FREE PUBLIC WEBINAR: WATCH REPORT HIGHLIGHTS & Q/A - Thurs Jan 12th 12PM ET

Join John Pasalis, report author, market analyst and President of Realosophy Realty, in a free monthly webinar as he discusses key highlights from this report, with added timely observations about new emerging issues, and answers your questions. A must see for well-informed Toronto area real estate consumers.

I like to start the new year by reviewing the past year in Toronto’s housing market and to identify the key trends that I believe ended up mattering the most.

In addition to data on average prices, sales and listing inventory, I take note of what was sentiment on the ground and how did it evolve over time?

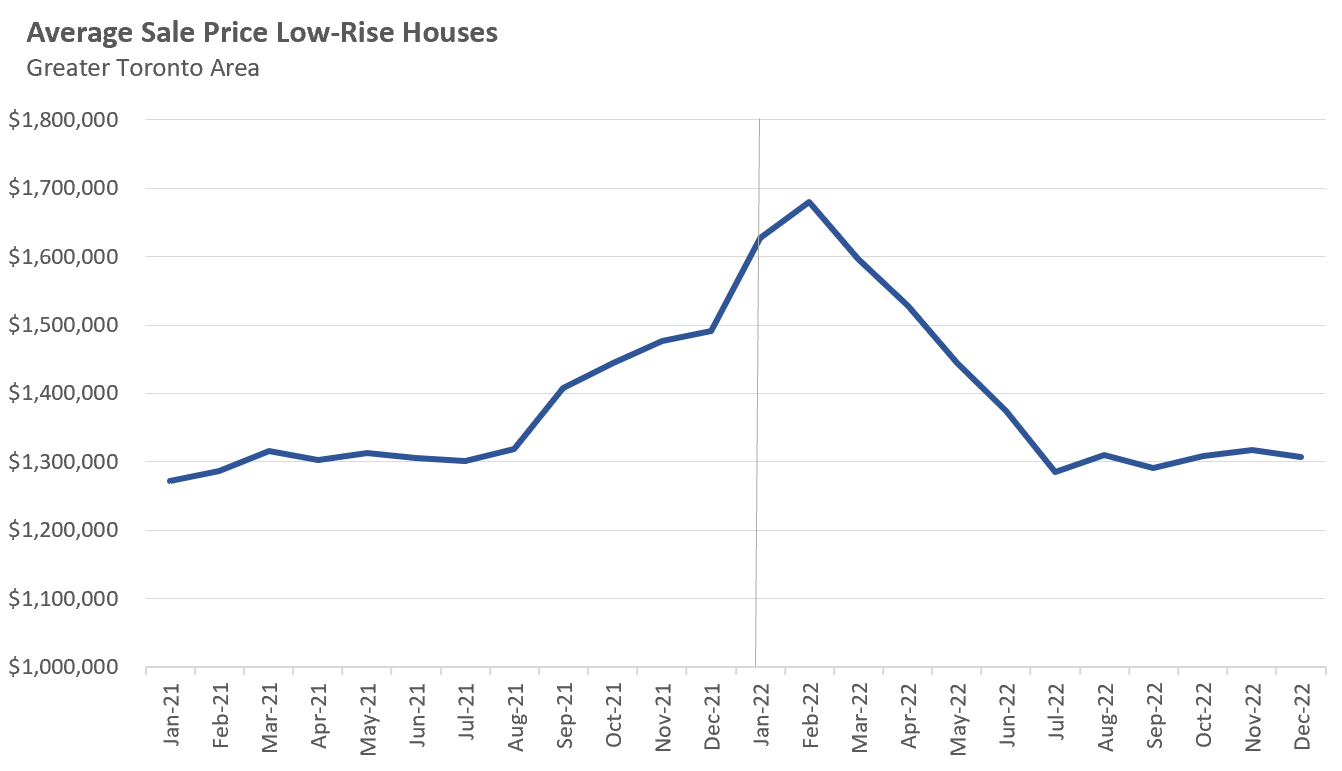

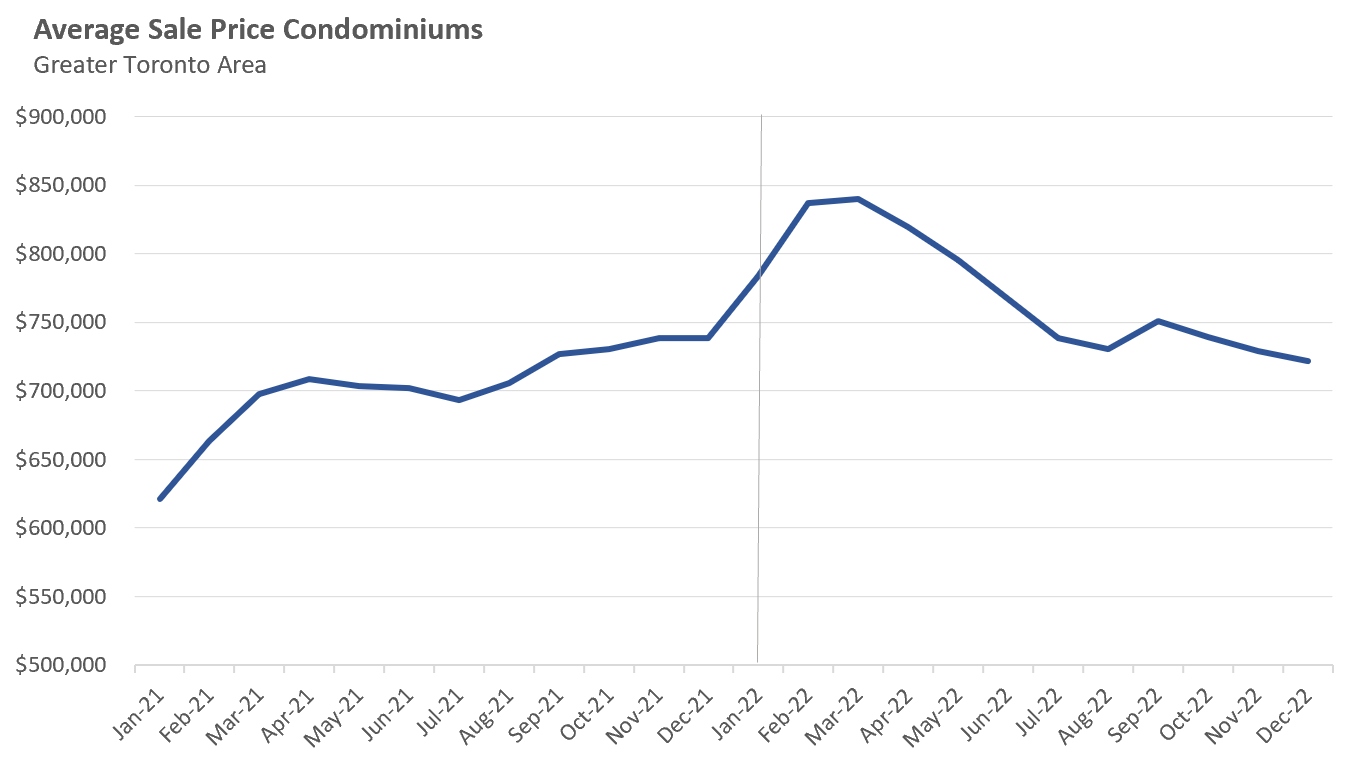

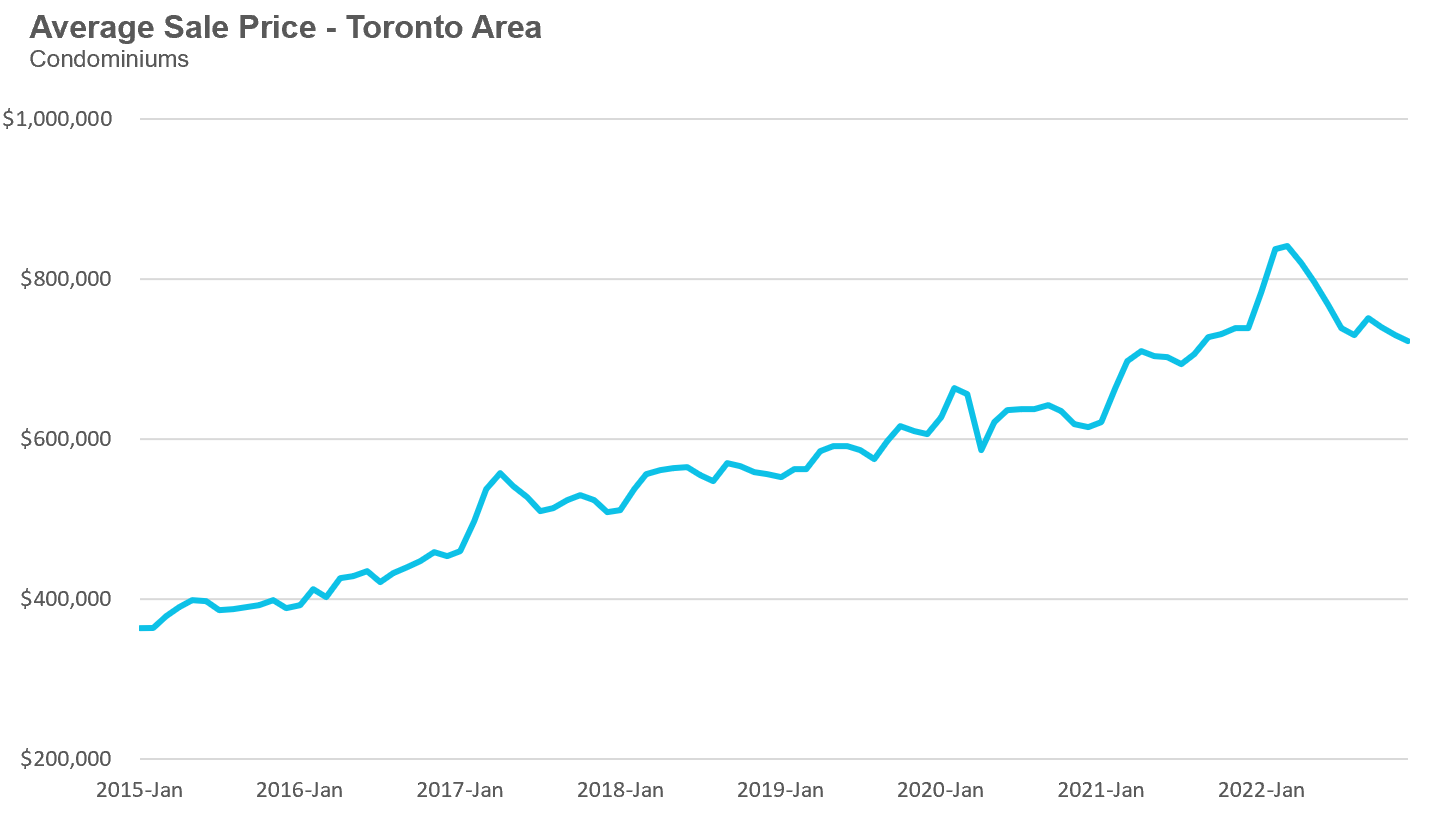

Since trends in the first quarter of a year are a continuation of the quarter preceding it, I start by looking back to the end of 2021. The following two charts show the average price, first for low-rise houses and then for condominium buildings and townhouses (condos) in 2021 and 2022, with a vertical line marking the start of 2022.

From these charts, we can see that both low-rise houses and condos saw prices begin to accelerate in 2021.

