LIVE MARKET UPDATE: WATCH REPORT HIGHLIGHTS & Q/A - THURSDAY JULY 11th 12PM ET

Join John Pasalis, report author, market analyst and President of Realosophy Realty, in a free monthly webinar as he discusses key highlights from this report, with added timely observations about new emerging issues, and answers your questions. A must see for well-informed Toronto area real estate consumers.

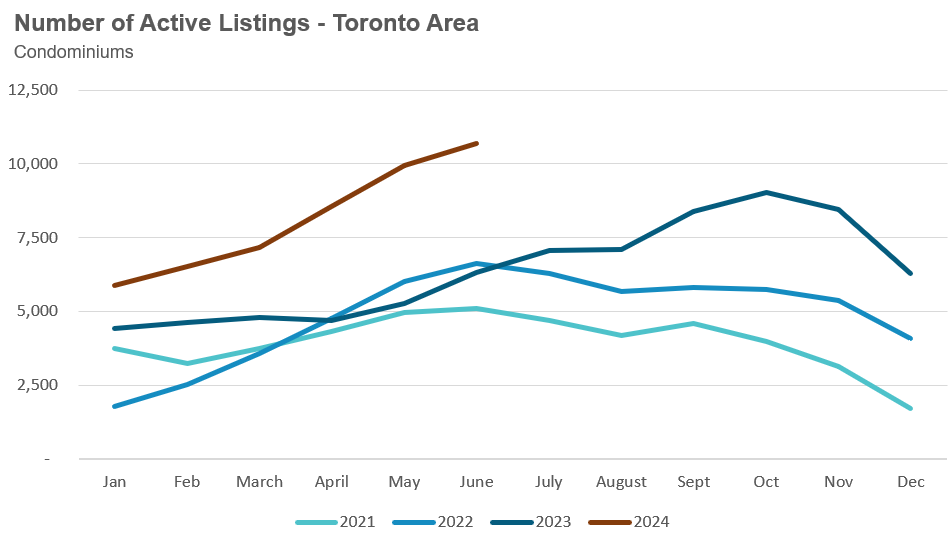

The number of condos available for sale in the Toronto area has reached another new record high — so will this surge ease our housing shortage?

The Toronto area condo market continues to cool, with the number of condos available for sale reaching a new record high, surpassing last month’s record — so will this surge ease the housing shortage in the Toronto area?

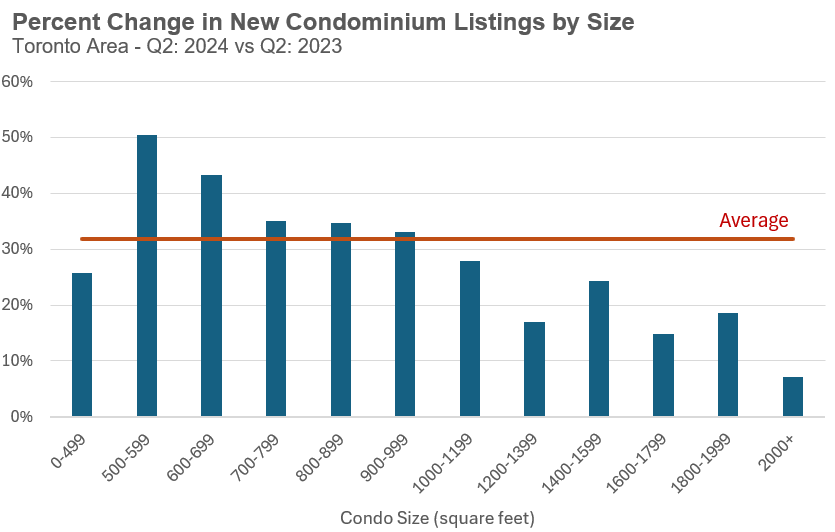

One way to help answer this question is to look at the year-over-year change in the number of new listings during the second-quarter by condo size. One common argument circulating in the media is that Toronto is seeing a spike in the number of small condos listed for sale, and the data largely supports that narrative.

Units in the 500-599 square foot range saw the sharpest increase in new listings, up 50% over last year. The growth in new listings generally declines as the unit size increases, indicating that proportionally fewer owners of large units are listing their condos for sale.

The one exception to the above trend is very small units under 500 sq ft, which saw a smaller 26% increase in new listings over the last year, below the overall average increase of 32%. I suspect that more of these smaller units didn’t hit the market because many of those units are in newer buildings that were likely instead rented out by their owners at completion.

