WATCH NOW: Report Author John Pasalis explains latest market numbers

August is typically a quiet month in the housing market.

Many active buyers often hit pause to enjoy the last month of warm weather, and few buyers start their home search in August.

September is typically much busier as it marks the start of the fall home-buying season. The first month of the fall market can often give us clues into how the market will likely progress for the remainder of the calendar year.

The key trend we need to monitor is the relationship between demand (the number of sales) and supply (new listings). If demand outpaces supply, months of inventory will begin to decline, and the market will gradually become more competitive than it has been over the previous few months.

However, if new listings come on the market faster than people buy them, inventory will gradually build, which may put downward pressure on prices.

After nearly 20 years of analyzing and writing about Toronto's housing market, I've learned that predicting where the market will be, even several months from now, is impossible. That said, I'll still offer my outlook for the fall market.

I'm expecting the market for low-rise houses to become a bit more competitive than it has been over the previous few months. This means that sales should outpace new listings, which would put downward pressure on the months of inventory.

We are seeing more buyers who were waiting on the sidelines plan to jump back into the market now to take advantage of a less competitive market where relatively few homes are receiving multiple offers from buyers. While rates are still relatively high, most buyers are looking for short-term mortgages, anticipating rates to be lower a year or two when it's time for them to renew.

However, I'm not expecting a significant surge in demand or a rapid price acceleration. Some buyers are still sitting on the sidelines, waiting for rates to drop further, which would increase the amount they can borrow for a mortgage and, by extension, how much they can spend on a home.

But I'm not as confident we'll see the same trends unfold in the condo market.

Investors play a bigger role in the condo market, and the slight drop in interest rates is still not enough to make buying an investment condo an attractive investment. This means that if the demand for condos increases this fall, the growth will likely be more modest than the increase in demand for low-rise homes.

However, the big factor that will impact the outlook for the condo market is the growth in new listings. Between January and August of this year new listings for condos were up 24% over the previous year. If this trend continues, we could see inventory levels remain elevated and possibly even increase in the months ahead.

LIVE MARKET UPDATE: WATCH REPORT HIGHLIGHTS & Q/A - THURSDAY SEPTEMBER 12th 12PM ET

Join John Pasalis, report author, market analyst and President of Realosophy Realty, in a free monthly webinar as he discusses key highlights from this report, with added timely observations about new emerging issues, and answers your questions. A must see for well-informed Toronto area real estate consumers.