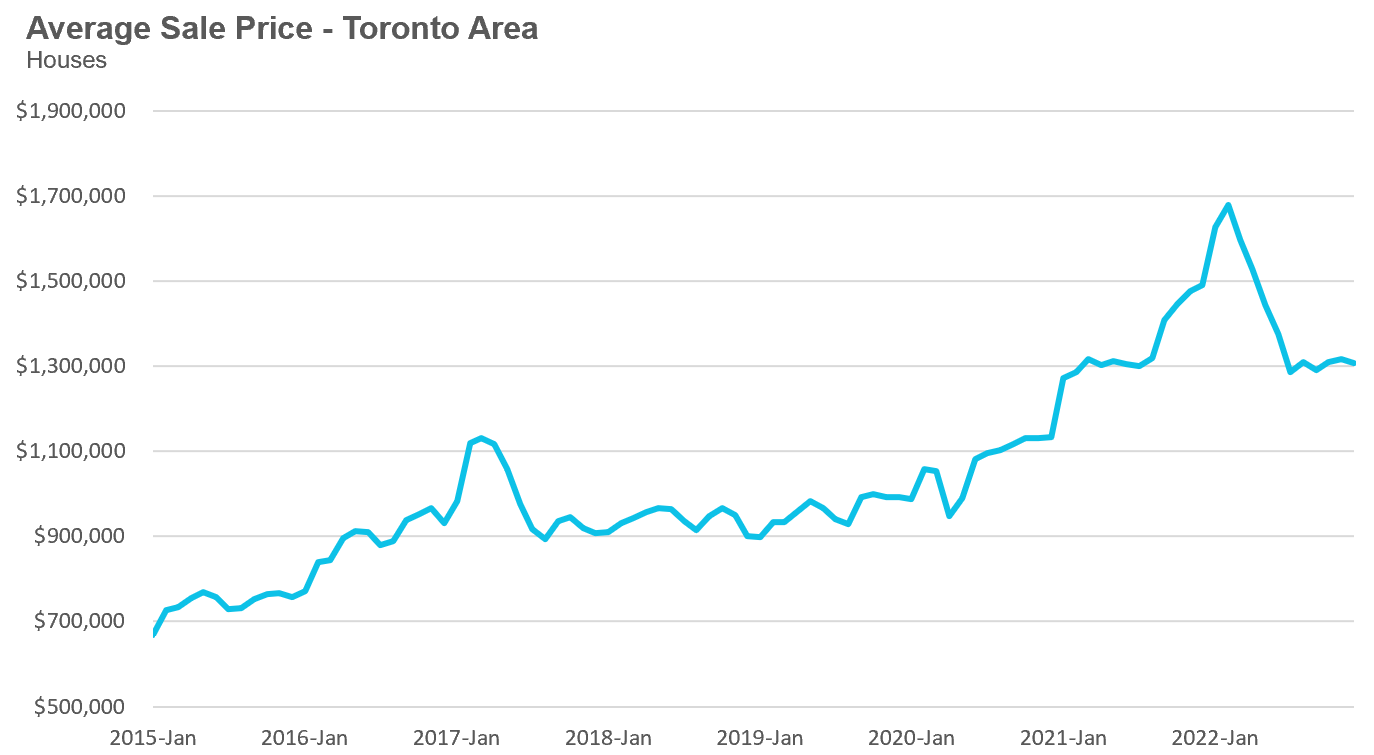

The low-rise market in particular was quite interesting because from January to August of 2021, prices were flat and the market was very balanced, before average prices took off, climbing from $1.32M in August 2021 to a peak of at $1.68M in February 2022, a 27% increase in just 6 months.

Condo prices accelerated 19% over that same period.

There’s no concrete explanation for why the market went from being relatively calm during the first half of 2021 to a frenzied one, other than an irrational exuberance leading to bubble conditions that peaked in early 2022.