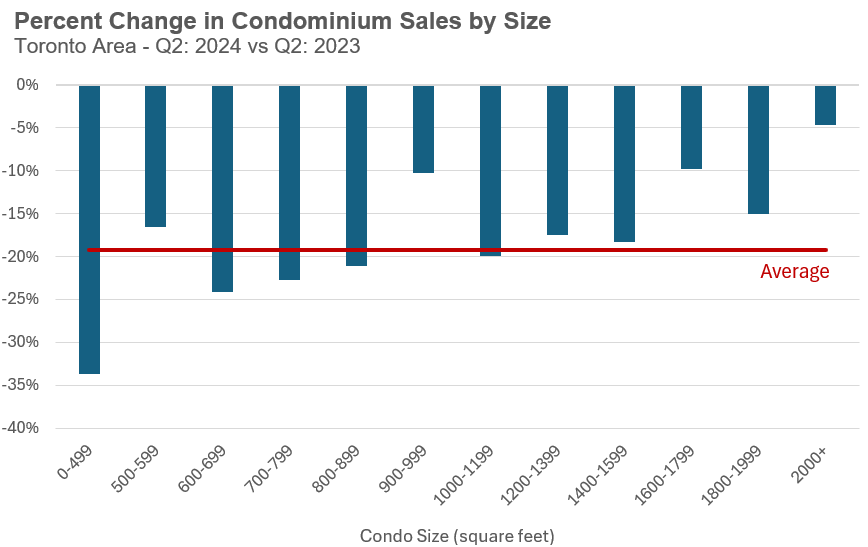

However, when we consider the demand for condo units by measuring the change in the number of sales during the second quarter, we see that units under 500 sq ft in size saw the biggest decline in sales. This is largely driven by the fact that the most common buyer of these units are investors and demand from investors has largely dried up because of high interest rates.

While the sales data is more volatile, the overall trend is that larger units are seeing a more moderate decline in sales compared to smaller units.

Despite the surge in the number of condos listed for sale, average prices have been relatively stable. However, the future is uncertain. If the number of active listings continues to accelerate, we may see some downward pressure on prices in the months ahead. Conversely, if inventory levels decline during the fall market, prices may continue to remain stable. This uncertainty underscores the potential risks in the market.

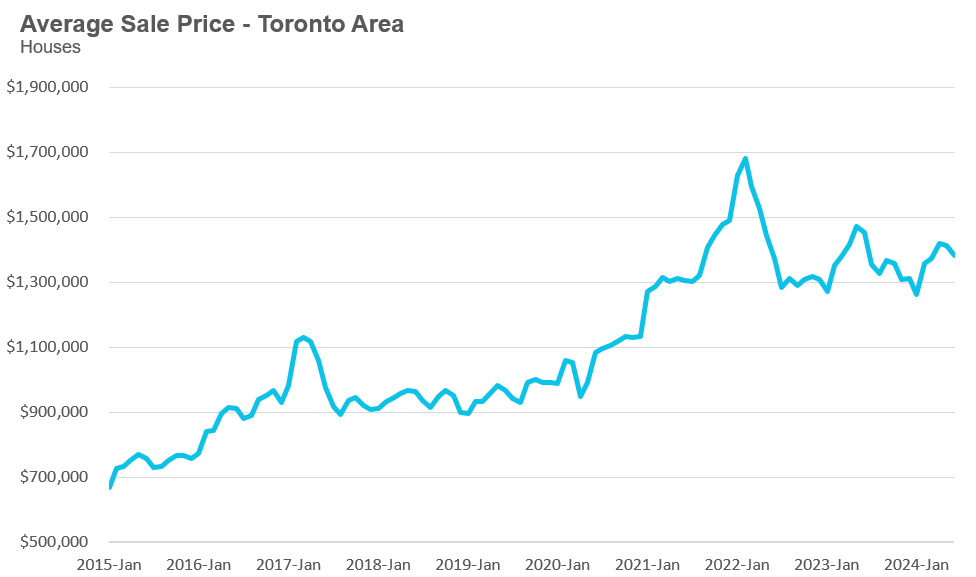

The average price for a house in the Toronto area was $1,382,118 in June, down 5% over the same month last year. Last month's median house price was $1,200,000, down 6% over last year.

