Two months ago, I wrote about bubble-like conditions in Toronto’s suburban housing market.

At the time, house prices were appreciating by 15 to 20% per year and there were plenty of signs that things were going to get even hotter. Many houses for sale were receiving upwards of 20 to 30 offers from buyers and the prices that buyers were paying were starting to look irrationally high. When looking at the actual sales and inventory data, all signs were pointing to a market that was going to get hotter in the next few months with no signs of cooling.

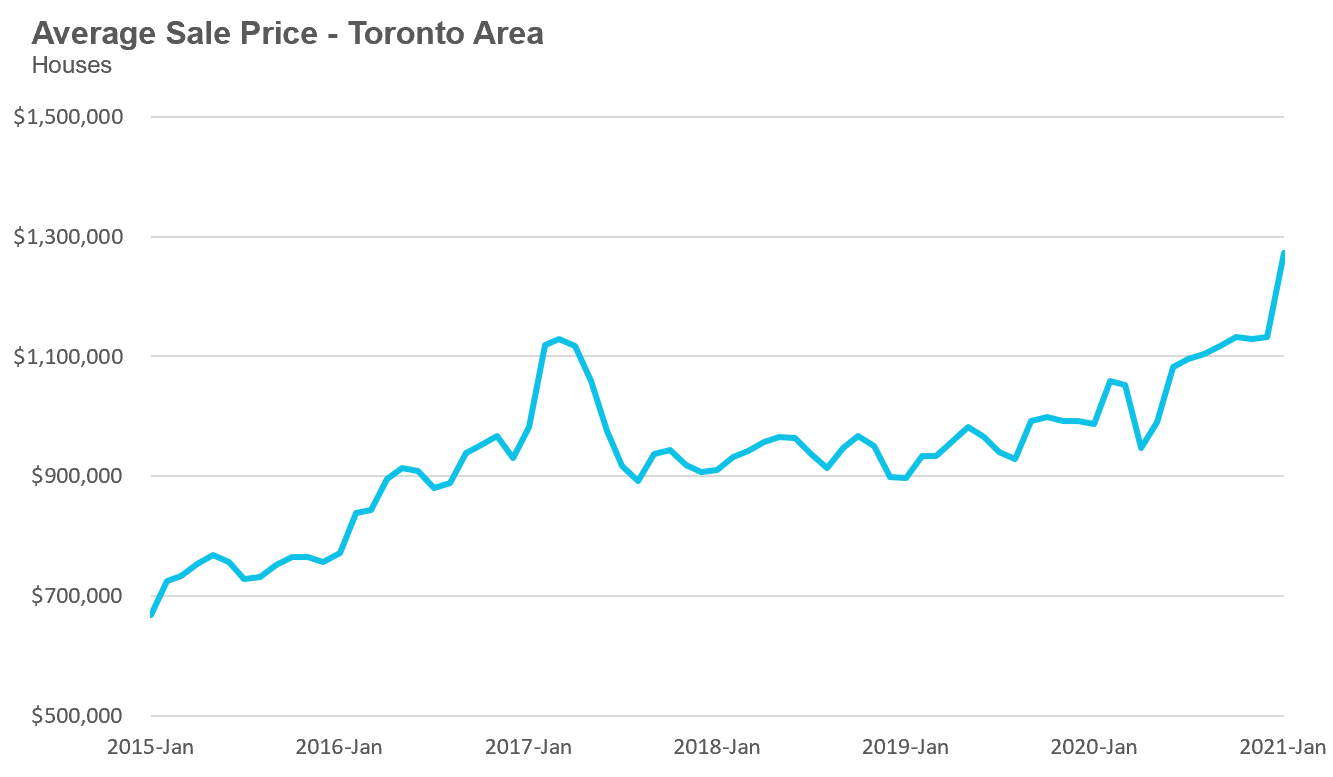

Unfortunately, this is precisely what happened. In the two months since that report, average sale prices for suburban homes have surged 16% from $1,052,940 in November 2020 to $1,221,092 in January 2021. Median prices are up 14% over the same period.