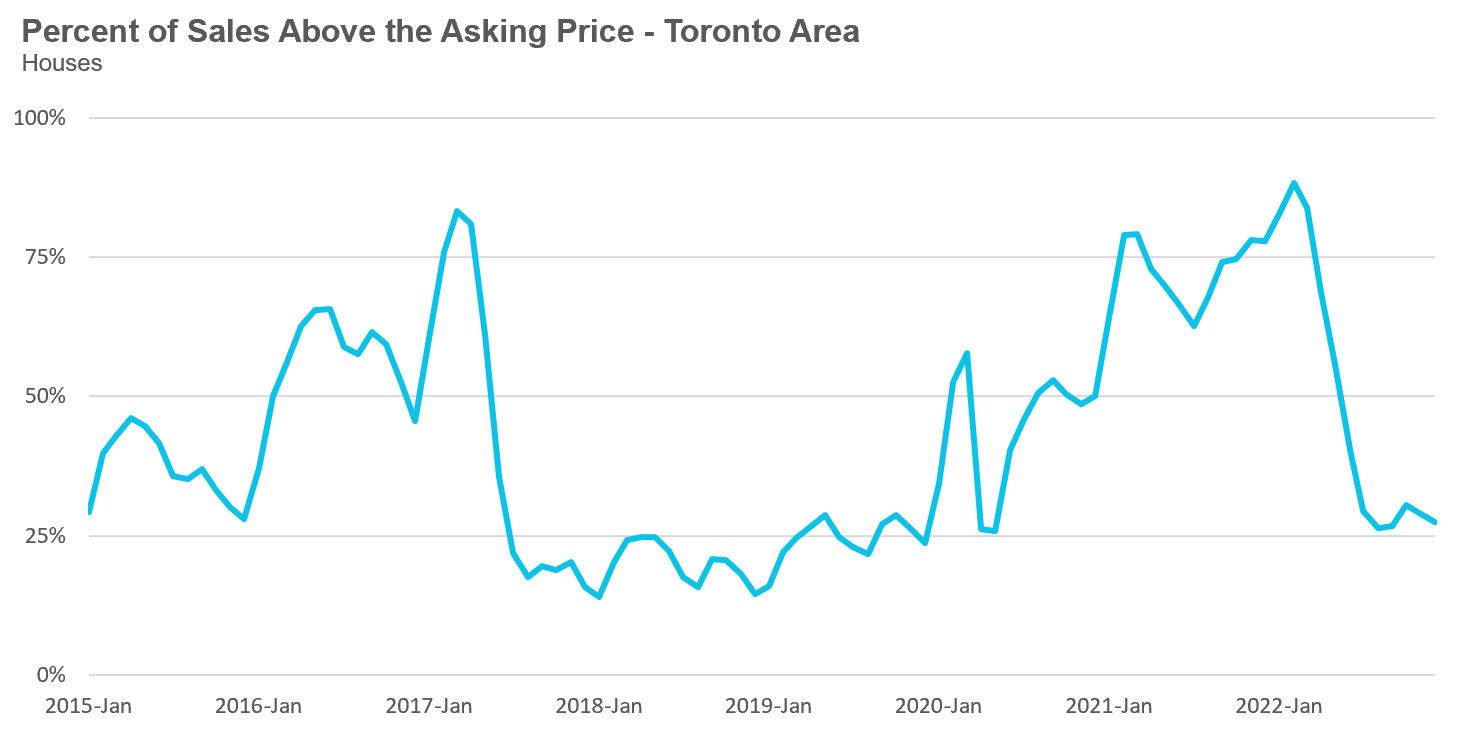

In the first two months of 2022, the market was unbelievably competitive with 9 in 10 low-rise houses (and 8 in 10 condos) receiving multiple offers and selling for more than the property’s list (or asking) price. In many cases, low-rise houses were receiving upwards of 50 offers on their offer nights from desperate buyers eager to buy a home.

While sellers and their agents often list homes with artificially low asking prices to generate more buyer interest and multiple offers, this strategy rarely works on almost every home listed for sale. For example, for most of 2018 and 2019, fewer than 25% of homes received multiple offers and sold for more than the seller’s asking price. During the first quarter of 2022, 9 in 10 homes were receiving multiple offers because buyers were buying anything, they were desperate.

But towards the end of February 2022, I started to notice some early signs of the housing market cooling, which I wrote about in my March 2022 report here. The earliest signs were homes receiving fewer showings, getting fewer offers on offer nights and in some cases not even selling on their offer night because it didn’t attract a price the seller was happy with.

So why this sudden decline in demand?

This again is very hard to say with any certainty, but I think there were two primary reasons.

Firstly, after such a frenzied market, buyers who kept losing out on multiple offers week after week gave up and moved to the sidelines as buyer fatigue set in. The other big factor was that the media headlines turned more pessimistic, with the message that the Bank of Canada was likely going to raise rates aggressively to cool Canada’s high inflation rate which would likely result in a chill in house prices. No buyer wants to be caught out buying at the peak of a market.

Many of the sellers who had bought homes in January or February 2022 and still needed to sell their current home started to panic when they found that demand had cooled and they were getting far fewer showings than they expected. Every week that passed, more sellers were willing to sell for less than what their neighbours sold for the week earlier for the security of having a firm sale agreement in place in order to get a mortgage on the home they had purchased.