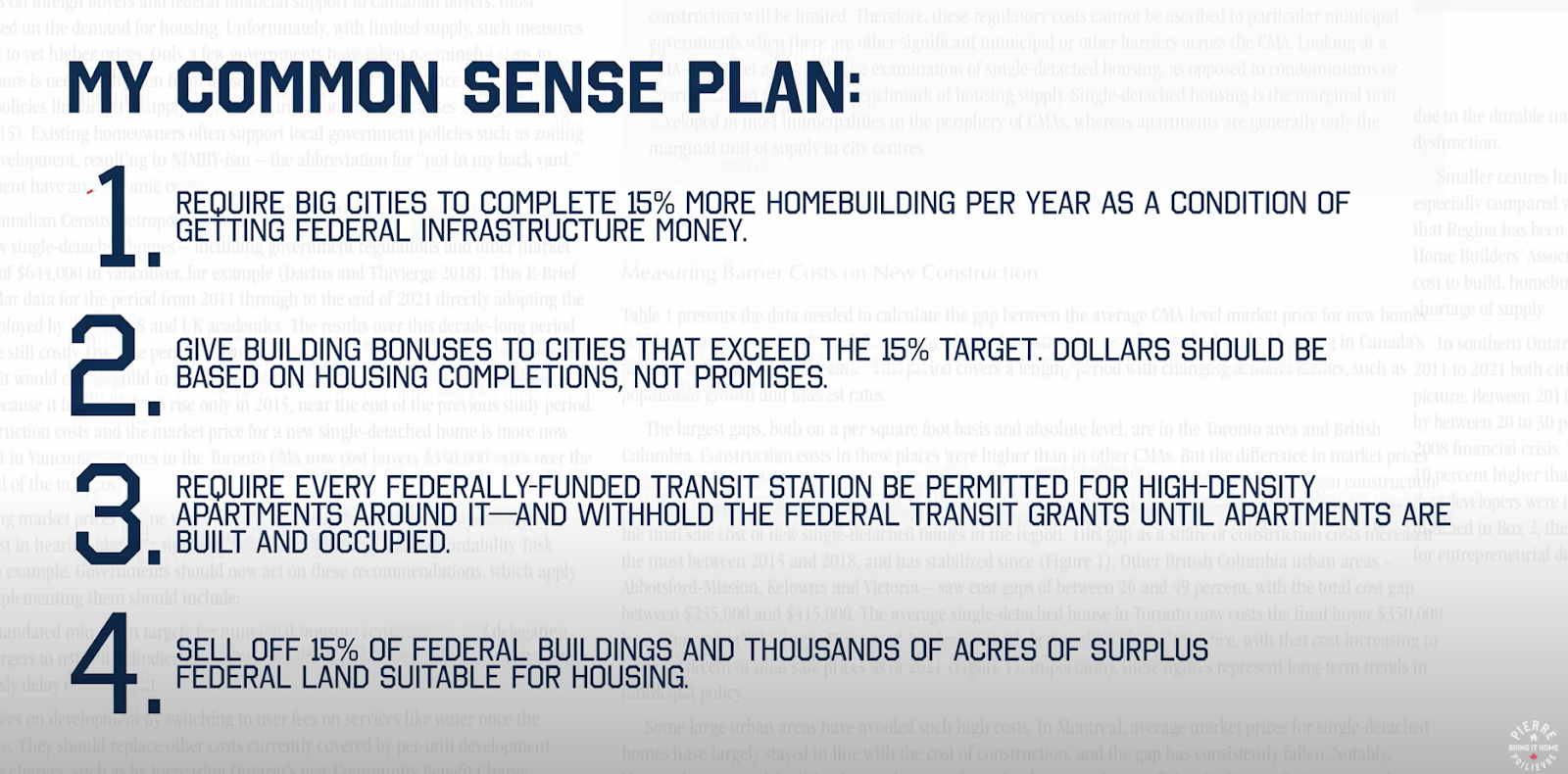

Nine months ago, the federal Conservative Party leader Pierre Poilievre released a YouTube video, titled Housing hell: How we got here and how we get out, in which he unpacked his analysis of Canada’s housing crisis and proposed solutions. Noted for it’s original straight-to-public communication style, the video has over half a million views on YouTube.

While original in format, Poilievre’s housing plan focused on the same old arguments Canadians have heard from politicians and housing economists for years — that Canada’s housing crisis is due exclusively to a lack of supply.

He believed one key way to rapidly increase the supply of housing was to require big cities to complete 15% more homes each year to receive federal infrastructure money, as detailed in his “Common Sense Plan”:

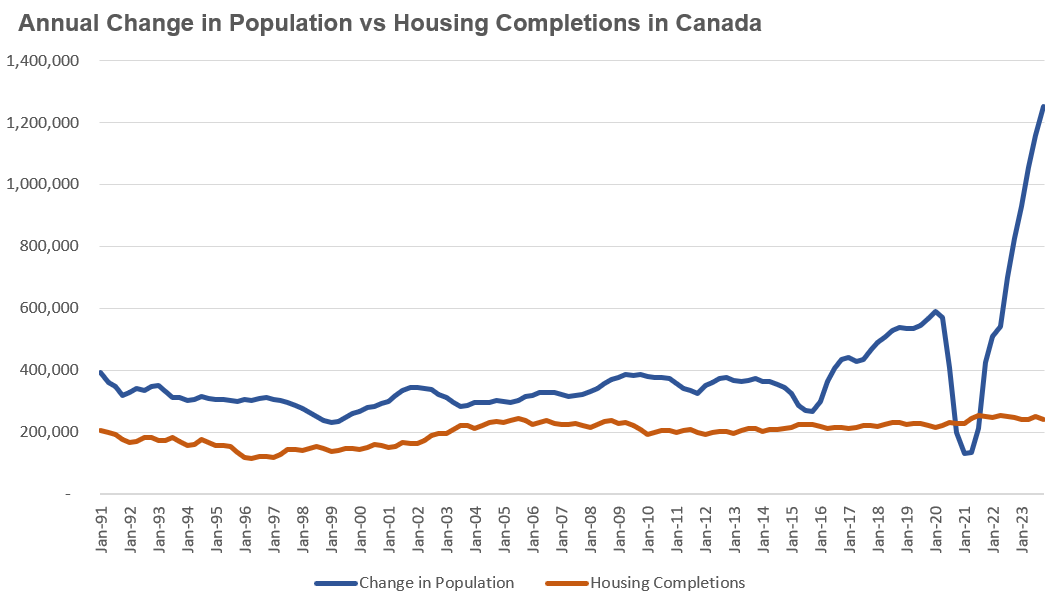

In my December 2023 report, I unpacked the many problems with Poilievre’s theories and plans to fix Canada’s housing crisis, highlighting what I think is the the biggest problem — his failure to mention anything about Canada’s booming population growth driven by immigration:

