particularly in downtown Toronto, where the majority of condo rentals are.

On the supply side, we see in the above chart that new condo completions accounted for 11% of the increase in new rental listings this year vs. last year. There was a 1% decline in the number of rentals attributed to investor purchases and a 14% increase in rentals previously owner occupied.

Overall, these results suggest that we are not out of the woods yet and that we will likely see further downward pressure on the Toronto area rental market.

The decline in demand for downtown Toronto condos will continue as work-from-home and other pandemic restrictions appear set to continue well into 2021.

The transfer of short-term to longer term rental supply looks set to continue as well. The City of Toronto's short term rental registration system went live In September and all Airbnb operators will have to register their units by the end of this year. The new rules only allow homeowners to rent their principal residence for up to 180 nights per year. Many of these Airbnb rentals may find their way Into the long term rental market or the Investors may opt to sell their units.

The vulnerabilities facing Toronto's rental market are not new. Back In January, I discussed why the discrepancy between condo rents and prices was one of the “big vulnerabilities in the market”.

The decline in average rents we are seeing as a result of this recession has only widened the gap between condo rents and prices making the condo market even more vulnerable, particularly given that a significant number of condos in Toronto are owned by small investors who are likely to experience financial pressure as a result.

The ability of these small investors to weather this economic storm will have a significant impact on the future direction of Toronto condo prices – and a material impact on our economic recovery as a whole.

1. Condominium listings were analysed monthly. If a particular condominium was listed more than once during the same month - a common practice when agents reduce the price - that unit would only be counted once in that month. If the unit had been listed for lease in any of the previous three months but not rented, the new listing in the current month would be excluded from the analysis because that unit would have been already counted as a "new listing" In the previous months.