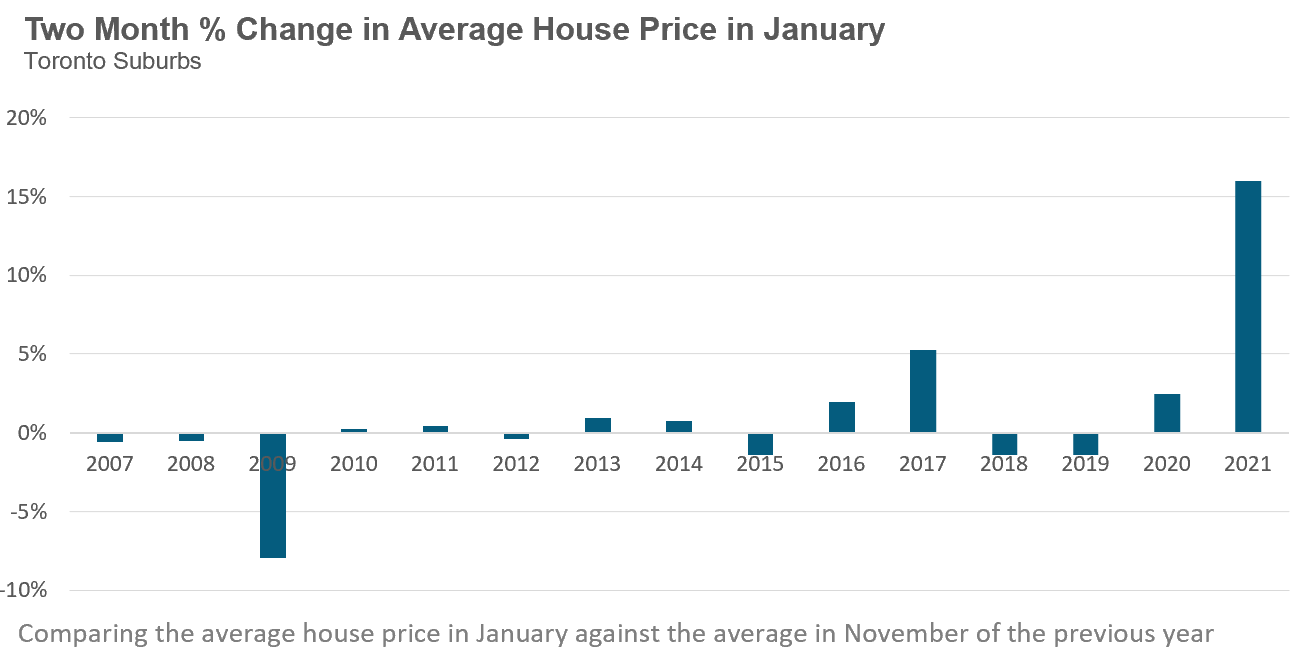

While we don’t typically compare house price changes on a month-over-month basis because seasonal differences can impact the average, it’s worth noting that average prices rarely change very much during the two months from November to January.

Below is a chart showing the 2 month change in average house price for suburban houses between November and January since 2007. You’ll note two outliers in the trend (aside from last month). The decline in 2009 was during the financial crisis and the 5% increase in 2017 was leading up to the peak of Toronto’s last real estate bubble.