Polievre, like virtually every other politician at that time, instead continued to emphasize the arguments put forward by YIMBY (“Yes in My Back Yard” or pro-density housing) economists who repeatedly argued that Canada’s booming population isn’t the problem but instead the problem is Canada’s failure to build enough homes for our population, due to government restrictions and municipal and provincial “gatekeepers” who are restricting the supply of new home construction.

According to the YIMBY economists, Canada could triple the number of houses completed over the next ten years if every level of government followed their hundreds of policy recommendations and reforms to stimulate the supply of new housing.

In looking at the above chart, which shows in blue the surging population and in red a straight-line of housing supply, we see that the YIMBY economists have allowed politicians to tell a young generation of potential home buyers who have seen their rents surge and home prices climb out of reach that Canada’s housing crisis has very little to do with the surge in the demand driven by a booming population (blue line) and everything to do with housing supply that has remained relatively flat since the 1990s, and continues to be held down by municipal and provincial “gatekeepers” today (red line).

As I’ve been saying on Move Smartly and other publications for years, the ”it’s just the supply” ideas put forward by YIMBY economists were as misguided five years ago as they are today.

Fortunately, we are starting to see politicians abandon the idea that our housing crisis can be solved by focusing solely on supply-side policies while ignoring Canada’s recent population boom.

The Liberals, who under PM Justin Trudeau have been responsible for Canada’s population surge through a spike in immigration, particularly through the issuing of temporary worker and student visas, were the first party to acknowledge that these increased demand for housing is just as important as supply constraints. In their 2024 Federal Budget, their section on housing policies included a discussion around better managing the demand for housing through a more sustainable immigration strategy. The Liberals have imposed cutbacks on the number of student visas being issued and have announced their intention to do the same with temporary workers.

Four months after the federal government’s remarkable shift on housing policy, Polievre now also says that the demand for housing matters and that his housing policies will also include a careful review of establishing sustainable immigration levels.

While it’s encouraging to see that Canada’s politicians are now focusing on this spike in demand for housing as key driver of our housing crisis,, I am alarmed that the analysis and expertise they have access too did not allow them to see this problem before so much damage has been done to the aspirations of all Canadians, newcomers and existing alike as housing costs have spiralled out of control.

An alarming assessment of their miscalculation is that they genuinely believe the misguided ideas put forward by housing academics who focussed exclusively on the supply side of the problem; a more cynical, and perhaps even more alarming, assessment is that they lacked the courage to say what some including myself have long said — that mismanaged demand through surging immigration was a huge problem.

After all, it was merely hurtful to me for others to suggest that my assessment came from an anti-immigrant and xenophobic attitude, but for politicians perhaps the risk seems even greater — in their desire to gain votes, they’ve decided that correctly assessing problems is simply not a winning strategy politically, that is, until the voters themselves demand change long after the damage has already been done.

Monthly Statistics

House sales (low-rise freehold detached, semi-detached, townhouse, etc.) in the Greater Toronto Area (GTA) in August 2024 were down 3% compared to the same month last year.

New house listings in August were unchanged compared to last year.

