Why things are different from the last time we saw a market downturn in 2017.

Hit play to watch new video from John Pasalis of Realosophy Realty above and read the full story below. For more analysis of the Toronto real estate market this month, read our monthly report.

In last month’s report, I discussed why some of the trends we are seeing in Toronto’s housing market today (rapidly declining home sales and prices) look very similar to the trends we saw in 2017 after Toronto’s housing bubble burst in the first quarter of that year, but I also noted that the economic conditions we are facing today are very different from 2017.

In this month’s report, I want to unpack the three very big differences in our economy today when compared to 2017 - a high inflation rate, rapidly rising interest rates and higher levels of household debt - and how these factors can have a material impact on what happens in the housing market in the months and years ahead.

These are economic conditions we have not seen in Canada in decades and when we are trying to make informed real estate decisions it helps to understand some of the broader economic trends that will influence the future path of home prices.

Why High Inflation is Bad

Inflation is a word that has been all over the news lately. What is inflation? Let’s start with how the Bank of Canada (BOC) defines it:

“Inflation is a persistent rise the in the average level of prices over time.”

- The Bank of Canada

Prices typically rise over time, but the BOC’s goal is to have prices rising in a range between 1 to 3%. But we all know that the cost of the things we buy and consume, from food to gasoline, have been rising far more rapidly than 1 to 3%.

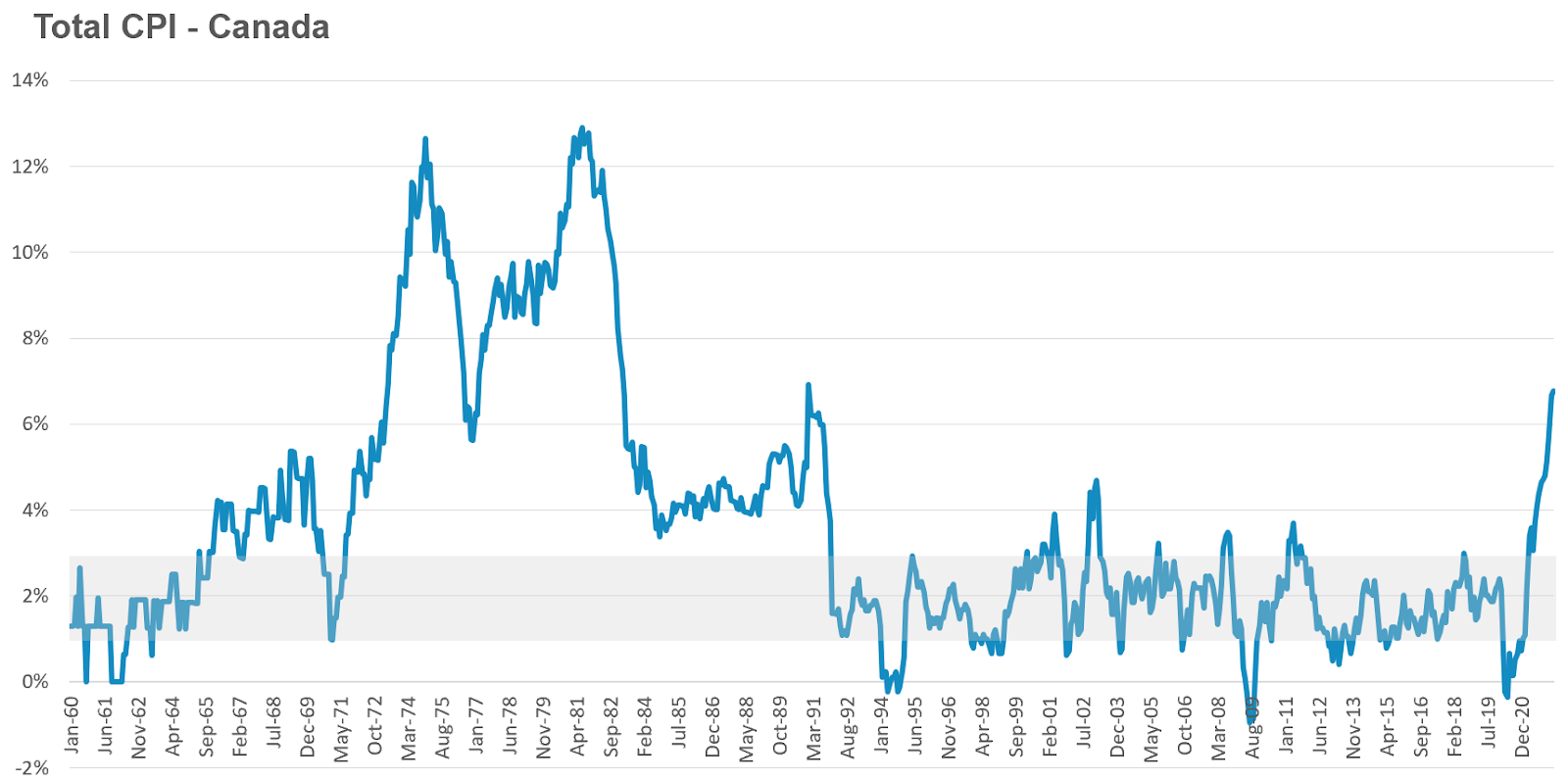

The BOC measure of inflation shows that prices are rising closer to 8% per year, and some experts even think this estimate is low.