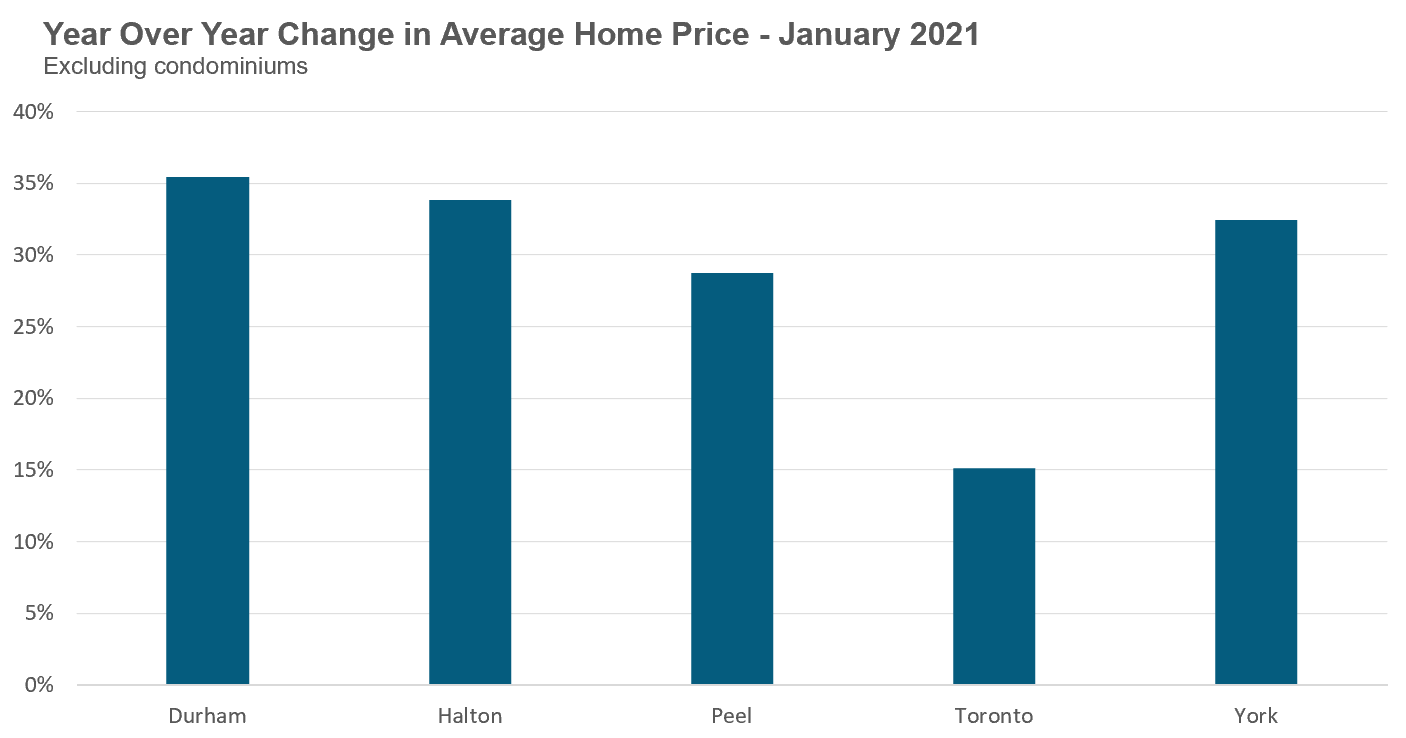

When comparing average sale prices in January 2021 on a year-over-year basis we see that average prices in Toronto’s suburbs were up by over 30% in Durham, Halton and York regions and by 29% in Peel Region. Prices in the City of Toronto were up a more modest 15%.