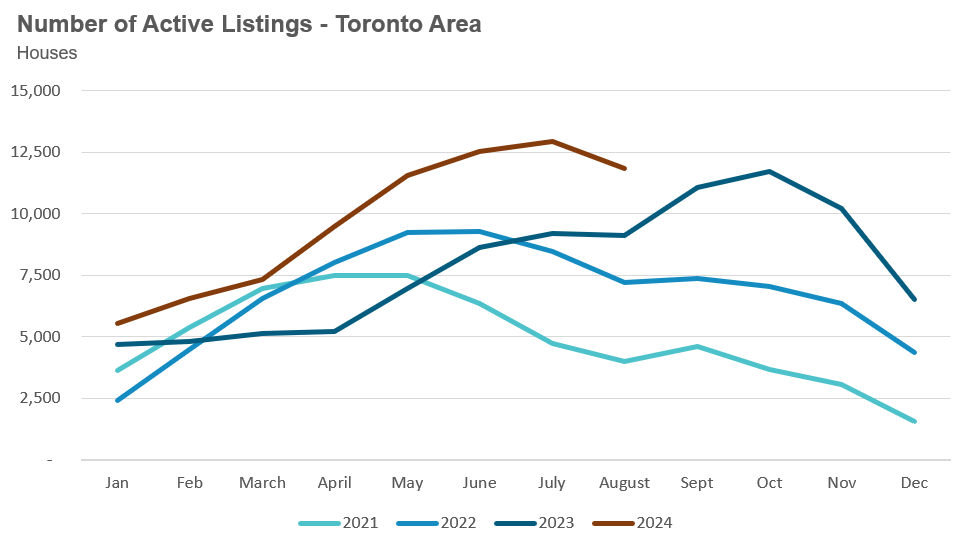

The number of houses available for sale (“active listings”) was up 30% in August compared to the same month last year.

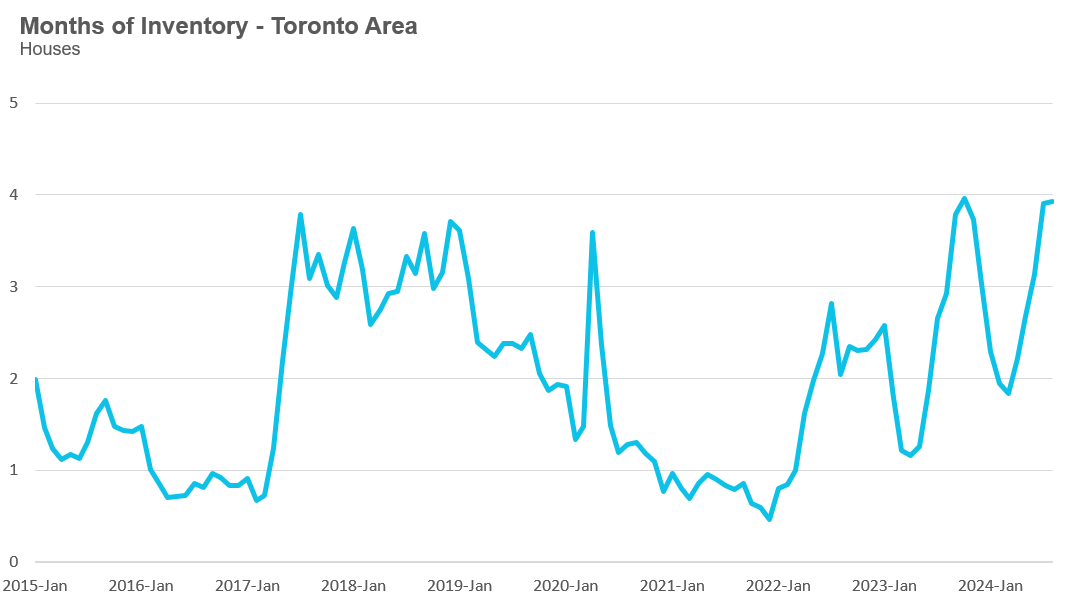

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number of homes sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell, given the current level of demand? The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

While the current level of MOI gives us clues into how competitive the market is on-the-ground today, the direction it is moving in also gives us some clues into where the market will be heading.

The MOI for houses was unchanged at 3.9 for August.