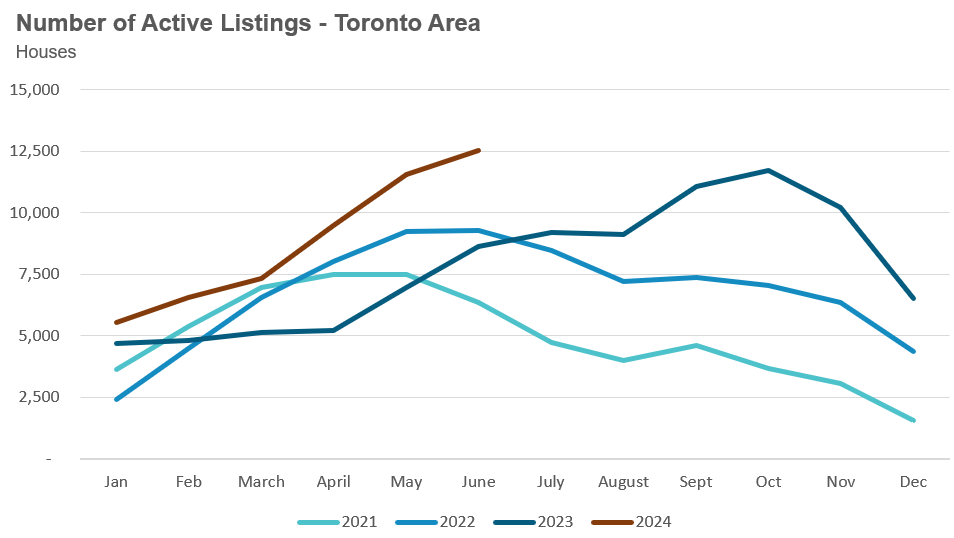

House sales in June were down 13% over last year, while new house listings were up 8%. The number of houses available for sale at the end of the month, or active listings, was up 45% over last year.

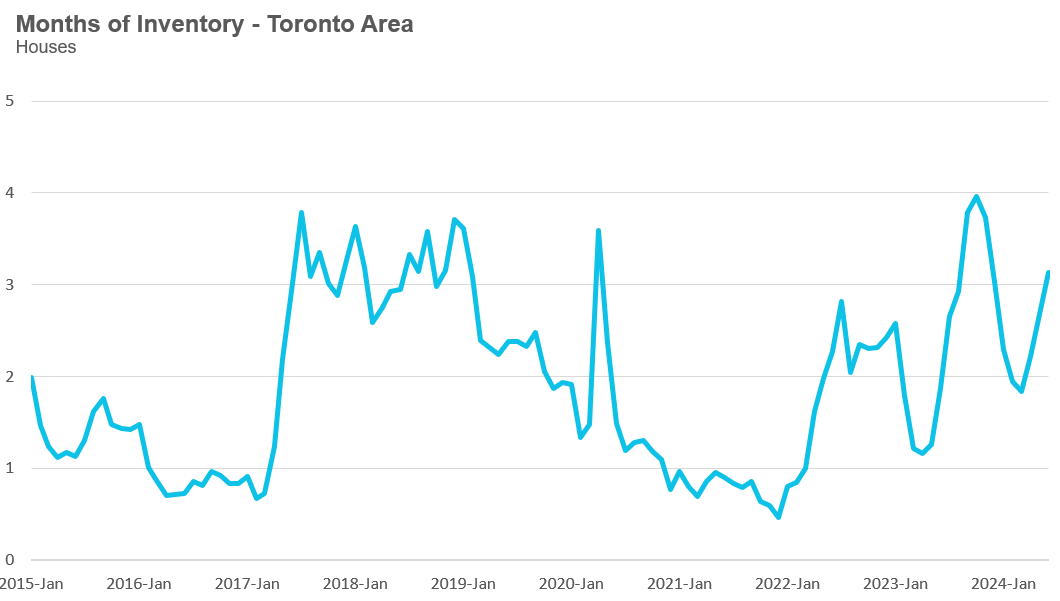

The current balance between supply and demand is reflected in the MOI, which is a measure of inventory relative to the number of sales each month. In June, the MOI for houses increased slightly to 3.1.