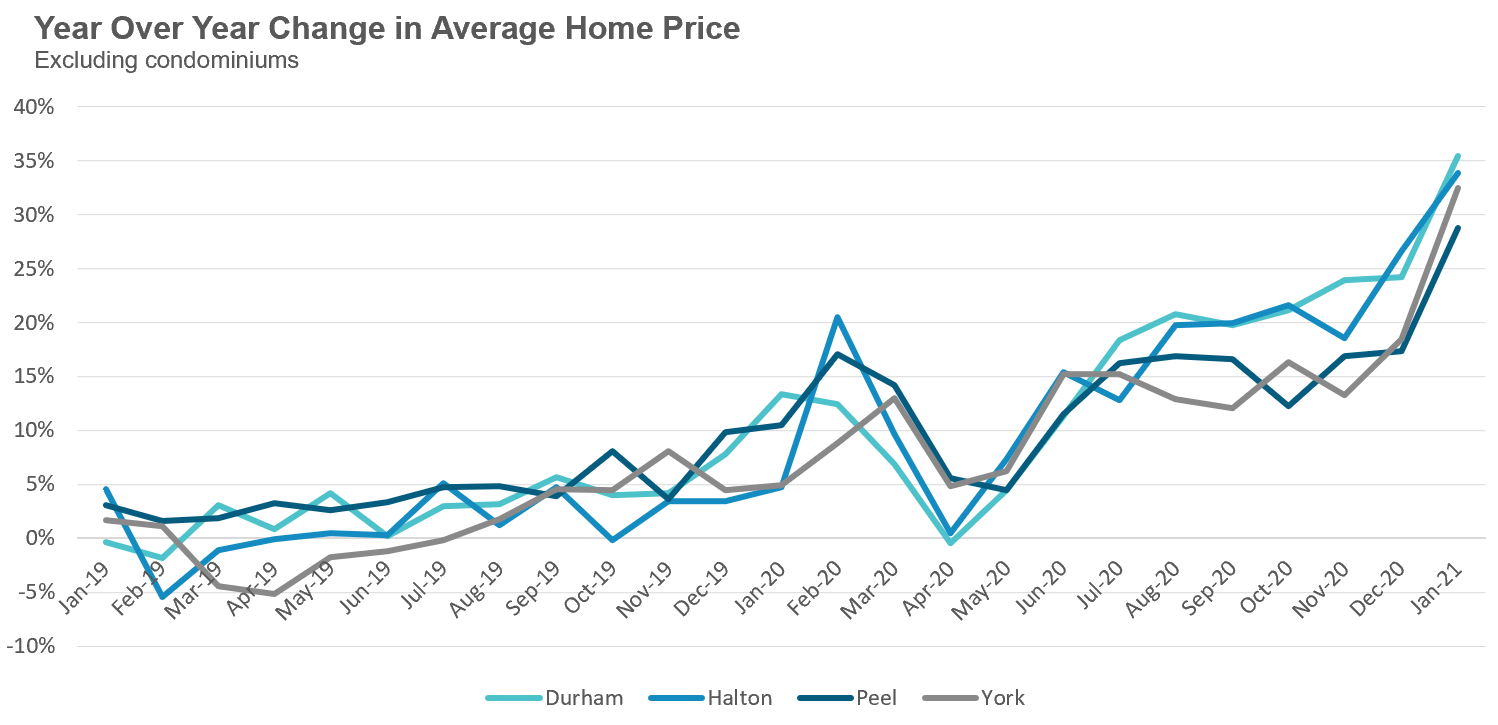

Suburban house prices have been accelerating since the first quarter of 2020 and after hitting a short pause during the spring lockdowns continued their trend up.