After average low-rise home prices peaked at $1.68M in February, they fell to $1.29M by July, a $394K or 23% decrease in just five months. I discuss the dynamics during this period in more detail in my September 2022 report.

As we moved towards the summer months of 2022, the volume of monthly sales hit 20-year lows, a decline that was largely driven by the surge in interest rates which made it harder for buyers to qualify for a mortgage. By July, the Bank of Canada had increased rates from 0.25% to 2.5% and most analysts were expecting more hikes in the future.

But in spite of sales hitting these 20-year lows, something unexpected happened — rather than home prices falling further as would be expected, prices stayed flat or plateaued from July till the end of 2022.

One of the primary reasons that prices plateaued is because the decline in sales was accompanied by a decline in the number of new homes coming onto the market as sellers were becoming more stubborn and unwilling to reduce their price and sell in a slower market. In my September 2022 report, I showed that there was a big increase in the number of homes that were simply being taken off the market by sellers or were being rented after the owner was unsuccessful at selling for their desired price.

And this is how 2022 ended with six consecutive months of low sales, low listings and relatively flat prices.

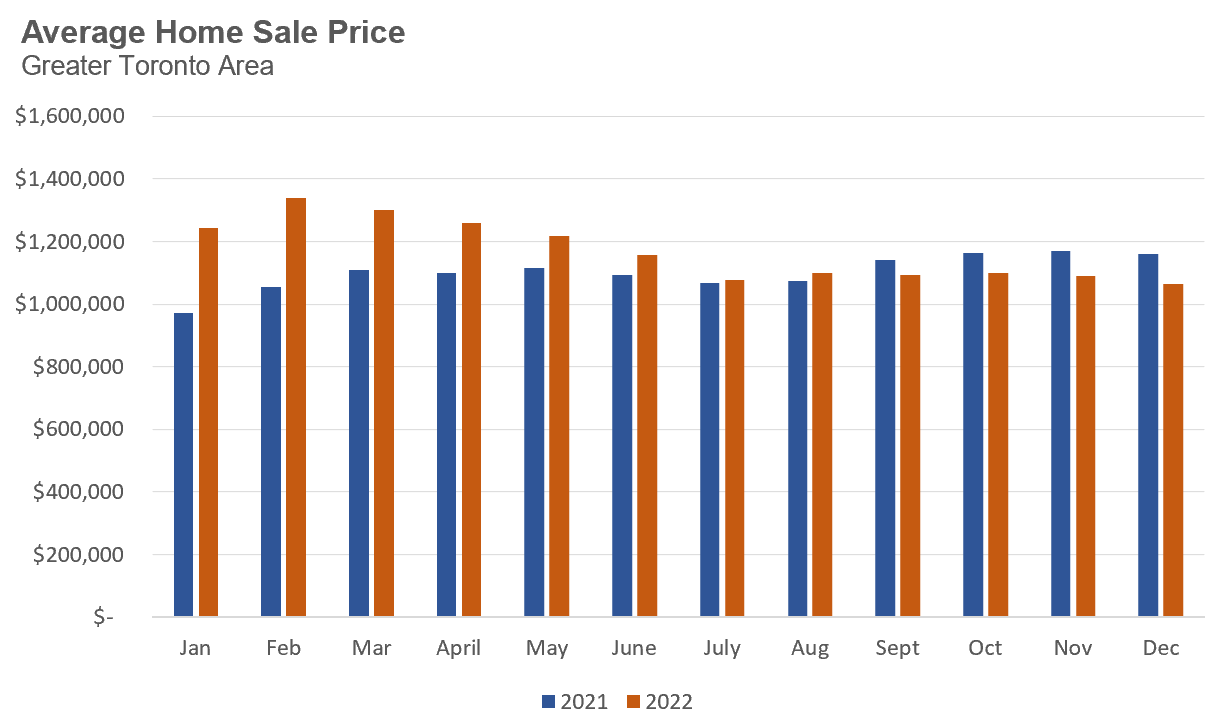

Before wrapping up my year in review, it’s worth highlighting one odd statistic that some might stumble across when looking at annual statistics comparing 2022 and 2021. Even though total sales transactions were down 38% when compared to 2021, the average price for all homes was up 8.6% in 2022 over the previous year.

Just how can annual prices be up given the dramatic decline in sales caused by one of the fastest rate hiking cycles ever?

Firstly, if we compare sale prices by month in 2021 and 2022 we see that even though average prices today are well below the peak reached in February 2022, average prices were up from January to August 2022 when compared year-over-year to corresponding months in 2021.