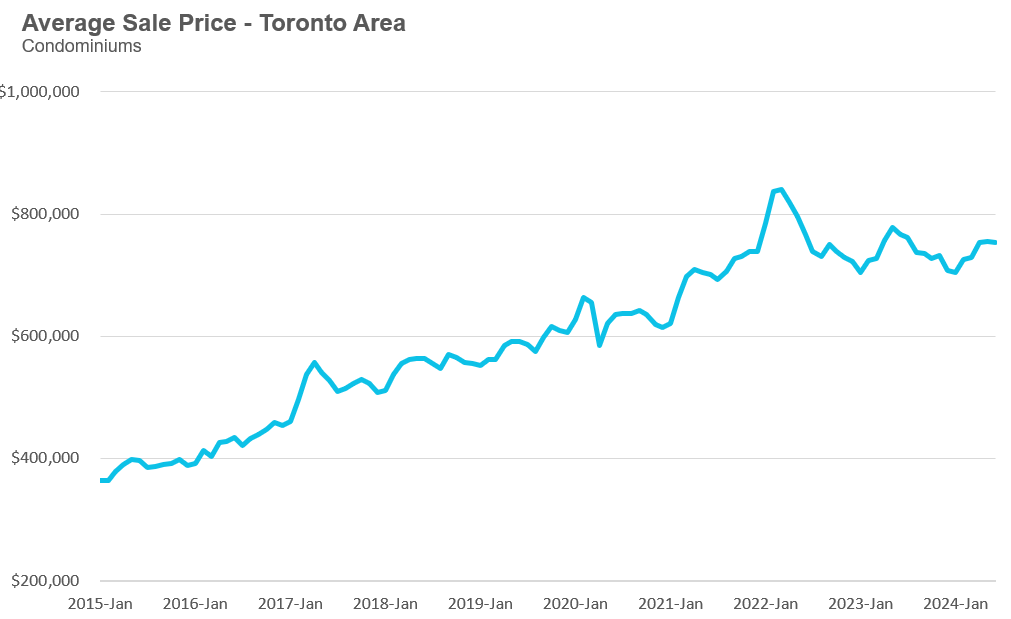

The average price for a condo in the Toronto Area was $753,111 in June, down 2% over last year. The median price for a condo in June was $670,000, down 3% over last year.