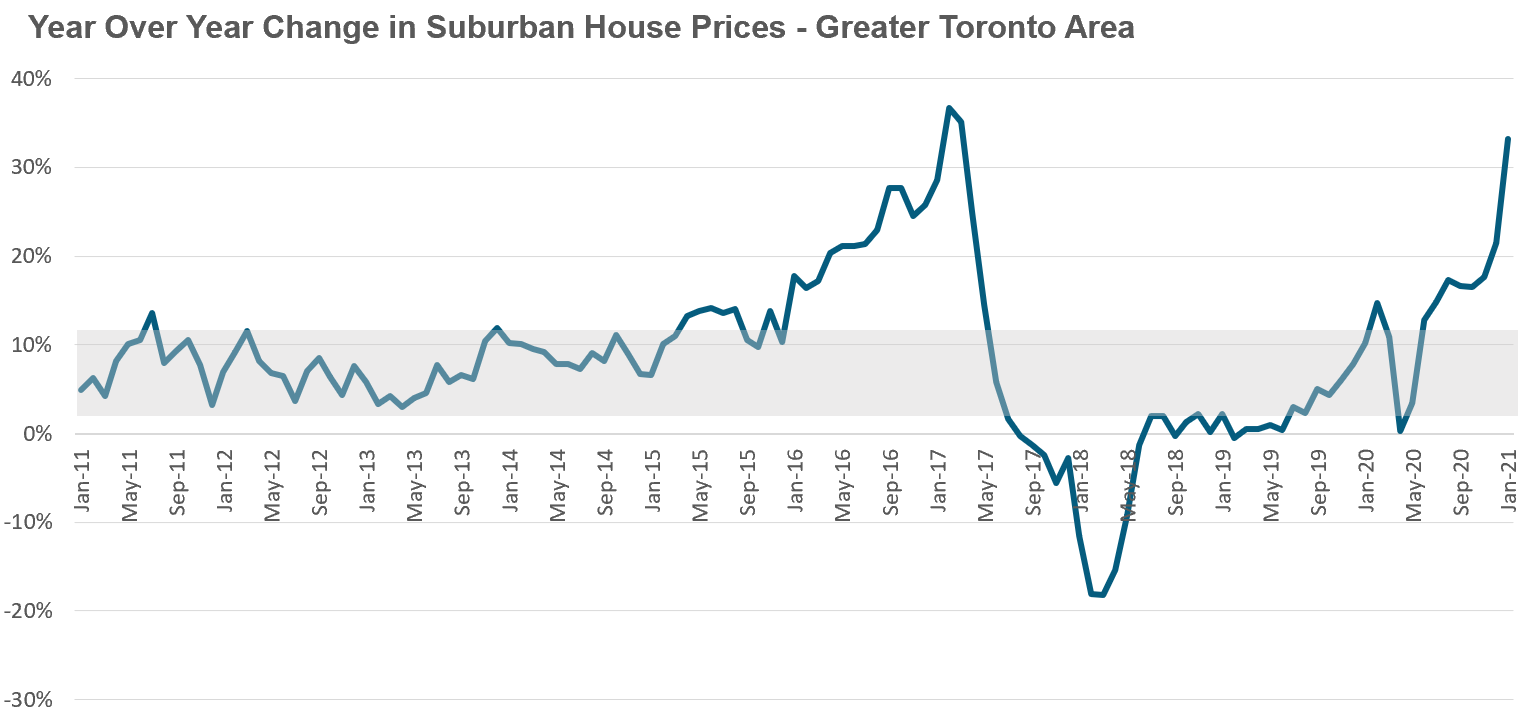

Let’s assume for a moment that the grey band represents the long term appreciation range for suburban house prices. Minor deviations from this range, like in late 2018 and early 2019 when price growth was below the range is not particularly alarming and can be caused by policy changes that tighten mortgage lending, for example.

“A situation in which news of price increases spurs investor enthusiasm which spreads by psychological contagion from person to person, in the process amplifying stories that might justify the price increase and bringing in a larger and larger class of investors, who, despite doubts about the real value of the investment, are drawn to it partly through envy of others’ successes and partly through a gambler’s excitement.”

- Robert Shiller

The second reason is that we are in the middle of a booming housing bubble that investors believe the government will do everything in their power to keep going.

In a normal market, policy makers would typically be concerned to see house prices rising by over 30% per year and at a minimum would caution markets of the risks of this type of acceleration and that measures may be introduced in the future to cool the market.

In short, the message investors would normally get from governments is that they don’t like the trend they are seeing and they may step in to end it.

Things are quite different today. To start with, there appears to be absolutely no concern about the rapid acceleration we are seeing in house prices from our government or our central bank.

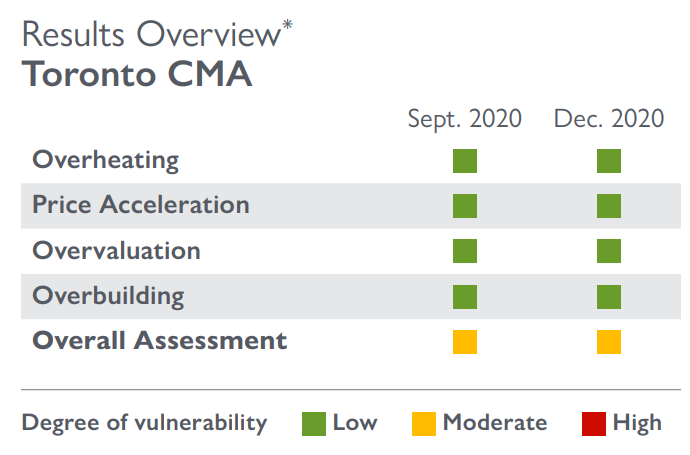

In December 2020, the Canadian Mortgage and Housing Corporation (CMHC) concluded that there was a low risk that house prices in Toronto were overvalued and a low risk of overheating and price acceleration. They came to this conclusion a month before suburban house prices in Toronto were up by more than 30% year-over-year.

Now, in CMHC’s defence, Toronto’s housing market is made up of many different submarkets and not all are overheating. But to suggest that the risks in Toronto as a whole are low, when house prices in the suburbs were up more than 30% year-over-year a month after their report seems quite odd. What can the average home buyer take away from CMHC’s conclusions? That prices rising by 30% year-over-year in the suburbs is normal?