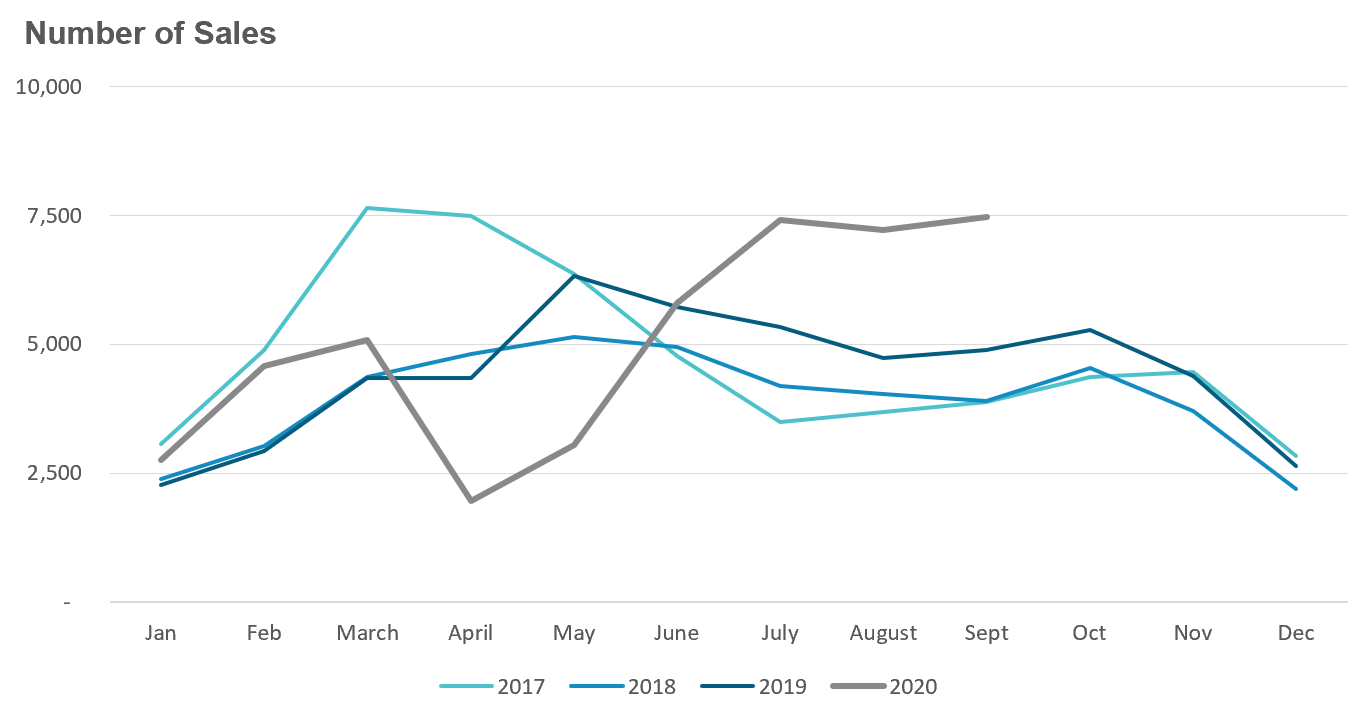

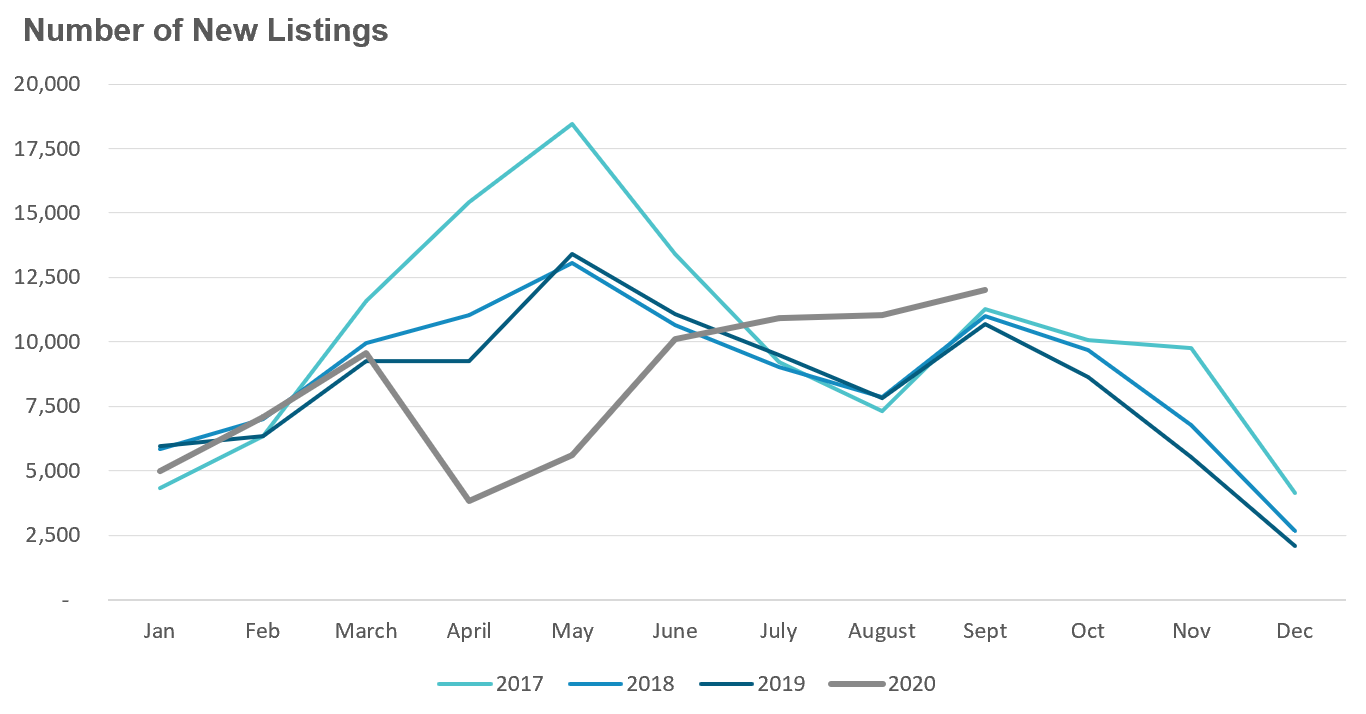

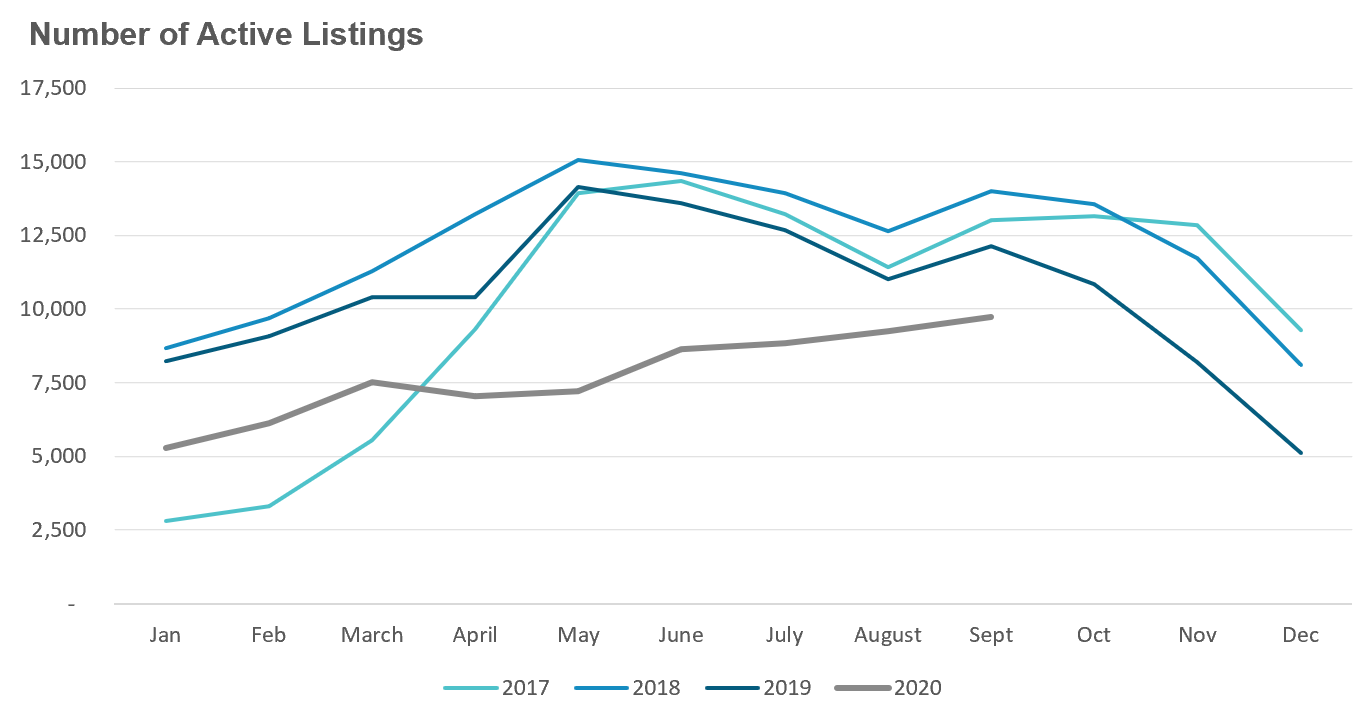

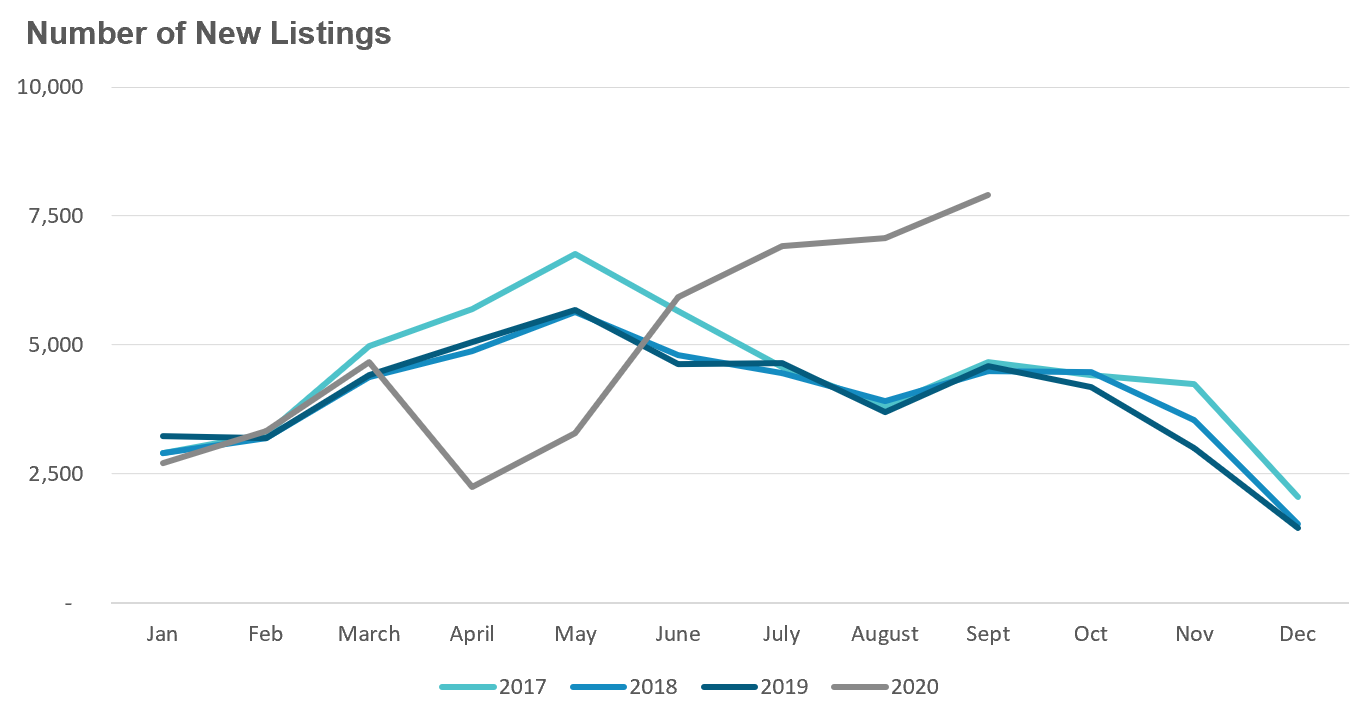