So why is a high inflation rate bad?

For households, it means that the monthly paycheque doesn’t go as far in covering living expenses and without a rise in income, this can strain household finances.

But inflation is also a big problem for businesses. When inflation is stable, say at around 2%, which is the BOC target, it’s a lot easier for businesses to forecast future costs. But when inflation is high and volatile, it makes it a lot harder for businesses to make investments today without clarity around tomorrow’s costs.

Here’s a chart showing the Consumer Price Index (CPI) which is the measure the Bank of Canada uses to measure inflation:

How Higher Interest Rates Impact Us

So how does the BOC lower the inflation rate?

The BOC’s main policy tool is their policy rate, also called the overnight rate. This is the rate that variable rate mortgages are based on, which means that as the policy rate increases so does the interest rate on your variable rate mortgage. (These rate increases, through their impact on bond markets, also indirectly affect new and renewing fixed rate mortgages.)

The BOC’s policy rate was 0.25% in March and at the time of writing this report in early July 2022, it has been raised to 1.5%, with most economists expecting it to increase another .75% at their next policy meeting in mid-July, and potentially reaching as high as 3% by the end of the year.

So how does raising interest rates cool inflation?

Rapidly rising prices are due to an imbalance between supply and demand, or too much demand chasing too few goods. As the BOC’s policy rate can’t do much on the supply front (i.e., to produce more oil or more food), it is utilized to impact demand.

As interest rates increase, people eventually start spending less. A household that was planning to borrow $100K from their home equity line of credit to renovate their house may put that on hold if they would have to pay a much higher interest to pay that money back. As people start spending less, this takes demand out of the market and should help ease the inflation rate over time.

But it’s not just households who spend less - businesses also scale back investments because the cost to borrow funds to finance investments is high, but also because the high inflation rate makes it hard to forecast future costs.

This combination of reduced consumer and business activity is why periods of high interest rates and high inflation can lead to recessions, which can lead to further economic downturns and even job losses.

Why High Household Debt Matters

In the Bank of Canada’s June 2022 Financial System Review, they highlighted six vulnerabilities in the financial system and at the top of that list was “elevated level of household indebtedness.”

(Side note: For anyone who is interested in learning more about the current macroeconomic environment in Canada, I would recommend reading the Bank of Canada’s Financial System Review, which offers a brief but very detailed summary written in plain language.)

High household debt is a significant risk when interest rates are rising rapidly because the costs to service (or payback) our debt rises with interest rates. As this usually happens while inflation is also very high, this additional debt expense comes at a time when the cost of all other household expenses is also rising.

One of the Bank of Canada’s concerns is understanding if highly indebted households can continue servicing their debt as rates increase without significantly reducing their household spending/consumption and that these households are also far more likely to face financial difficulties if there is a shock to their income due to job loss.

How These Factors Impact Our Market

As discussed, the future path of home prices is largely determined by interest rates.

Let’s look at how changes in interest rates impact a household’s mortgage payments:

- A year ago you could get a 5 year mortgage for around 2%

- The mortgage payment on $1M - just to pick a round number - would have been $4,200

- But that same $1M mortgage with a mortgage rate of 5% results in a payment of $5,800 per month, $1,600 more, an almost 40% increase

As rates increase, households can’t spend as much as they did a year ago to buy a home because their monthly mortgage payments would be much higher so to stay in the market, they would have to reduce their budget for buying a home, resulting in downward pressure on home prices.

The second thing to keep in mind is that the future path of interest rates is largely going to depend on the inflation rate. If the inflation rate remains high then the BOC will keep interest rates high. Changes to the policy rate will also depend on current economic conditions, but even if we find ourselves in a recession a year from now, the BOC will have a hard time lowering rates to stimulate the economy if inflation remains elevated.

And finally, if high inflation and high interest rates are with us for an extended period of time this may begin to strain highly indebted households, especially if households see a shock to their income due to a recession.

So these are just some of the macroeconomic factors that will likely impact the future path of home prices over the next 12-24 months. But while these macro factors help us understand the broader trends that might impact the housing market, real estate trends are very local.

When thinking about how stable or unstable prices are over the next 12+ months, these trends will likely be very different depending on the type of home and neighbourhood you’re considering buying or selling in.

It will be important to really understand these very local micro trends in the neighbourhoods you’re most interested in - and I’ll be touching on this topic in future reports.

Click here to book a consultation with John

Click here to sign up for the Homebuyer's Bootcamp online course - Use code: 50OFF

The Move Smartly monthly report is powered Realosophy Realty Inc. Brokerage, an innovative residential real estate brokerage in Toronto. A leader in real estate analytics, Realosophy educates consumers at Realosophy.com and MoveSmartly.com and helps clients make better decisions when buying and selling a home.

Email report author John Pasalis, Realosophy President

Published: July 28, 2022