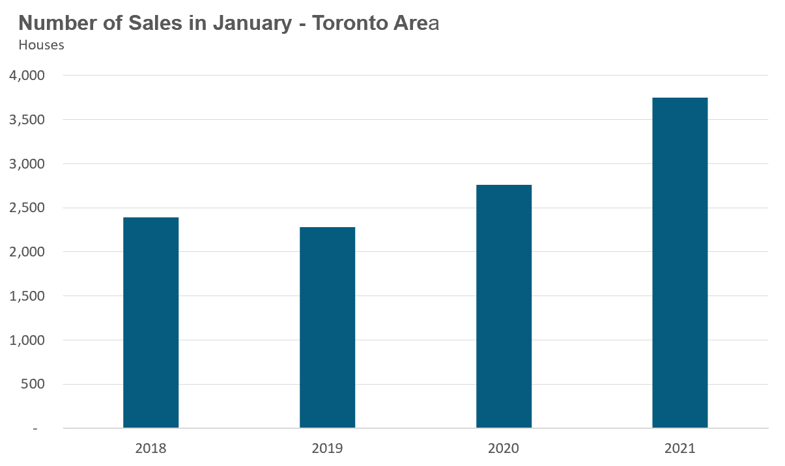

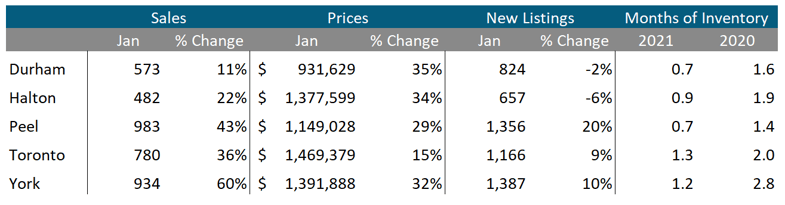

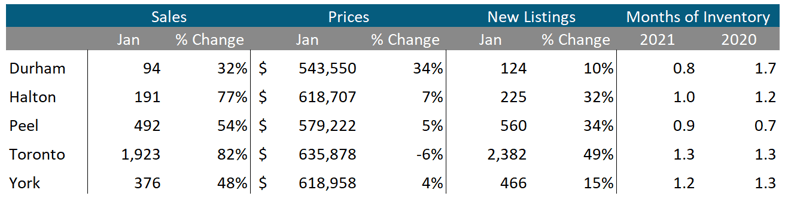

York Region showed the strongest growth in sales, up 60% over 2020.

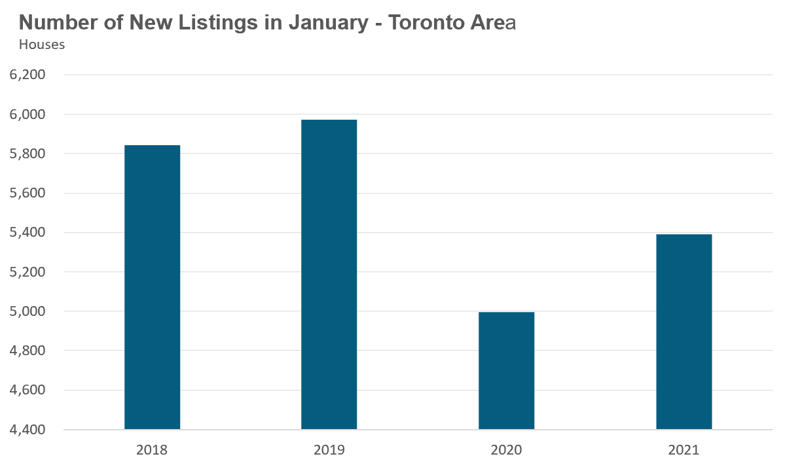

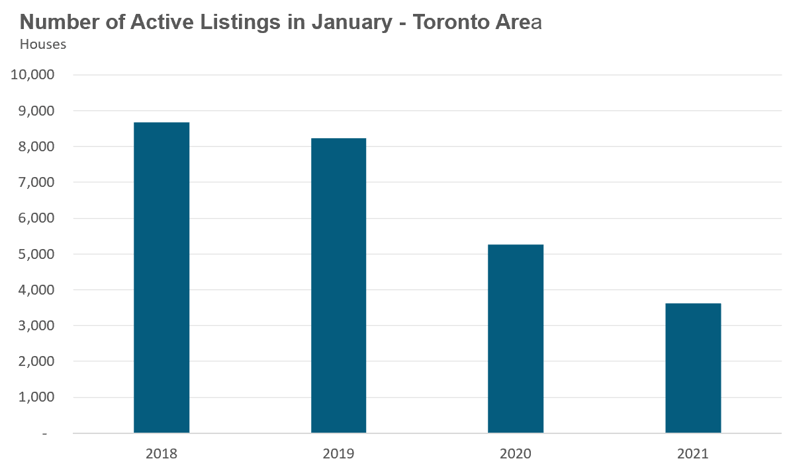

New listings did not keep up with the strong pace of demand. January saw an 8% increase in new listings over last year while the number of homes available for sale (“active listings”) was down 31% when compared to the same month last year.