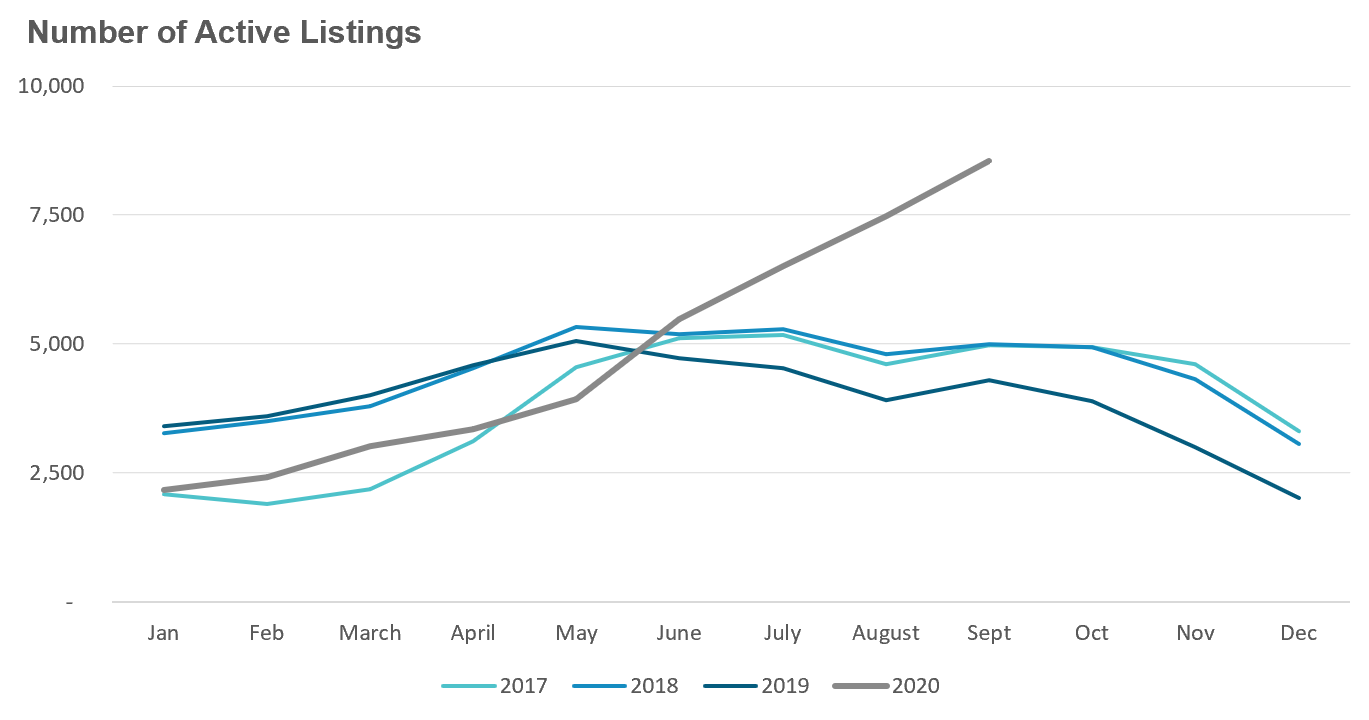

But new listings did not keep up with the strong pace of demand. September saw a 12% increase in new listings over last year while the number of homes available for sale (“active listings”) was down 20% when compared to the same month last year.