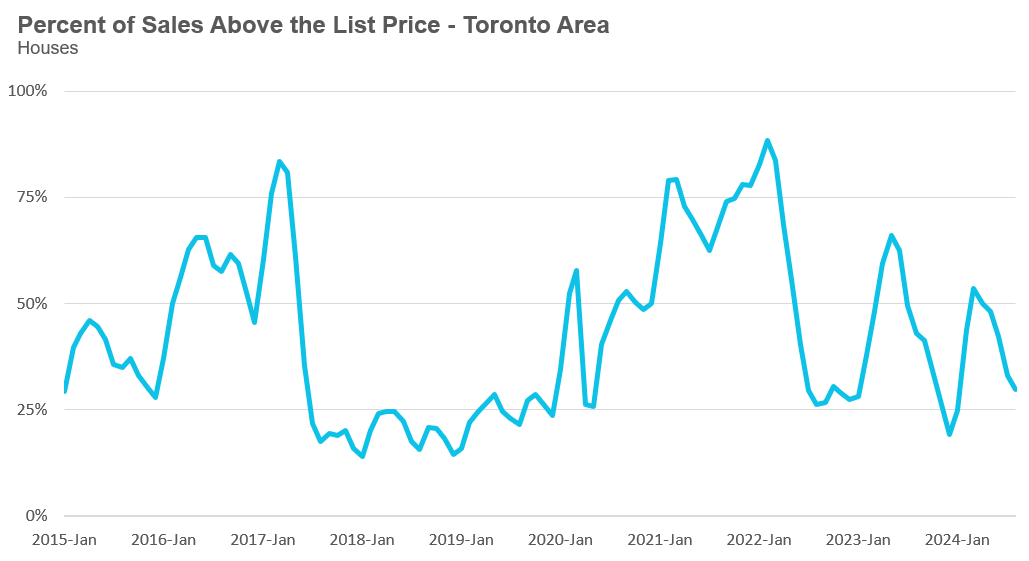

The share of houses selling for more than the owner’s list price decreased to 30% in August.

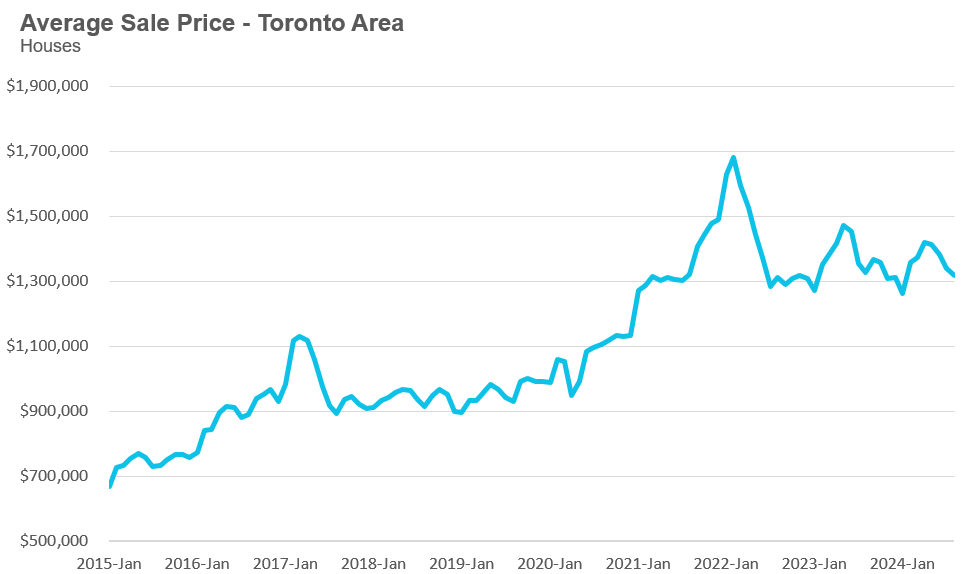

The average price for a house in August 2024 was $1,318,684, down 1% from the same month last year.

The median house price in August was $1,125,000, down 3% over last year.

The median is calculated by ordering all the sale prices in a given month and then selecting the price at the midpoint of that list such that half of all home sales are above that price and half are below that price. Economists often prefer the median price over the average because it is less sensitive to big increases in the sale of high-end or low-end homes in a given month, which can skew the average price.

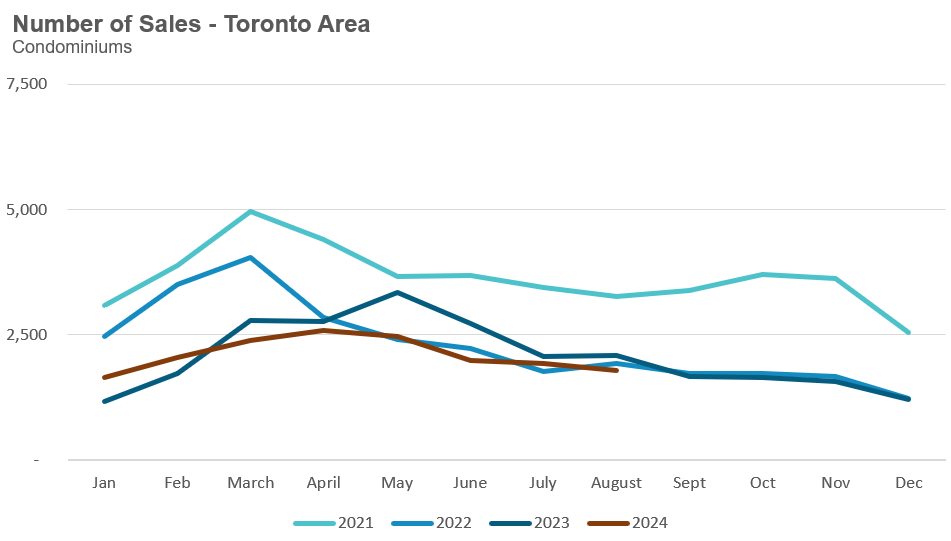

Condo (condominiums, including condo apartments, condo townhouses, etc.) sales in the Toronto area in August 2024 were down 15% compared to the same month last year.