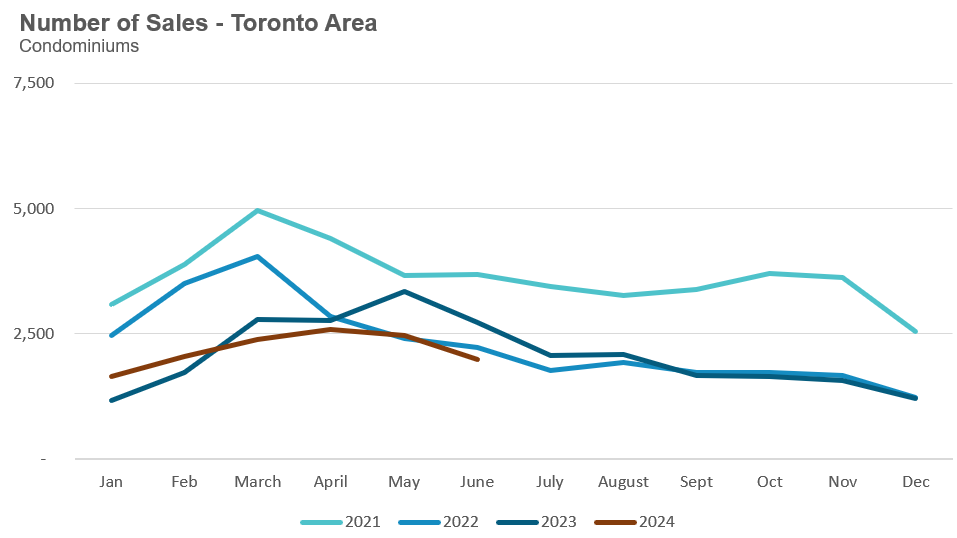

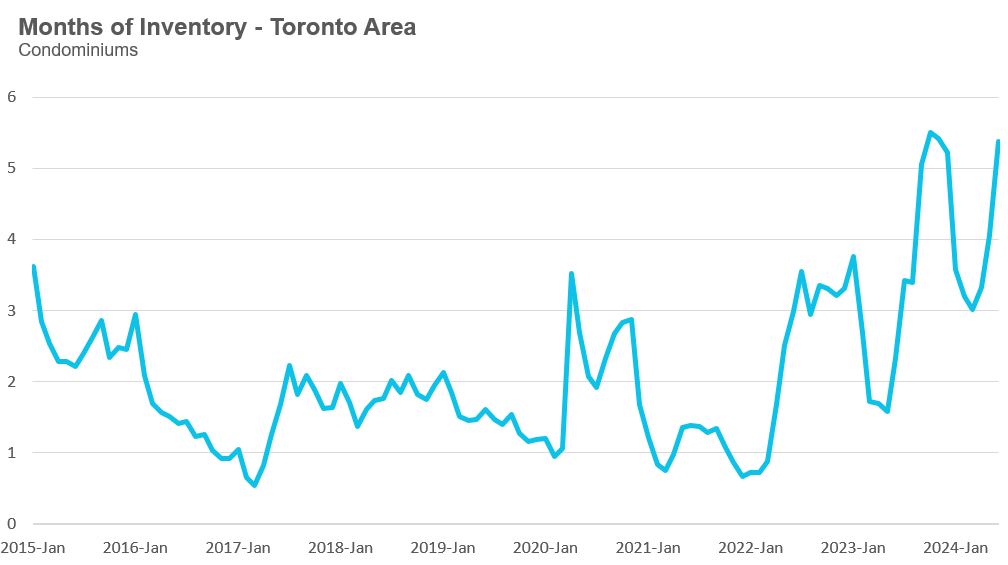

Condo sales in June were down 27% over last year, and new condo listings were up 16% over last year. The number of active condo listings was up 70% over last year and reached a new record of 10,688 for any month. The MOI increased to 5.3.

Browse detailed monthly statistics for June 2024 for the entire Toronto area market, including house, condo and regional breakdowns below.

WATCH THIS STORY NOW: Is Canada Propping up Condo Investors to Prevent Prices From Falling?

While most media headlines regarding Toronto’s condo market have focused on the record number of units listed for sale, there is a bigger and more troubling risk that few have considered. Many of the newly completed condominiums in Toronto are not worth what investors paid, which raises an important question.

Are Canadian policymakers and financial institutions artificially supporting investors to prevent condo prices from collapsing? I believe they are, and I think this problem will only get worse in the years ahead.

Warnings in 2020

In early 2020, I published an article on Move Smartly titled Why Investing in Pre-Construction Condos Could Cost You Money.

At that time, the average price for pre-construction condos in downtown Toronto was around $1,500 per square foot, whereas resale condos sold for about $1,000 per square foot. This stark difference in pricing raised concerns about the sustainability of such premiums, particularly if the resale market did not continue to appreciate at the same pace. Investors banking on future price increases could find themselves in a difficult position, holding properties worth less than their purchase price.

Looking at the condominiums that will be completed in 2024, it’s clear that my concerns about pre-construction condos not being worth what investors paid are playing out just as I suggested they might.

55 Mercer Street: A Case Study

A telling example of the challenges of the pre-construction condo market is the development at 55 Mercer Street, a downtown Toronto condominium completed in early 2024. I analyzed twenty recently rented units to better understand the price investors paid and the net rental income earned on these units.

Investors of these units paid an average purchase price of $855,000, equating to about $1,539 per square foot and an average unit size of 555 square feet. In contrast, the average resale condo price in the same neighbourhood is $870,000, equating to $1,029 per square foot and an average size of 845 square feet. This is not an apples-to-apples comparison since 55 Mercer is a newer building and will be superior to many of the older existing resale condominium units.

The monthly cash flow for these units can also be easily estimated since we know the price each unit was rented for. We can also easily estimate the monthly maintenance fees and property taxes based on the information from the comparable existing units for sale. Assuming the average buyer had a 25% down payment, the rental income from these units fell significantly short of covering costs, resulting in a negative cash flow of around $1,700 per month for investors.

When writing this article, 27 condominium units had been listed for sale at 55 Mercer, but only one had been sold. The unit sold for roughly 19% less than its original purchase price. This decline is likely representative of the approximate market value for units in the building. On a per-square-foot basis, the condos are worth more than the average condo in the neighbourhood but not worth what the investors paid.

The primary reason that newly completed condos are not worth what investors paid is that resale prices have not appreciated since 2020. The chart below is from the condo website Condos.ca, showing the average price per square foot in the King West neighbourhood in downtown Toronto. Prices increased between 2020 and 2022, when interest rates fell to a record low, but have since declined to their 2020 level.

Are Banks Bending the Rules?

Normally, when a property declines in value between the time the buyer purchases it and the closing date, banks will only underwrite the mortgage based on what the property is worth (the appraised value), not what the investor paid for it.

For example, if an investor paid $800,000 for a unit that declined in value by 20%, banks will only provide a mortgage of up to 80% of the appraised value of the property - which is $640,000. A buyer who planned to make a 20% down payment ($160K) based on the original purchase price would have found that their original down payment covers the decline in the property’s value. They would have to contribute an additional $128,000, which serves as the 20% down payment required based on the lower appraised value.

When hundreds of condo buyers in a project scheduled to be completed all have units worth less than what they paid for them, we would normally hear some rumblings among industry insiders about distress. We would hear stories about investors who didn’t have the additional capital required to get their mortgage or investors who didn’t qualify for a mortgage at today’s much higher interest rates. But we haven’t heard any stories of distress.

I have heard from many reputable people in the real estate and mortgage industry that financial institutions are bending banking rules to help these investors get a mortgage. Banks use "blanket appraisals," which assume that newly completed condos are worth their original purchase price despite lower market values.