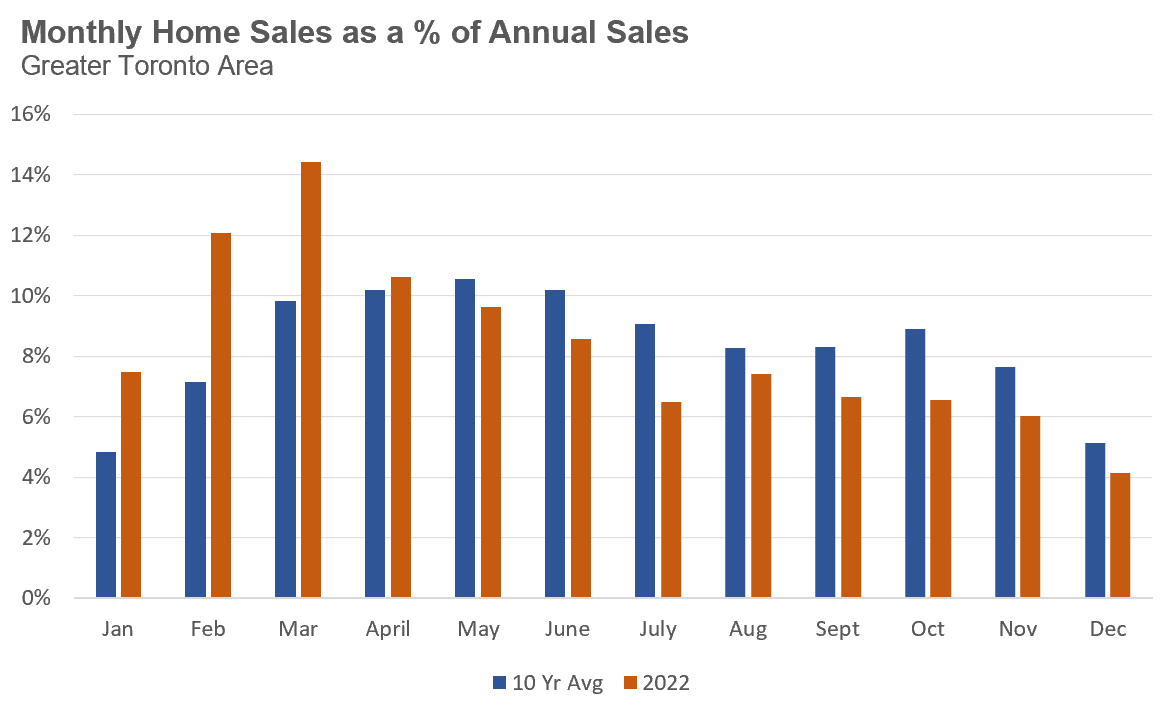

Furthermore, a disproportionate number of sales in 2022 occurred during the first quarter, when prices were at their highest, and before sales fell dramatically.

Looking at sales each month as a % of annual sales for 2022 over the previous 10 years in the above chart, we can see that a far greater share of sales in 2022 occurred during the first quarter, which is helping to skew the annual average price for homes in 2022 up.

While the average sales price in 2022 is technically up for the year, it’s the notable downward trend that marked the last six months of 2022 that has mattered most as we enter 2023.

Who doesn’t like a Top 10 list to kick off the New Year?

In a normal annual list looking at neighbourhood appreciation, we would typically compare the annual average home sale prices in each neighbourhood for the target year (2022 in this case) against the previous year to see how home prices have changed over that period.

But 2022 was a crazy year — given that home prices peaked during the first quarter of 2022 and then fell dramatically after that, a traditional comparison is less relevant.

What’s more interesting is to compare how home prices have changed since the peak in the first quarter of 2022.

Which areas in the Greater Toronto Area (GTA) saw the biggest decline in home prices this year and which areas saw more stability?

The Method

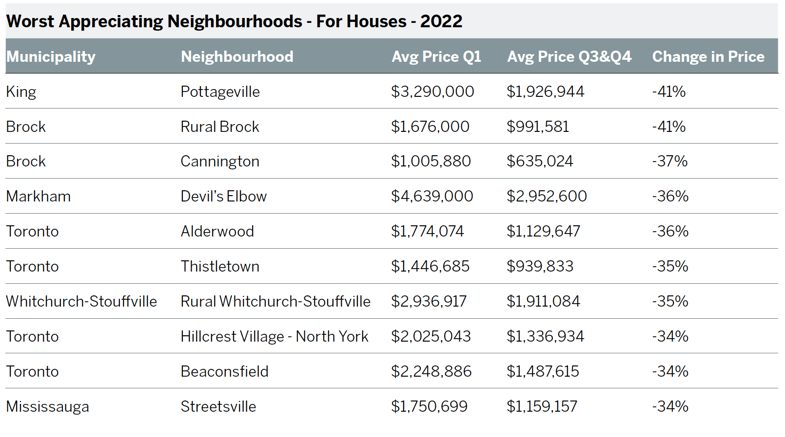

This analysis compares average prices during the first quarter of 2022 against the average during the last two quarters of 2022. The second quarter was excluded because prices were trending down during those three months before plateauing at the start of the third quarter. I decided to use the last two quarters of 2022, rather than just the fourth quarter, because prices started to flatten July onwards and because, given record lows, the number of sales were very low during this entire period so having an extra quarter of data would help increase the number of transactions for each neighbourhood. Neighbourhoods needed at least five sales in each period to have been included in the analysis.

Finally, it’s important to note that these results do not mean that all homes in a given neighbourhood declined (or increased) by the percentage indicated in this list. Neighbourhood price trends over short periods of time can always be vulnerable to shifts in the types of homes selling from one period over another (e.g., such as when a new condo is completed, etc.) which can dramatically skew the results. You should consult a real estate professional to determine how the value of your particular home may have changed over the past year.