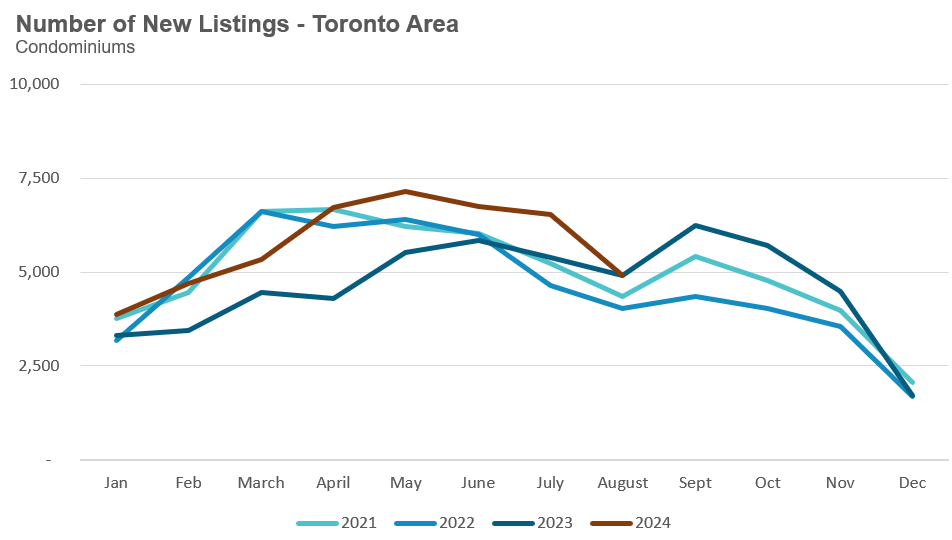

New condo listings were unchanged in August over last year.

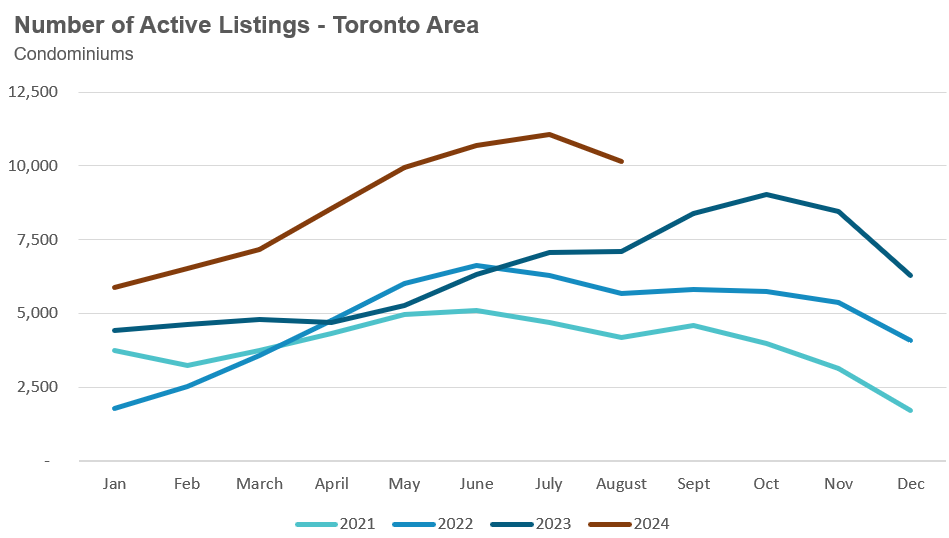

The number of condos available for sale at the end of the month, or active listings, was up 43% over last year.