This means that the condo investor does not need to come up with additional funds on closing when their unit is worth less than what they paid. However, it also means that banks may be issuing mortgages equal to 100% of the current market value of these properties in some cases.

This practice introduces significant long-term risks. By not adjusting appraisals to reflect current market conditions, banks may be inflating the true value of their loan portfolios and misrepresenting the loan-to-value ratio on this debt.

Furthermore, our government's decision to allow banks to bend the rules to accommodate real estate investors raises questions about its promise to restore generational fairness in Canada. When our government changes mortgage rules for one segment of the population, older and wealthier real estate investors, it does so at the younger generation's expense.

Young potential home buyers have a right to be furious about these trends. The real estate playing field was already stacked against them, and by protecting investors from the consequences of their bad investment decisions, our government has transferred the costs of these mistakes to younger buyers in the form of condo prices that are higher than they otherwise would have been.

The Troubled Road Ahead

Canadian policymakers and financial institutions appear to be bending mortgage rules to help investors because they have a vested interest. Many of Canada’s big banks are the primary lenders financing the construction of new condominiums, and for banks to get those loans paid back by builders, the investors who bought units in the project need to take ownership of their units - which means they need a mortgage.

If too many investors find that they can’t close on their units, this could jeopardize the entire project and, in a worst-case scenario, could lead to the condominium failing to register and possibly the builder defaulting on their debt. While this rarely happens in Canada, many condominium projects in the United States failed during the financial crisis when investors refused to close on their units because property values plummeted well below the original purchase price.

Policymakers find themselves in a tough spot.

Sweeping these problems under the mat by offering investors blanket appraisals and hoping nobody notices has served banks well so far, but this approach has its downsides and limits.

When considering the downsides of this approach, Canada’s policymakers are sending a clear signal to real estate investors that governments will do everything in their power to mitigate their bad investment decisions - particularly when this also protects Canada's big banks.

Several years ago, Peter Routledge, the head of Canada’s banking regulator OSFI, said this about the impact real estate investors were having on Canada’s housing market.

“Secondary buyers -- the investors -- they're making investments to generate a return. That's a free-market economy, more power to them”

Peter Routledge, BNN Bloomberg 2021

The challenge with Routledge’s free-market economy is that by bending Canada’s mortgage rules to help real estate investors qualify for a mortgage, policymakers are ensuring that real estate investing in Canada does not operate as a free-market economy.

Investors get all the upside benefits when their investments perform well, but they do not bear the full cost when they make a bad investment - because governments are there to help them avoid any loss. When investors don’t lose money when making a poor investment decision, policymakers are creating a government-supported moral hazard problem that will only encourage more investors to use and view housing in Canada as a speculative asset that policymakers have a direct interest in ensuring is a lucrative investment with minimal downside risk.

Canada’s approach will also have its limits, which will be tested in the years ahead.

Over 90,000 condominium units are still under construction in the Toronto area, and the future outlook for those units looks even more challenging.

Of the condominiums completed this year, the market value of those units is, on average, 10% below what investors originally paid for them.

In the years ahead, the difference between what newly completed condominiums were purchased for and what they will be worth on the resale market will only get worse (assuming resale prices don't increase).

What will happen when banks accept blanket appraisals for newly completed condos purchased for $1,800 per square foot, but the market value for those units is only $1,300 per square foot?

We’ll end up with a situation in which the mortgages on these units exceed their market value.

Our government is going to extraordinary lengths to keep condo prices from falling, and the market will test those limits over the next 12-24 months.

Where Do We Go From Here?

Where we go from here depends heavily on our government’s policies and approach to handling the problematic conditions ahead.

Policymakers can continue doing what they have been doing, encouraging banks to break Canada’s banking regulations to support the bad investment decisions of this small sub-class of real estate investors. This would avoid a broader systemic crisis of condo projects failing due to too many buyers defaulting on their purchases.

If newly completed condo projects begin to fail, the negative consequences and economic side effects would be significant.

While policymakers have some control over managing the overpriced new condominiums that will be completed in the years ahead, they have far less control over what happens in the resale market, which currently has a record number of units available for sale. The future direction of condominium prices in the resale market in the short term is largely out of our government’s control.

If condo inventory continues to increase, we could see some downward pressure on condo prices, further widening the gap between resale prices and the prices pre-construction condo investors paid for their units.

To mitigate this risk, our government could reverse its plans to reduce the number of non-permanent residents in Canada over the next three years. If the federal government follows through with its plans, Canada’s population will go from growing by just under 1.3 million to approximately 300,000 people annually. This dramatic decrease may contribute to future downward pressure on condo prices and rents.