We generate separate lists for houses and condos because different mixes of housing (i.e., lower priced condos vs. higher priced houses) will screw average price numbers, so it’s useful to look at these separately. Houses here represent all detached, semi-detached, townhomes and linked homes while condos include condo building apartments and townhomes.

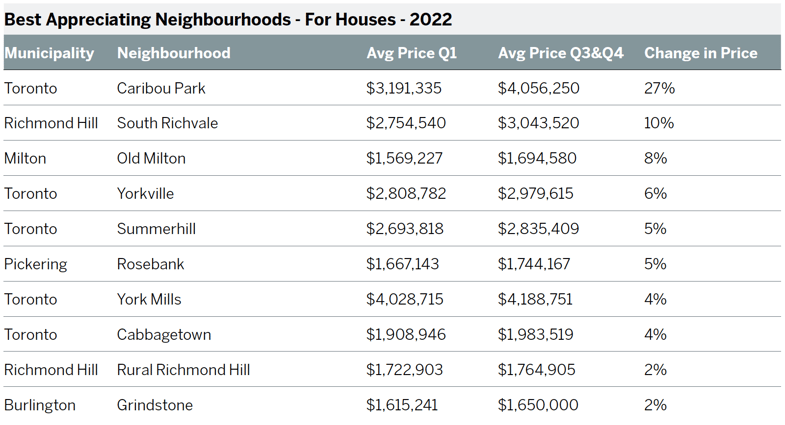

The one noteworthy trend from the worst appreciating list is that the top three neighbourhoods for houses are small communities on the outskirts of the GTA. These types of communities saw a big surge in demand for homes during the Covid-19 pandemic, as movers sought out more space during lockdown and work-from-home protocols, and a resulting spike in prices, are now adjusting down faster than other areas.

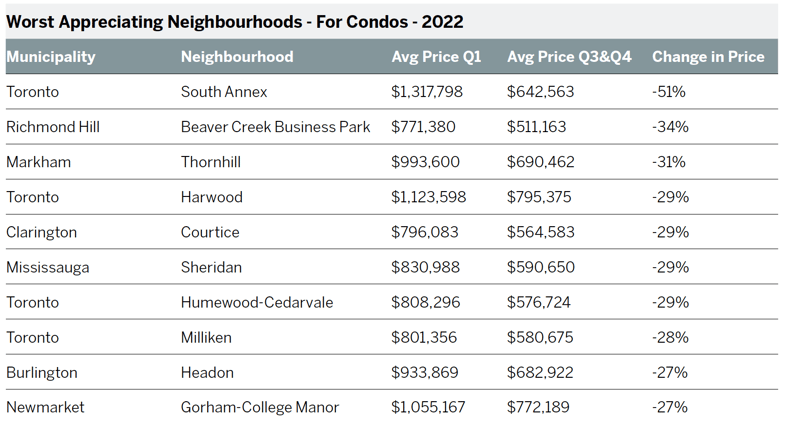

In the worst appreciating list for condos, it’s noteworthy that the list contains a mix of neighbourhoods from all five of the GTA regions, again suggesting that when it comes to condos, it’s important to consider each building, complex and area carefully.

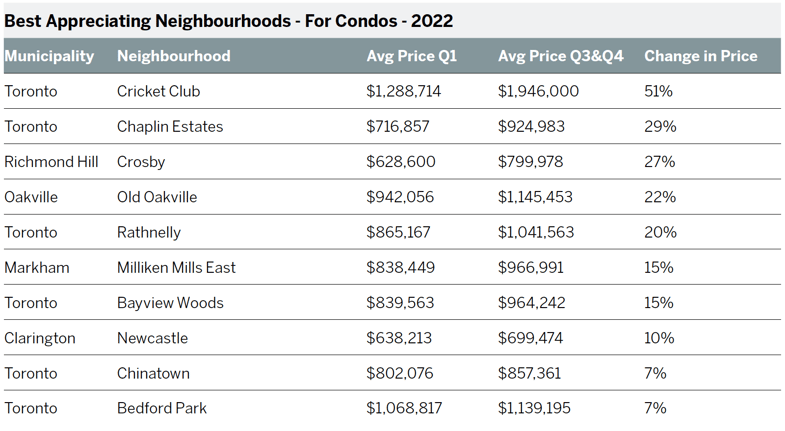

Similarly, the best appreciating lists for both houses and condos are a real mix of neighbourhood types throughout the GTA, including many that we often see on these types of lists, such as Caribou Park and Yorkville. Also, unlike the worst appreciating list, the best appreciating neighbourhoods for houses, except for one or two exceptions, saw very modest appreciation gains when compared to gains in neighbourhoods for condos.