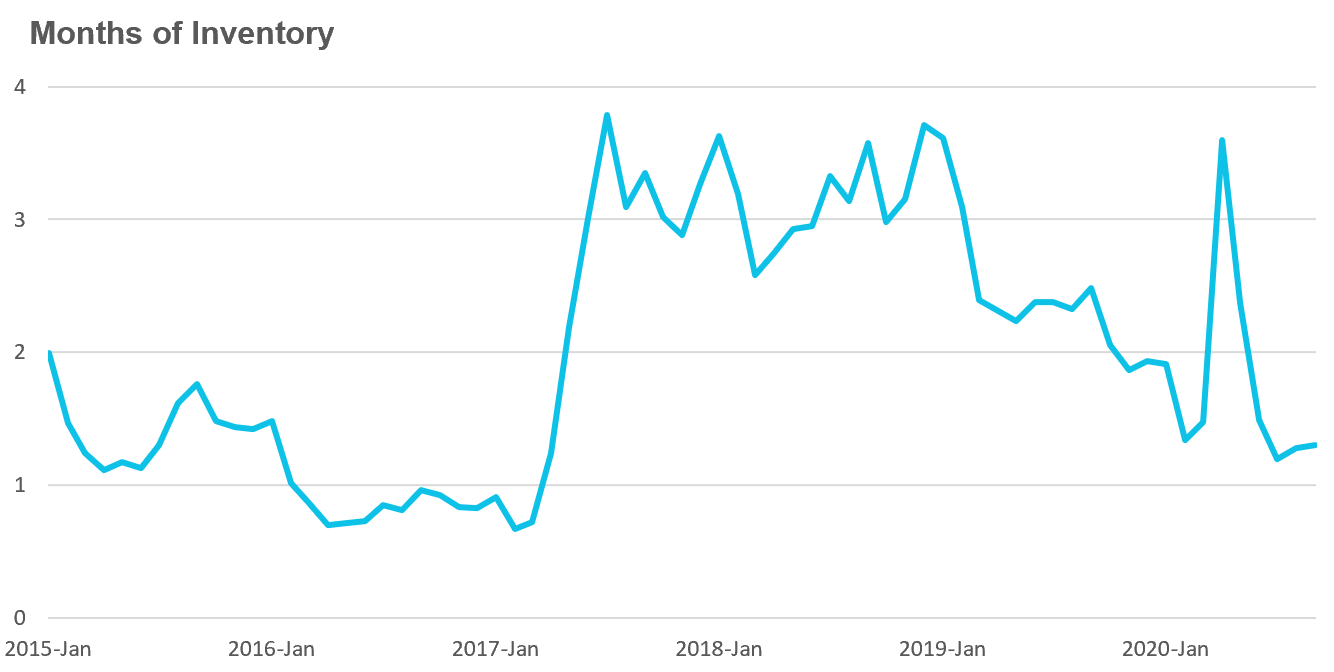

The Months of Inventory (MOI) looks at the number of homes available for sale in a given month divided by the number homes that sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell given the current level of demand?

The higher the MOI, the cooler the market Is. A balanced market (a market where prices are neither rising or falling) is one where MOI is between 4-6 months. The lower the MOI, the more rapidly we would expect prices to rise.

The market remained very competitive in September with an MOI of just 1.3 months.

While the current level of the MOI gives us clues into how competitive the market Is on the ground today, the direction it's moving in also gives us some clues into where the market may be heading. The MOI remaining relatively steady over the past three months suggest that the market is neither heating up or cooling down but remains a very competitive seller's market.