But if our government wants to keep condo prices and rents as high as possible to mitigate the potential negative side effects of the overpriced condos scheduled to be completed in the years ahead, it may reverse course on these plans. Extending Canada’s current population boom isn’t guaranteed to drive prices and rents higher, but at a minimum, it would help raise the floor of any declines.

Finally, buyers and sellers in Toronto’s housing market will want to keep a close eye on the trends I highlighted above because it’s unclear how far policymakers will go to keep prices from falling. I would encourage readers to subscribe to our Move Smartly blog here and our Move Smartly YouTube channel, where I frequently discuss trends that might influence their real estate decisions.

House sales (low-rise freehold detached, semi-detached, townhouse, etc.) in the Greater Toronto Area (GTA) in June 2024 were down 13% compared to the same month last year.

New house listings in June were up 8% compared to last year.

The number of houses available for sale (“active listings”) was up 45% in June compared to the same month last year.

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number of homes sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell, given the current level of demand? The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

While the current level of MOI gives us clues into how competitive the market is on-the-ground today, the direction it is moving in also gives us some clues into where the market June be heading.

The MOI for houses increased to 3.1 in June.

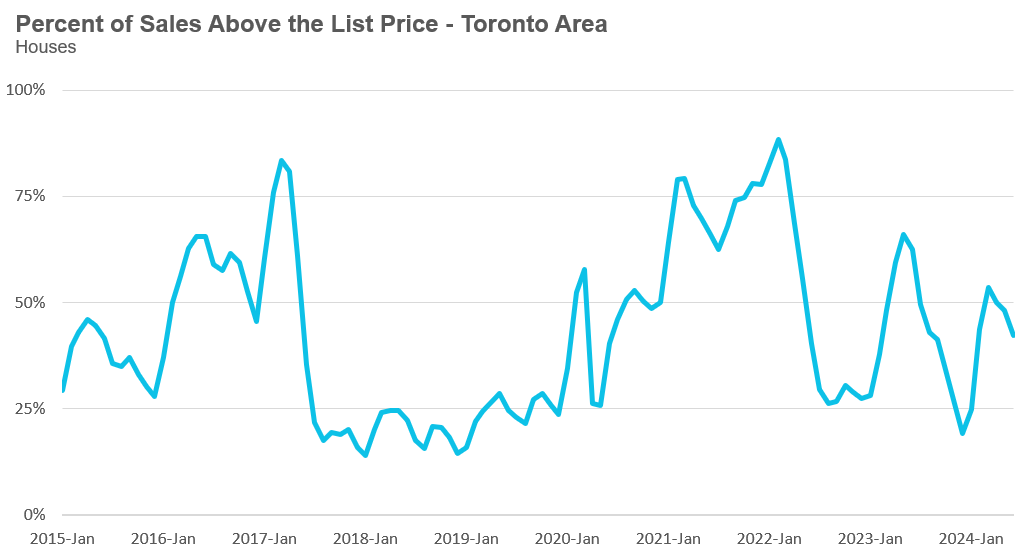

The share of houses selling for more than the owner’s list price decreased to 42% in June.

The average price for a house in June was $1,382,118 in June 2024, down 5% compared to the same month last year.

The median house price in June was $1,200,000, down 6% over last year.

The median is calculated by ordering all the sale prices in a given month and then selecting the price at the midpoint of that list such that half of all home sales are above that price and half are below that price. Economists often prefer the median price over the average because it is less sensitive to big increases in the sale of high-end or low-end homes in a given month, which can skew the average price.

Condo (condominiums, including condo apartments, condo townhouses, etc.) sales in the Toronto area in June 2024 were down 27% compared to the same month last year.

New condo listings were up 16% in June over last year.

The number of condos available for sale at the end of the month, or active listings, was up 70% over last year.

Condo months of inventory increased to 5.4 MOI in June.