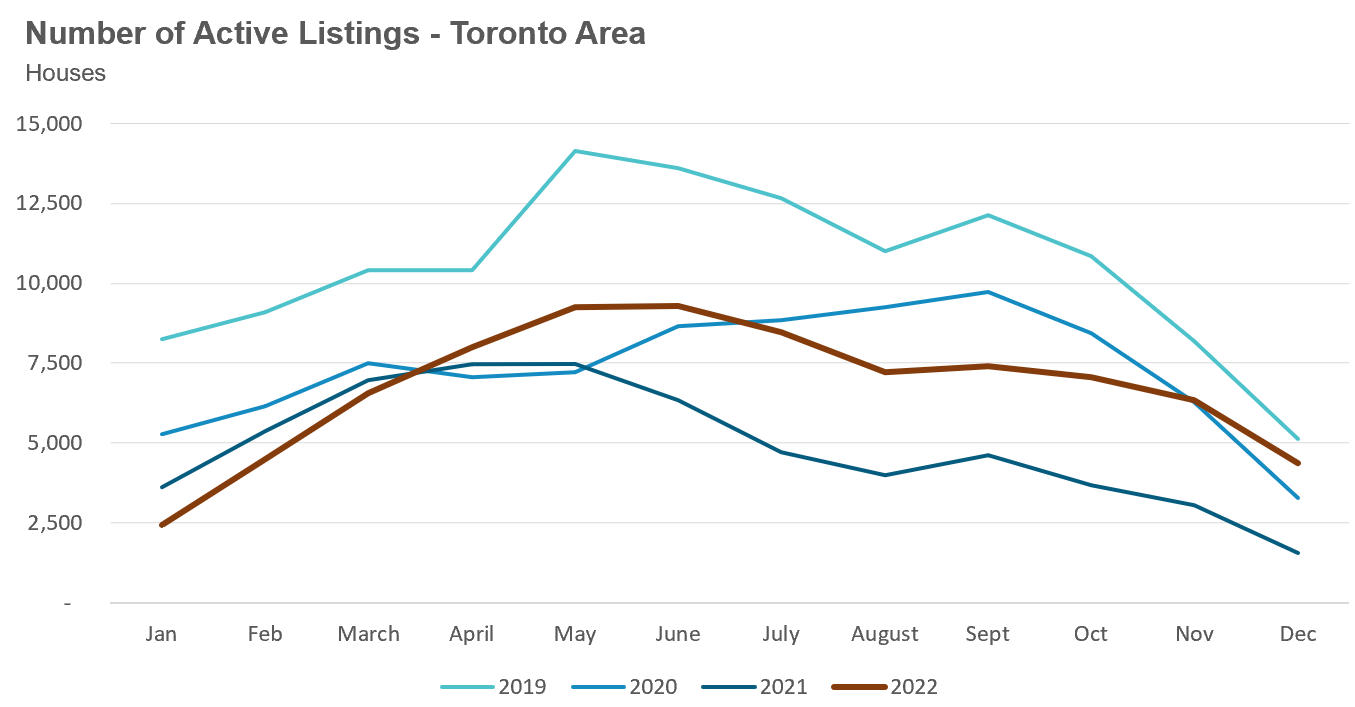

House sales (low-rise freehold detached, semi-detached, townhouse, etc.) in the Greater Toronto Area (GTA) in December 2022 were down 46% over the same month last year and remain well below historical levels for the month.

New house listings in December were down 25% over last year.

The number of houses available for sale (“active listings”) was up 179% when compared to the same month last year, but still well below pre-COVID levels for the month of December. It’s worth noting that the extremely low inventory levels in the second half of 2021 were due to a surge in demand as the market accelerated towards the peak in February 2022.

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number of homes that sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell given the current level of demand?

The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

While the current level of MOI gives us clues into how competitive the market is on-the-ground today, the direction it is moving in also gives us some clues into where the market may be heading.

The MOI for houses remained relatively unchanged at 2.4 MOI in December.

The share of houses selling for more than the owner’s asking price dipped slightly to 27% in December.

The average price for a house in December was $1,307,513 in December 2022, well below the peak of $1,679,429 reached in February and down 12% when compared to the same month last year.

The median house price in December was $1,100,000, down 17% over last year, and below the peak of $1,485,000 reached in February.

The median is calculated by ordering all the sale prices in a given month and then selecting the price that is in the midpoint of that list such that half of all home sales were above that price and half are below that price. Economists often prefer the median price over the average because it is less sensitive to big increases in the sale of high-end or low-end homes in a given month which can skew the average price.

Condo (condominiums, including condo apartments, condo townhouses, etc.) sales in the Toronto area in December 2022 were down 52% over last year and well below pre-COVID sales volumes for the month of December.

New condo listings were down 19% in December over last year and in line with historical listing volumes for the month of December.

The number of condos available for sale at the end of the month, or active listings, was up 140% over last year.

Condo inventory levels increased slightly to 3.3 MOI in December.

The share of condos selling for over the asking price decreased to 17% in December.

The average price for a condo in December was $721,885, down from the peak of $840,444 in March, and down 2% over last year. The median price for a condo in December was $645,000, down 2% over last year, and down from the March peak of $777,000.

Houses

Average prices were down over last year across all five regions with Peel and Durham seeing the biggest decline in prices. Sales were down significantly across all regions and inventory levels were well ahead of last year’s level.

Condos

Average condo prices were down over last year in Durham, Peel and Halton down, with Toronto and York seeing little change. Sales were down significantly across all regions and inventory levels were well ahead of last year’s level.

See Market Performance by Neighbourhood Map, All Toronto and the GTA

Greater Toronto Area Market Trends