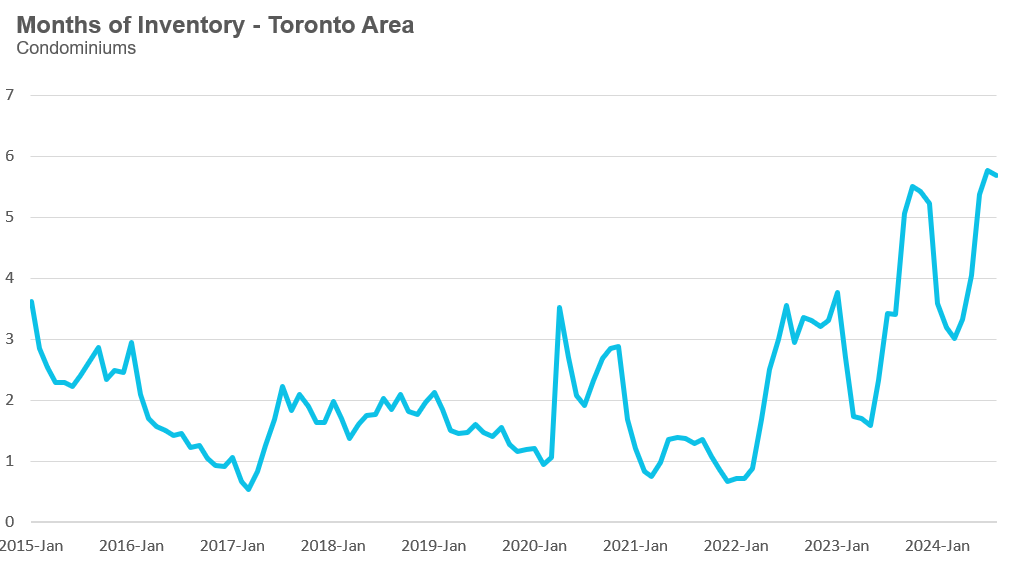

Condo months of inventory decreased slightly to 5.7 MOI in August.

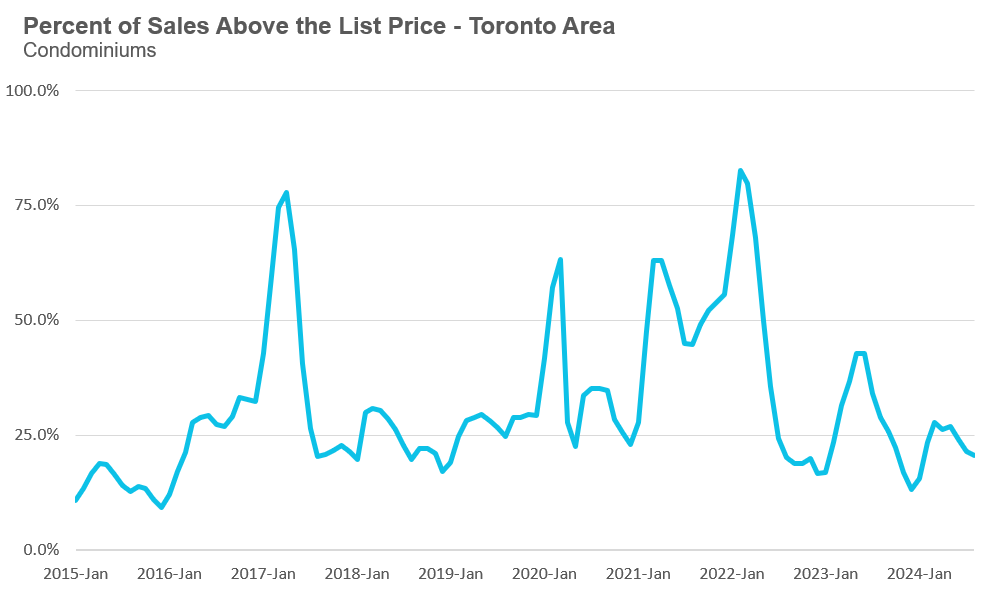

The share of condos selling for over the asking price was unchanged at 21% in August.