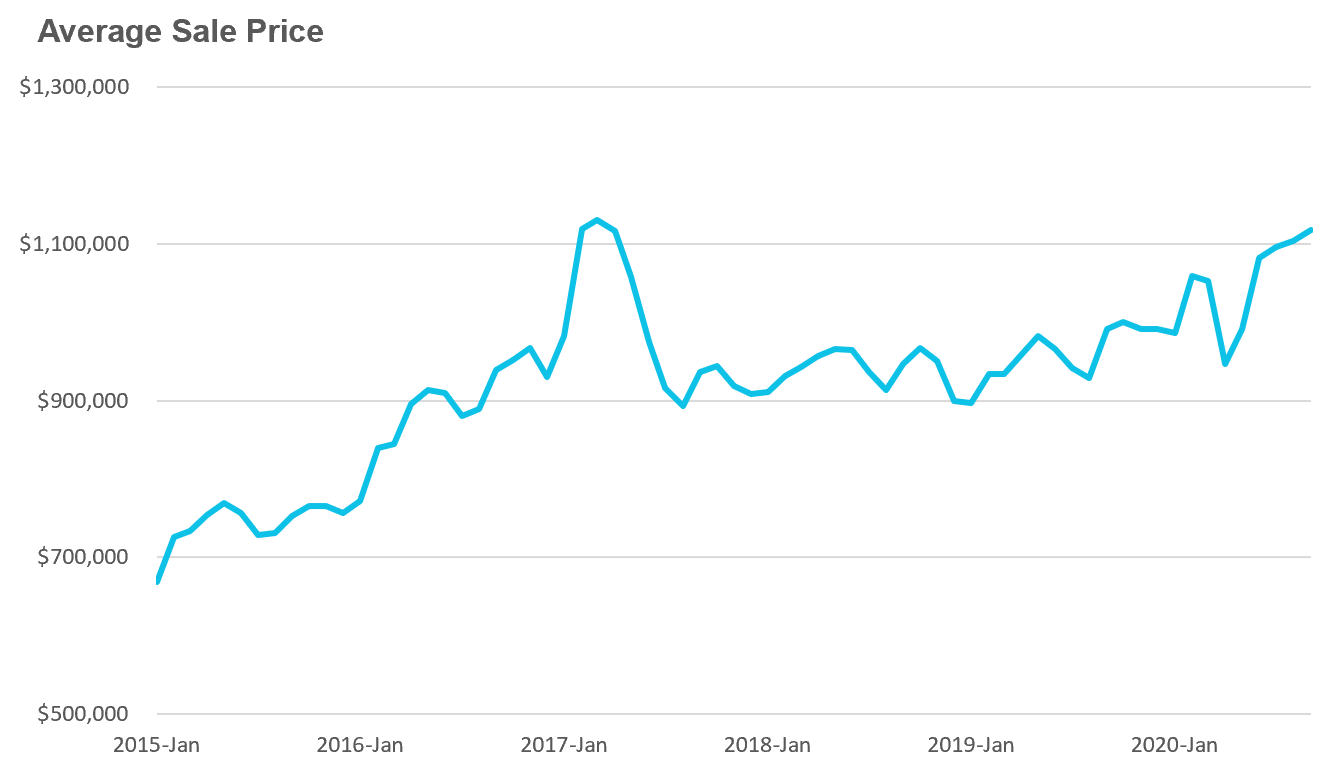

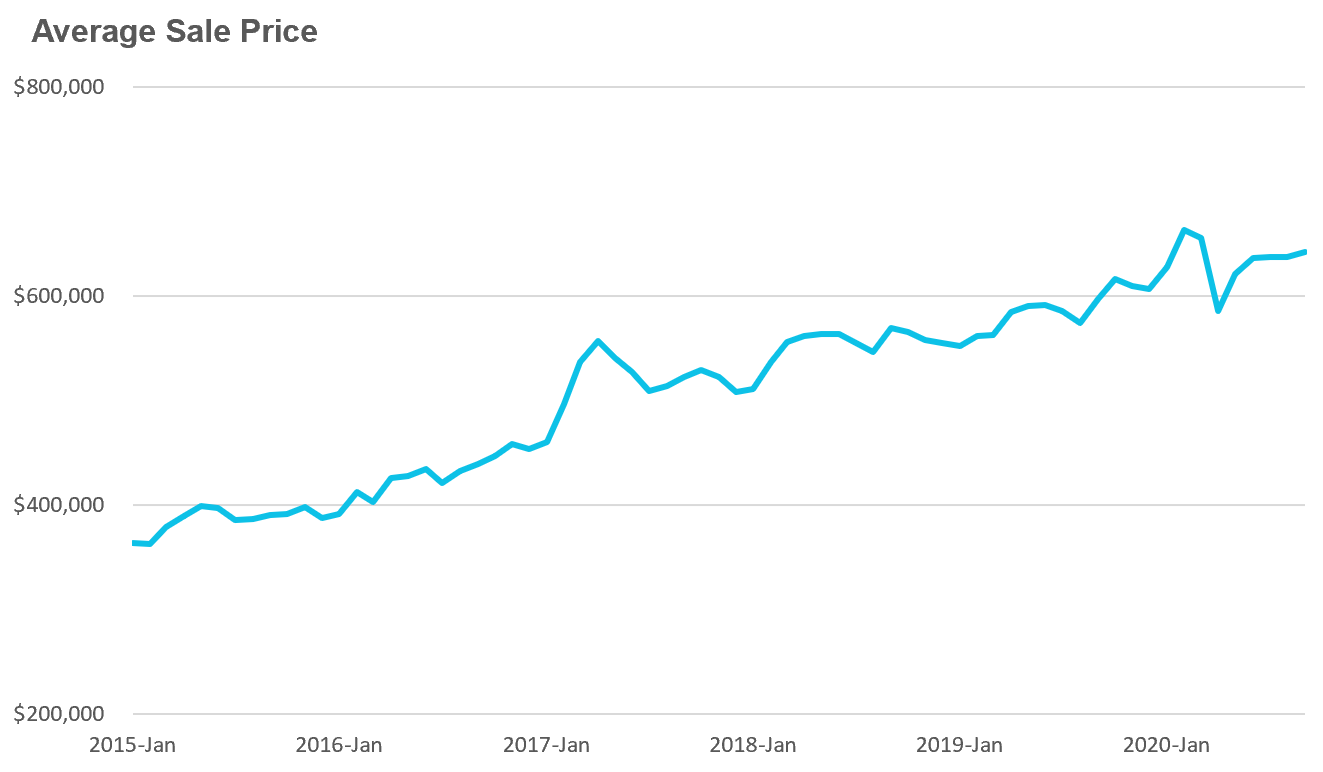

Strong demand coupled with very low inventory levels helped push average house prices up 13% over last year.

New condo listings surged by 73% in September which pushed the active number of condos available for sale In September up by 99% over last year.

This spike in inventory is leading to a cooling down in the condominium market with the MOI increasing from just under 2 months in July to 2.7 in September.

But with inventory still relatively tight, average prices were still up 7% over last year.

It's worth noting that the downtown condo market is currently cooler than the rest of the GTA with an MOI of 5, and while average prices are still rising we are starting to see some early signs of downward pressure on prices as some owners are beginning to price their units below recent sales to get ahead of a cooling market.