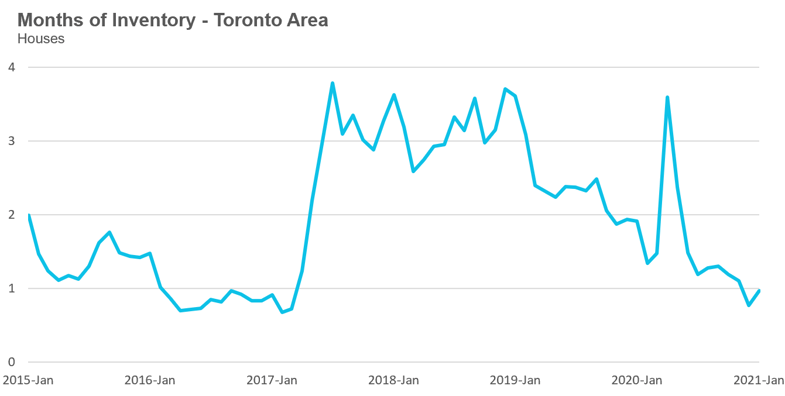

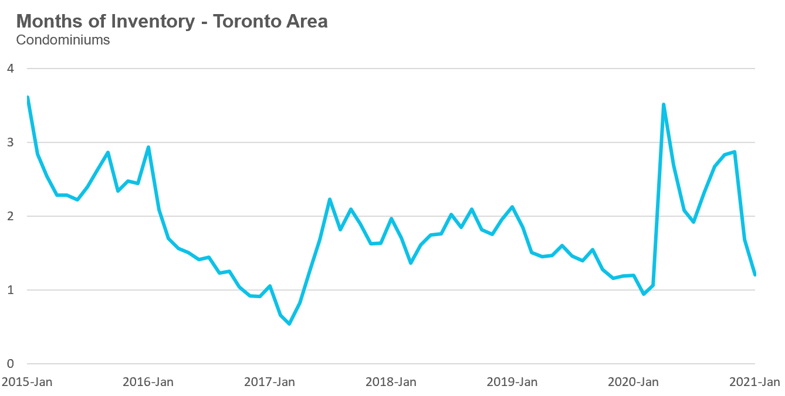

The Months of Inventory ratio (MOI) looks at the number of homes available for sale in a given month divided by the number homes that sold in that month. It answers the following question: If no more homes came on the market for sale, how long would it take for all the existing homes on the market to sell given the current level of demand?

The higher the MOI, the cooler the market is. A balanced market (a market where prices are neither rising nor falling) is one where MOI is between four to six months. The lower the MOI, the more rapidly we would expect prices to rise.

The market remained very competitive in January with an MOI of just 1 month of inventory.

While the current level of the MOI gives us clues into how competitive the market is on the ground today, the direction it is moving in also gives us some clues into where the market may be heading. While the MOI is up slightly over last month, inventory is still deep in seller’s market territory.

Strong demand coupled with very low inventory levels helped push average house prices up to another record high of $1.272M and up 29% over last year.

Median house prices are up by the same amount over last year.

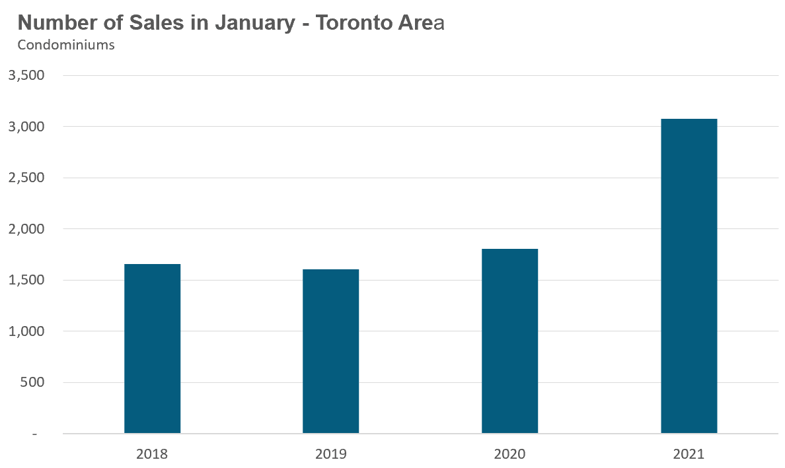

Condominium (condo) sales (condo apartments, condo townhouses, etc.) in January were up by 70% over last year led by an 82% increase in sales in the City of Toronto