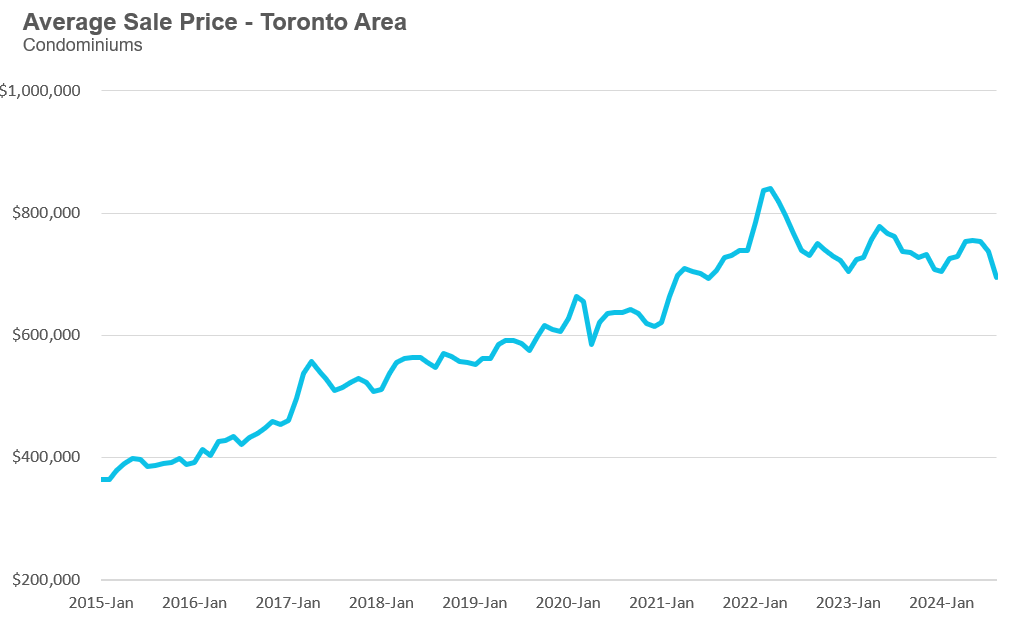

The average price of a condo in August was $693,845, down 6% from last year. The median price was $633,751, down 6% from last year.

Houses

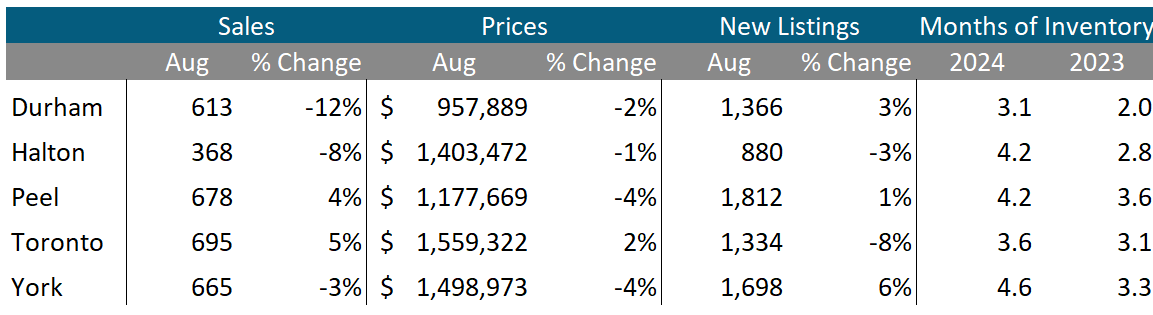

Sales were up by 5% in Toronto and 4% in Peel, but down in Durham, Halton and York. Average prices were up by 2% in Toronto but down modestly across all four suburban regions. New listings were up by 6% in Peel and down 8% in Toronto. Months of inventory was up across all regions.

Condos

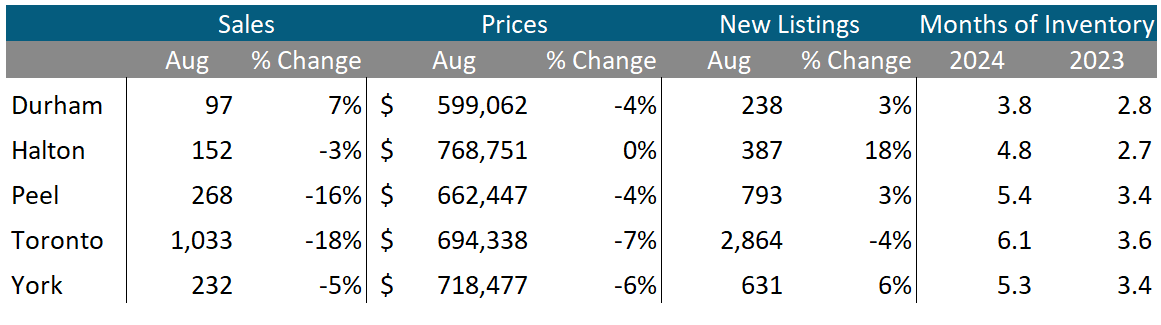

Condo sales were up in Durham but down in the other GTA regions with Toronto seeing the biggest decline in sales. Average prices were flat in Halton and down across the rest of the GTA. New listings and MOI were well above last year’s level for all regions. The City of Toronto has the highest MOI across all five regions.

See Market Performance by Neighbourhood Map, All Toronto and the GTA

Greater Toronto Area Market Trends