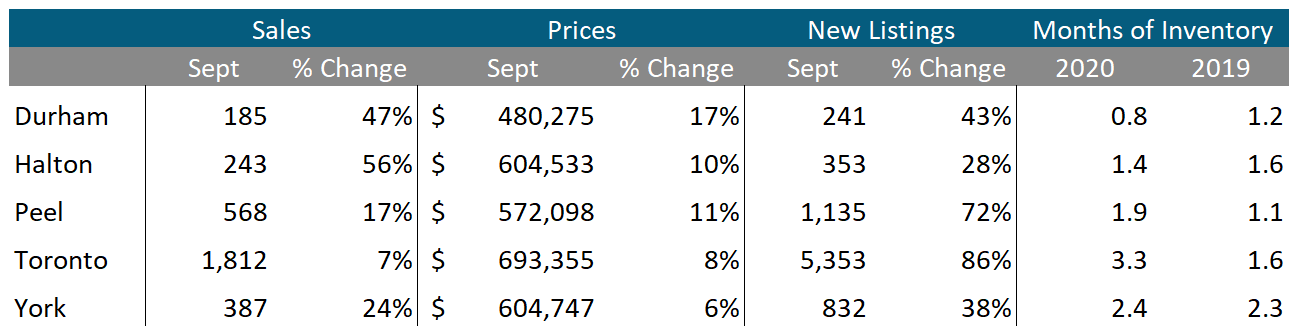

Houses

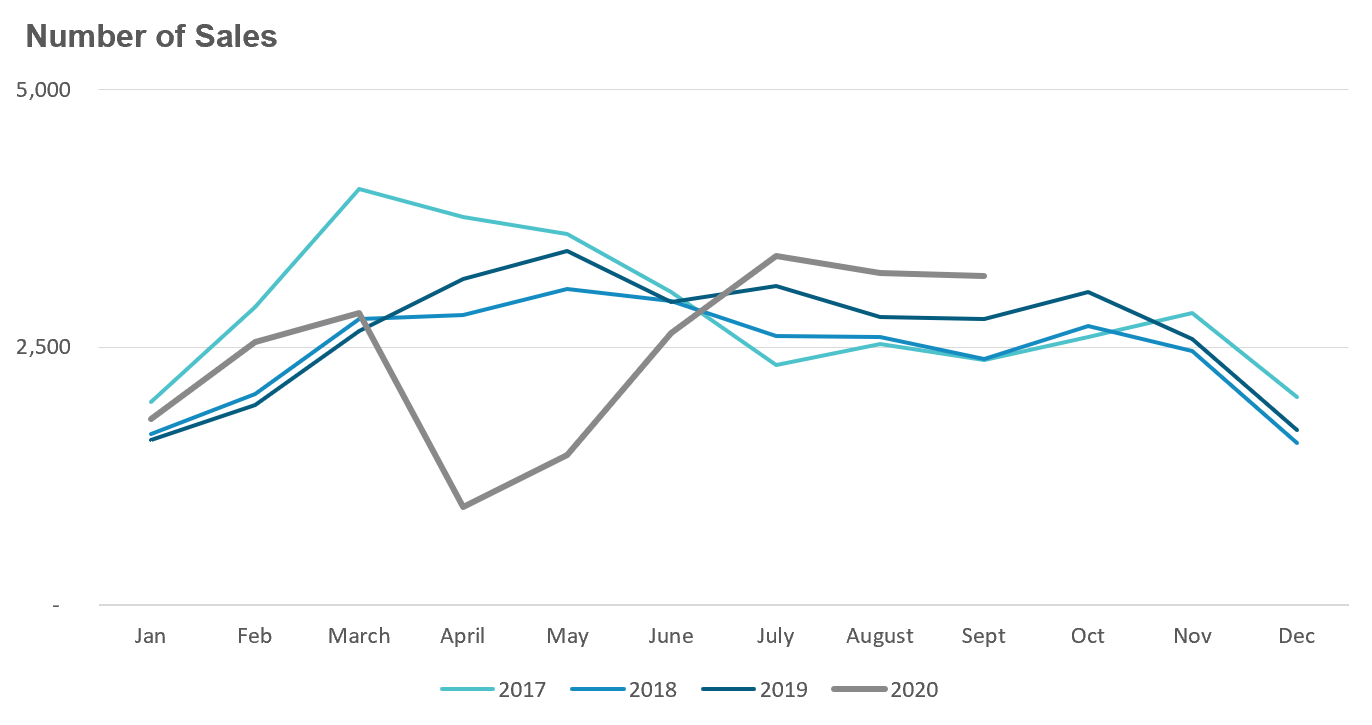

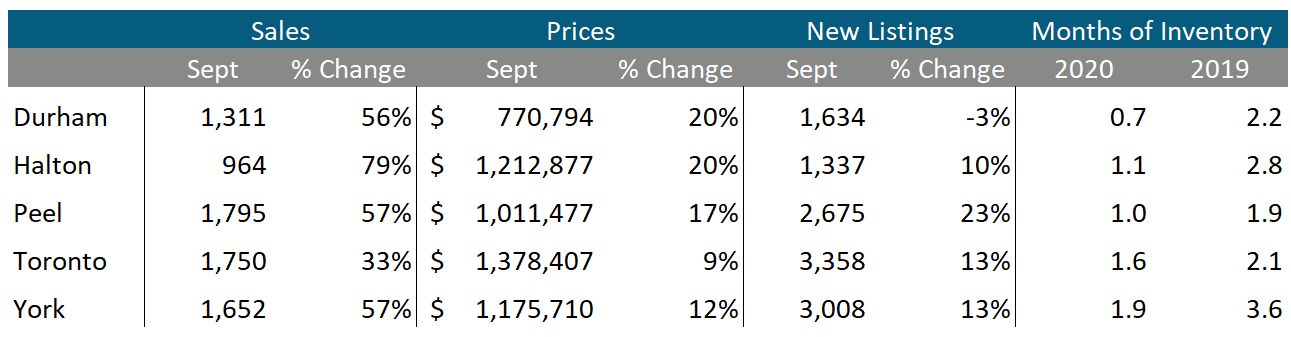

We can see that house sales and prices are up across all five regions in the Toronto Area. New listings were up in four of the five regions with Peel seeing the biggest increase at 23% and Durham seeing a 3% decline in new listings.

The MOI is down significantly in all five regions when compared to last year which tells us that the market is more competitive than it was a year ago.

Condominiums

Condo sales continue to see big increases in Durham and Halton, but both are relatively small markets for condominiums. The City of Toronto saw a modest 7% increase In condo sales, but the MOI for Toronto's condo market Increased from 1.6 months last year to 3.3 months in September indicating a cooling market.