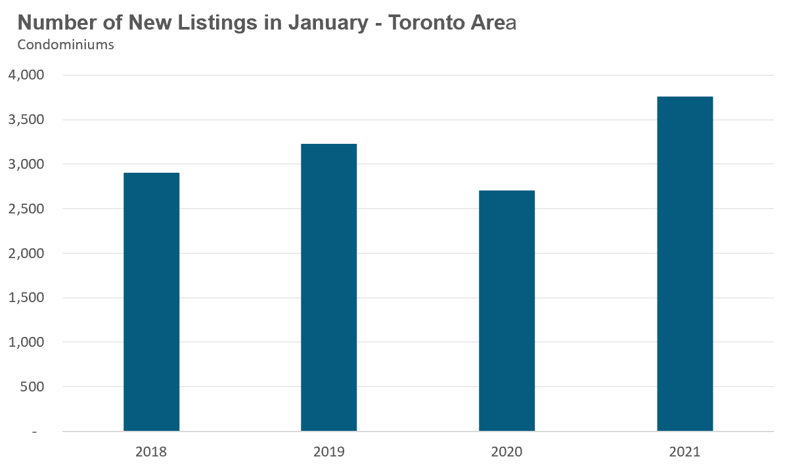

New condo listings were up by 39% in January 2021 over last year while active listings were up 71% over last year.

While active listings are still up over last year, the available inventory has been trending down since October when active condo listings peaked at 8,772.

This decline in active listings is leading to a more competitive condo market with the MOI decreasing from just under 2.9 months in November to 1.2 in January.

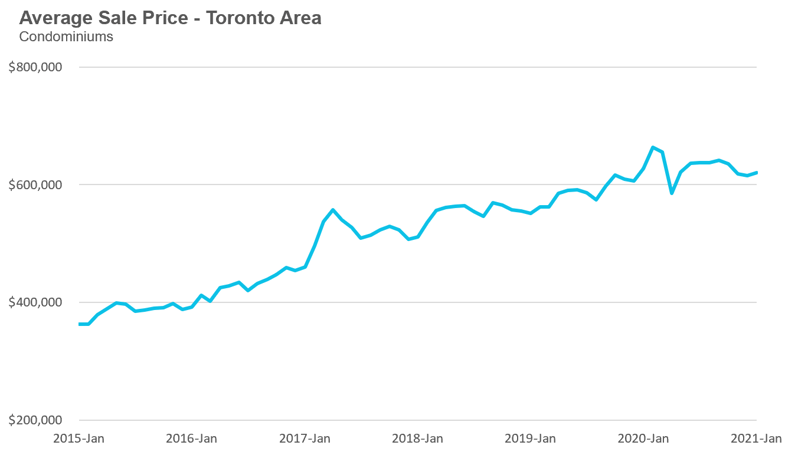

Toronto area condo prices are down 1% over last year. The decline in prices was due to the City of Toronto where prices were down 6% while suburban condo prices were up over last year.

The decline in Toronto condo prices should not be interpreted as a current trend. Condo prices in Toronto fell in the second half of 2020 but have been relatively stable over the past few months. We are seeing a decline in prices today because we are comparing today’s stable but lower prices against the peak prices reached during the first quarter of 2020.

Houses

Durham region saw only an 11% increase in sales but the strongest price growth (up 35%) because it has the most affordable and tightly supplied market with 0.7 MOI. Average prices were up 29%-35% in the suburbs while prices in the City of Toronto were up 15%. Despite the increase in new listings in Peel, York and Toronto inventory levels are at or below 1 month across the entire GTA.

Condos

Condominium (condo) sales saw a surge in sales in January across the entire GTA. Average prices were up across the suburban regions with the City of Toronto recording a 6% decline in average price.

Inventory levels are roughly at the same level as last year for all five regions.

Browse All Regional Market Trends for December 2020 on Realosophy.com:

Greater Toronto Area Market Trends

Durham Region Market Trends

Halton Region Market Trends

Peel Region Market Trends

City of Toronto Market Trends

York Region Market Trends

Market Performance by Neighbourhood Map, Toronto and the GTA