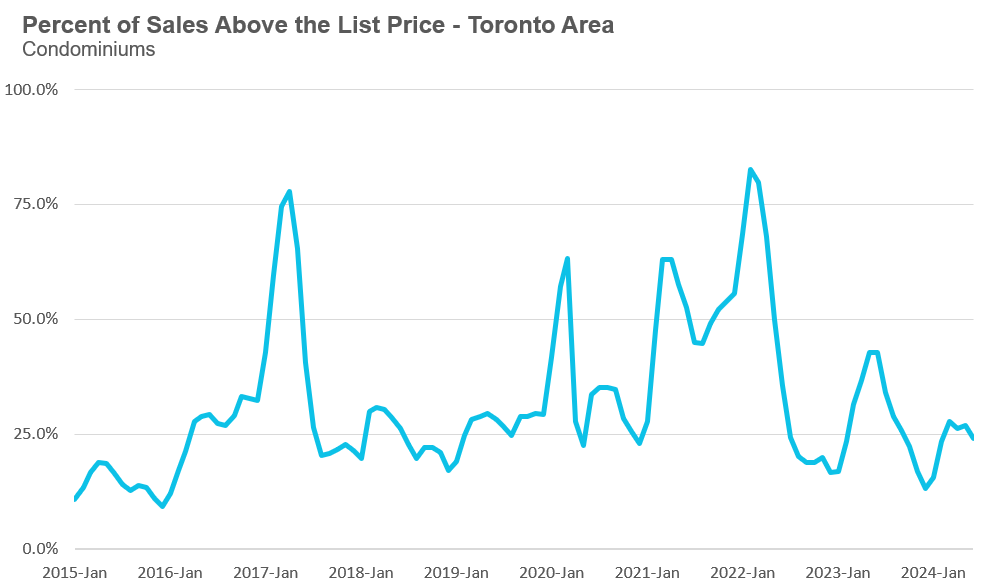

The share of condos selling for over the asking price increased slightly to 24% in June.

The average price of a condo in June was $753,111, down 2% from last year. The median price was $670,000, down 3% from last year.

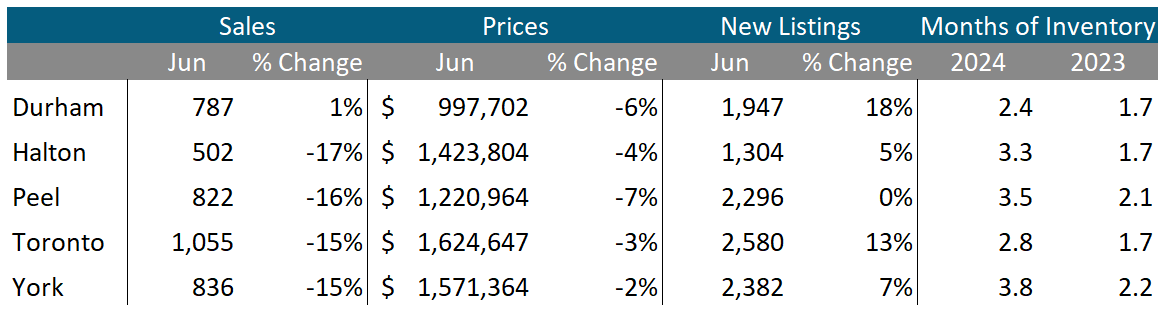

Sales were up by 1% in Durham, the GTA’s most affordable region, but down by double digits in the other five regions. Durham also saw the sharpest increase in new listings, up 18% over last year, followed by Toronto at 13%. Average prices were down in all five regions. Months of inventory was up across all regions, with York (3.8) and Peell (3.5) seeing the highest MOI of houses in the Greater Toronto Area.

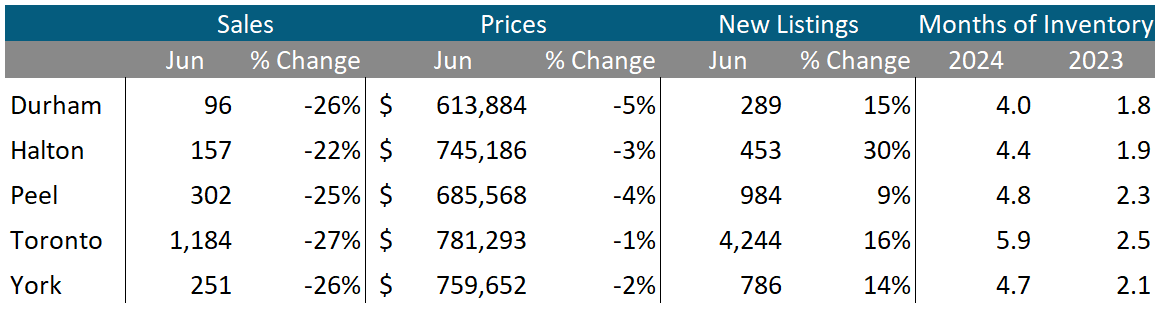

Condo sales were down by over 20% in all regions in June. Average prices were also down across the GTA. New listings and MOI were well above last year’s level for all regions. The City of Toronto has the highest MOI across all five regions.

See Market Performance by Neighbourhood Map, All Toronto and the GTA

Greater Toronto Area Market Trends